Issuer Free Writing

Prospectus

Filed Pursuant to Rule

433

File No.

333-248546

File No.

333-241569

File No.

333-230623

File No.

333-223943

December 30,

2020

FWP

NOTICE

The Teucrium Commodity Trust has filed a

registration statement (including a prospectus) with the SEC for

the offering to which this communication relates. Before you

invest, you should read the prospectus in that registration

statement and other documents that the Teucrium Commodity Trust has

filed with the SEC for more complete information about the issuer

and this offering. You may get these documents for free by visiting

EDGAR on the SEC Website at www.sec.gov. Alternatively, a copy of

the prospectus for each Fund may be obtained at

https://teucrium.com/ or

by calling (802) 540-0019.

____________________________________

2021 Grain

Outlook

The Big

Shift

Jake Hanley, Portfolio

Manager

Last year we wrote that the 2020s

could possibly mark the resurgence of a commodity bull market. That

thesis was put to test early this year as pandemic fears gripped

markets and initially caused assets across the globe to head lower.

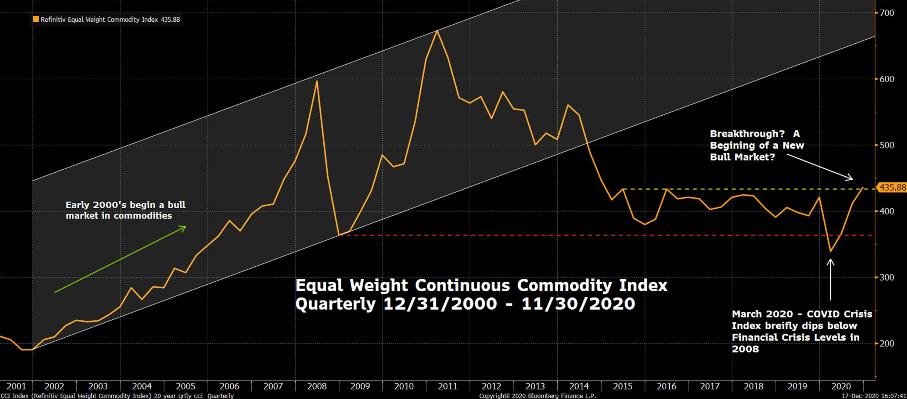

The Refinitiv Equal Weight Commodity Index briefly dipped below the

2008 financial crisis low, before reversing higher. Now the index

looks poised to break through 5-year highs, a move that could

potentially validate our commodity bull market

thesis.

Chart 1

Chart created by Teucrium using

Bloomberg Finance LP on 12/17/2020

Refinitiv Equal Weight Continuous

Commodity Futures Price Index

Quarterly Price Chart

12/31/2000–11/30/2020

Past performance is not indicative

of future results

Taking the grains specifically, we

might one day point back to 2020 as the year that began the

Big Shift. The Big Shift would mark the transition to

a secular bull market. Price trends are indicating that the

Big Shift in grains may

already be underway. As the market picture becomes clear over the

course of 2021, we will be looking to the fundamentals for

confirmation of the Big

Shift.

Ultimately, whether or not grains

and commodity prices continue to move higher is anyone’s

guess. Still, one trend remains clear: increasing investor appetite

for exposure to alternative asset classes. Having lived through

periods of high stock and bond price correlation, one can

understand investor desire for “non-correlated” assets.

That is, investments that tend to zig when others

zag.

What follows is an investigation of

the key drivers that may be leading to the Big Shift.

We begin our analysis by looking at

current and historic price patterns. We then explore supply and

demand fundamentals and review potential weather-related production

issues. At a high level, we discuss geopolitics, a weakening US

dollar, inflation on grain prices, and the potential

diversification benefits of including grains in a portfolio.

Finally, we conclude by relating our analysis back to the

investor.

We hope you find this information

interesting and valuable. Please do not hesitate to contact us with

questions or ideas you would like to discuss.

On behalf of all of us at Teucrium,

thank you for your continued interest in our

funds.

We wish you a Merry Christmas,

Happy Holidays, and a HAPPY NEW YEAR!

Prices Pointing

to a Big

Shift

Prices trend. When the price of an

asset is rising, it is likely to continue rising for some period.

Of course, the opposite is also true: when the price of an asset is

declining, it will likely continue its decline for some period. The

trick therefore is to identify, and determine the stage of, the

prevailing trend. Identifying a price trend and trend stage is not

easy to do. Even the best “trend followers” admit that

it is an imperfect science. Still, the recognition that prices

trend, and the potential to accurately identify the trend, has

captivated analysts and traders for centuries.1

Similar to the exercise of

predicting short-term weather versus long-term climate patterns, it

is difficult to predict a daily, weekly, or even monthly price

move. However, it can be much easier to accurately forecast

longer-range price trends.

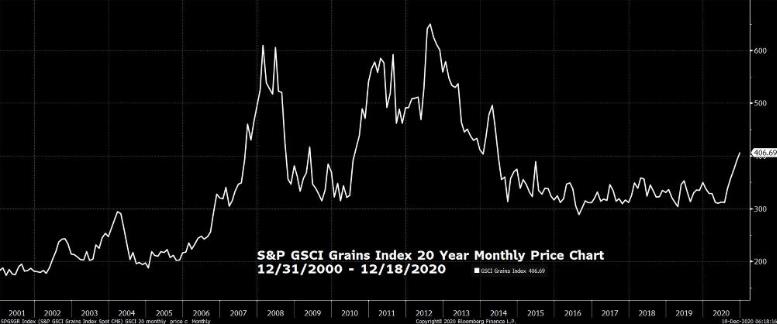

For example, take the following

one-year daily line chart on the S&P GSCI Grains Index. Notice

that the line is squiggly, even jagged, in some instances on a

shorter-term basis. It would be exceedingly difficult to predict

the price movement on any given day. Yet when you take a

longer-term perspective, you can see two very distinct trends that

occurred over two separate (approximate) six-month periods. There

is a downtrend that begins at the start of the year and an uptrend

beginning in early August.

Chart 2

Chart created by Teucrium using

Bloomberg Finance LP on 12/19/2020

S&P GSCI Grains

Index

Daily Price Chart

12/31/2019–12/11/2020

Past performance is not indicative

of future results

While the grain rally of 2020 has

been impressive, it may prove to be nothing more than a short-term

little shift in market

sentiment. Evidence for the Big

Shift must be derived from a longer-term analysis. For this

we’ve examined the 20 year monthly price chart for the GSCI

Grains Index.

Chart 3

Chart created by Teucrium using

Bloomberg Finance LP on 12/19/2020

S&P GSCI Grains

Index

Monthly Price Chart

12/31/2000–12/18/2020

Past performance is not indicative

of future results

Chart 3 is a simple line chart

showing the monthly closing price of the GSCI Grains Index over the

last 20 years. Note the price spikes in the middle of the chart in

2008, 2011, and 2013. Those price rallies occurred during periods

of tighter supplies resulting from decreased production or

extraordinarily strong demand. Also, note the recent rally on the

far right of the chart depicting the monthly price action for

grains in 2020.

A quick glance reveals that the

price advance appears to be coming off a price base that began in

2016. The recent highs also look to be testing price highs last

seen in 2015. A test of the 2015 highs confirms that grain prices

have moved to the upper end of their price range, but this alone is

not confirmation of a Big

Shift. A convincing monthly close above the 2015 highs,

however, would be considered supporting evidence that the

Big Shift is

underway.

Additional context presents us with

another view of the longer-term trend. Using the same monthly price

chart, we’ve added a moving average line (yellow) as well as

percentage bands to show when prices are 10% above or below the

moving average.

Chart 4

Chart created by Teucrium using

Bloomberg Finance LP on 12/22/2020

S&P GSCI Grains

Index

Monthly Price Chart

12/31/2000–12/18/2020

With 14 period simple moving

average & 10% Bands2

Past performance is not indicative

of future results

Notice that the downtrend beginning

in 2012 and identified by the moving average in 2013 continued

through 2016. The moving average appears to have transitioned from

a clear decline to a sideways pattern beginning in 2017. As grain

prices advanced in 2020, the moving average has once again begun

trending higher.

Moving averages are lagging

indicators, and this positive trajectory does not confirm that a

new uptrend is likely to continue. Still, market participants are

likely to view this as a positive development.

Furthermore, prices are now more

than 10% above the moving average for the first time since

2012.3The green arrows point to all periods

since 2001 where this occurred. The chart shows that a break above

this 10% line has historically preceded additional price

appreciation without exception since 2001. Note too that a break

below the 10% moving average band (red dotted line) has

historically, but not always, preceded additional price declines.

On both sides of the spectrum, about 50% of the moves above and

below the 10% channel led to longer-term price rallies and

longer-term price declines. The big question remains: where do we

go from here?

Historical performance is not

necessarily indicative of future results. Which way prices head

from here is anyone’s guess. One thing is certain: the market

will be keying in on supply and demand dynamics over the next year.

The fundamentals will either confirm or dispel the theory of the

Big

Shift.

“Charts are a picture of the

fundamentals.”—Sal Gilbertie

Fundamentals:

Supporting Prices (for now)

Commodity markets are primarily

driven by supply and demand. Grain market supply and demand is

estimated and reported monthly by the USDA in their World

Agricultural Supply and Demand Estimate report (WASDE). The supply

and demand data as presented is referred to as the “balance

sheet.” A balance sheet is said to be

“tightening” when supplies are declining relative to

demand, and “expanding” when supplies are increasing

relative to demand.

In general, US and global corn,

wheat, and soybean balance sheets have been tightening the last few

years. As part of that, the USDA is estimating all three grains

will have record high demand for the current production year. In

the past, we have learned that as the world builds a larger demand

base, it is difficult to deviate from this demand going forward,

even in years when there are production

shortfalls.

Importantly, the prices of corn,

wheat, and soybeans are highly correlated. This is due in large

part to the common and sometimes interchangeable uses for grains.

For example, the number one global use of corn and soybeans is to

feed animals. Wheat is also used as animal feed, though to a much

smaller extent. Corn, soybeans, and wheat can all also be used to

create biofuels. Given their interchangeability, a meaningful price

move in one of the grains can “pull” the prices of the

other two in the same direction. Perhaps this is one reason why we

continue to see relatively high wheat prices despite the expanding

global balance sheet.

Chart 5

This is for illustrative purposes

only and not indicative of any investment. Past performance is no

guarantee of future results.

Chart: DC Analysis, LLC, using data

from USDA through Sep. 30, 2020. Used with permission from DC

Analysis.

https://apps.fas.usda.gov/psdonline/app/index.html#/app/home

The information and data contained

herein do not constitute investment advice offered by Teucrium

Trading, LLC and are provided solely for informational

purposes.

Fundamentally, the move in grain

prices this year appears to be justified. Current US

Stocks/Use4

ratios for corn and soybeans are as low as they have been in the

last five years or more.

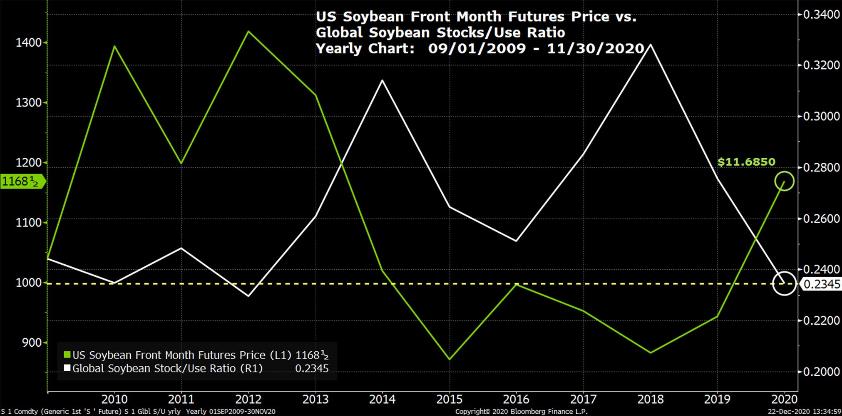

SOYBEANS

The US soybean balance sheet is

currently tighter than corn and the Stocks/Use ratio is the lowest

it’s been since the 2013–14 crop year. Globally, the

soybean Stocks/Use ratio is as low as it has been since the

2015–16 crop year. See Chart 6.

Chart 6

Chart created by Teucrium using

Bloomberg Finance LP on 12/22/2020

Front Month Soybean Futures vs

Global Stocks/Use Ratio

Monthly Price Chart

09/01/2009–11/30/2020

Past performance is not indicative

of future results

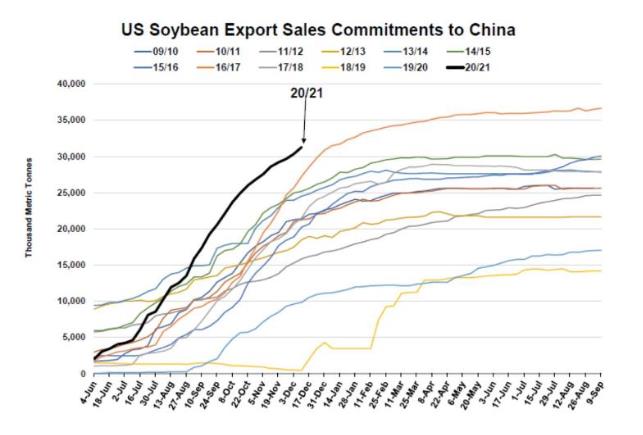

U.S. soybean supplies have dwindled

as Chinese soybean imports have soared over the last two years. In

the 2018–19 crop year, the Chinese imported a total of 82.54

million metric tons (MMT) of soybeans, equivalent to approximately

3 billion bushels. The 2020–21 crop year estimates show China

importing 100 MMT, or nearly 3.7 billion bushels. That jump, if

realized, would represent a 23% increase in just two years. The

growth in Chinese soybean demand appears to be tied to the

rebuilding of their hog herd and the stockpiling of strategic

reserves.5 What’s more, the Chinese are

relying heavily on US soybean exports, reflected by the historic

amount of U.S. soybean sales commitments already made this crop

year (see Chart 7).

Chart 7

This is for illustrative purposes

only and not indicative of any investment. Past performance is no

guarantee of future results. Chart: DC Analysis, LLC, using data

from USDA through December 17, 2020. Used with permission from DC

Analysis. The information and data contained herein do not

constitute investment advice offered by Teucrium Trading, LLC and

are provided solely for informational purposes

Currently, attention is on the

South American soybean crop, specifically in Brazil and Argentina

as various degrees of drought continue to persist across large

portions of those countries. Brazilian and US combined soybean

exports represent over 85% of total global soybean exports. Brazil

alone accounts for about one-half of global soybean exports, and

any significant impact on production will impact the overall

balance sheet and place even more importance on the 2021–22

US crop. Brazilian soybean famers typically finish planting in

December and harvest through March and April. Despite weather

challenges, it is possible that Brazil could produce a record

soybean crop even if the USDA reduces their current crop estimate

of 133 MMT down to analysts’ estimate of around 130 MMT. Note

that Brazilian production of 133 MMT is already reflected in the

global balance sheet. Anything less than that would likely be

viewed by the trade as supportive for prices.

CORN

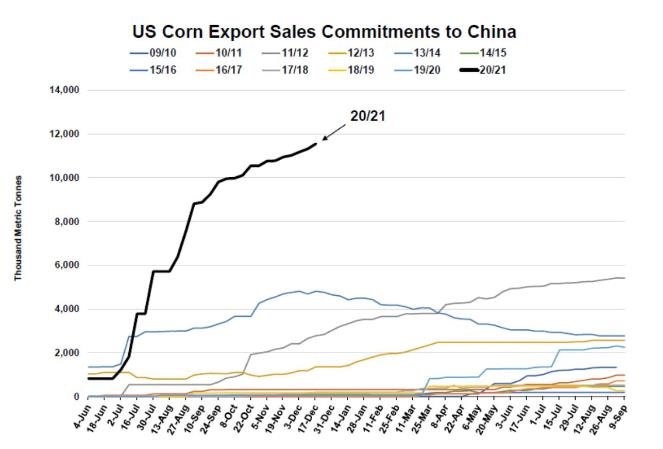

Importantly, the Chinese are also

poised to import a record amount of US corn. As of December 17,

2020, U.S. corn export sales commitments to China stand at a record

11.55 MMT for the 2020–21 crop year, which began on September

1, 2020. China, until this year, has never imported more than 6 MMT

from the world market.

Chart 8

This is for illustrative purposes

only and not indicative of any investment. Past performance is no

guarantee of future results. Chart: DC Analysis, LLC, using data

from USDA through December 17, 2020. Used with permission from DC

Analysis. The information and data contained herein do not

constitute investment advice offered by Teucrium Trading, LLC and

are provided solely for informational purposes

Internal Chinese corn demand

appears to be robust, with domestic Chinese corn prices trading

near 5-year highs. The Chinese aggressively auctioned off corn

inventories this year to both alleviate price inflation and

maintain freshness of state reserves. Presumably, China is

replenishing their reserves and is taking advantage of pricing

arbitrage, buying US corn for around $4 and selling older domestic

reserves for as much as double that amount.

Chart 9

Chart created by Teucrium using

Bloomberg Finance LP on 12/22/2020

Front Month Dalian Corn Futures vs

Front Month Corn Futures

Daily Price Chart

12/31/2019–12/18/2020

Past performance is not indicative

of future results

Robust global demand and tighter

balance sheets have helped push corn prices to their current

levels, testing the 5-year highs. However, to confirm the

Big Shift we will likely

need to see continued tightening of the global corn balance sheet

through the 2021–22 crop year.

Potential

Weather Challenges

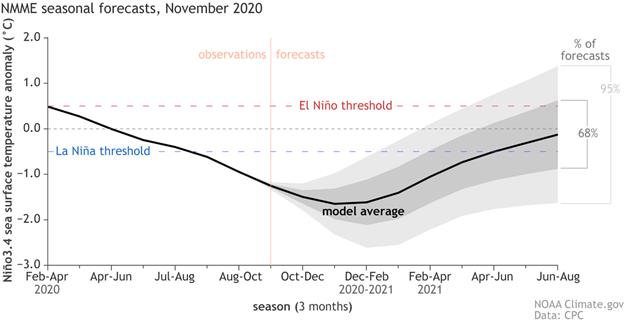

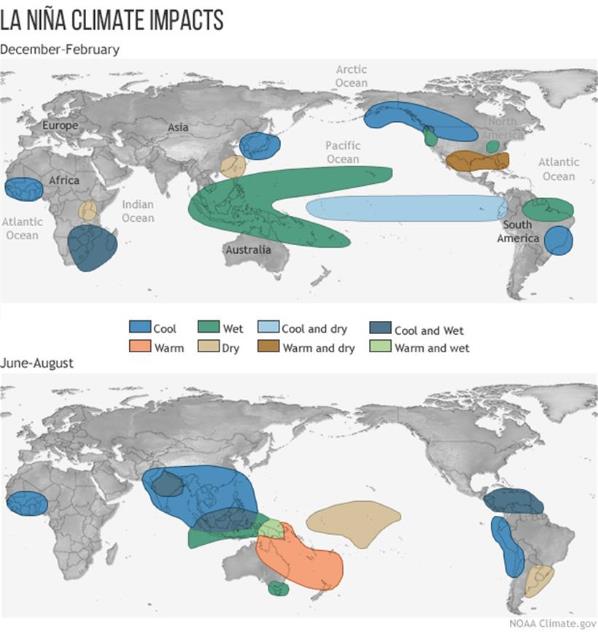

Weather challenges appear likely to

extend beyond 2020 and confront farmers across the globe again in

2021. Furthermore, these challenges may be exacerbated if the

current La Niña weather pattern

strengthens.

NOAA confirmed La Niña in

September 2020 and recent forecasts show that the pattern is likely

to remain in place through spring 2021. Typically, La Niña

occurring between June and August leads to drier weather in

southern Brazil and northern Argentina (see Charts 8–9). La

Niña occurring between December and February results in cooler

but not necessarily dryer weather for Brazil. However, should La

Niña continue on through June and August 2021, we would expect

continued dry conditions in Brazil and Argentina which could

negatively impact grain production in both

countries.

Chart 10

Chart 11

The La Niña weather pattern is

also likely responsible for dryness impacting US winter wheat

farmers as well. Remember, impacts during the winter months when

winter crops are in dormancy can be minimal but will grow in

importance once those crops start their final growth stages in the

spring. That said, current drought conditions extend far beyond the

areas typically affected by La Niña in the

US.

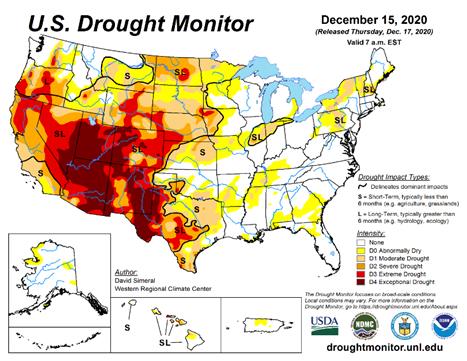

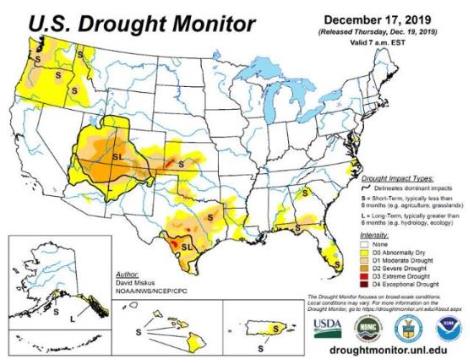

The most recent US Drought Monitor

shows severe, extreme, and exceptional drought across midwestern

states stretching down from North Dakota through Texas. The

December 17th, 2019 map is shown

below for the sake of comparison.

Chart 12

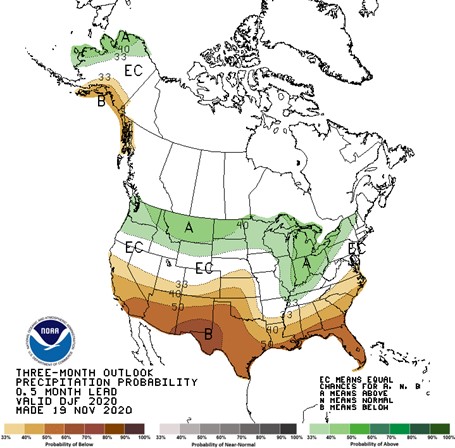

NOAA is forecasting above normal

precipitation for northern states this winter, and below normal

precipitation for southern states. If realized, this means states

such as Kansas, Oklahoma, and Texas, which are already experiencing

drought, will only get drier over the next few

months.

Chart 13

As mentioned, the most immediate La

Niña-influenced weather impact is on US winter wheat farmers.

The US winter wheat crop condition ratings have taken a hit with

43% of the crop rated “Good to Excellent” versus 52%

rated “Good to Excellent” last year.6 Wheat prices, however, are as likely to

be heavily influenced by production in Russia, the world’s

largest wheat exporter. The wheat trade is watching weather

conditions in Russia and the Black Sea region more broadly as

dryness has been a concern in key growing areas. According to the

Russian agricultural consultancy Sovecon, 22% of the Russian wheat

crop is in poor condition and in the worst shape since

2009–10.7 Despite all of this, global wheat

production is forecast to exceed demand for the 2020–21 crop

year.

International

Relations and Trade

While weather may be the critical

factor impacting grain prices in the year ahead, one cannot

overlook the potential impact of geopolitics.

During the spring of 2020, wheat

prices outperformed stocks as consumers and nations alike rushed to

procure pastas, breads, and wheat. Russia, in an attempt to shore

up their domestic supply, signaled that they would be capping their

exports. This was a significant development for wheat importers and

highlighted the need for sovereign nations to fortify both their

food stocks and their international supply chains for all

grains.

Case in point, a portion of Chinese

grain purchases, including corn, soybeans, wheat, and rice appears

to be tied to an effort to restock and increase domestic grain

reserves. China’s consumption needs and/or its desire to

stockpile grains inextricably ties China to the US and other global

grain exporters for the foreseeable future. While the relationship

between China and the US is volatile, we do not see a scenario

where the Chinese can turn away from American grain markets any

time soon.

China accounts for approximately

two-thirds of the world’s global soybean imports. Recall that

the US and Brazil account for over 85% of global soybean exports.

The US, Brazil, and Argentina are three of China’s largest

markets for soybeans. China would not be able to meet its soybean

demand without these three countries. What’s more, Brazil

recently purchased soybeans from the US. Presumably, Brazilian

farmers have “oversold” their crop and are importing in

order to meet domestic demand. The point here is that China needs

US soybeans, and they will likely continue to purchase from the US

regardless of political tensions.

A Weakening US

Dollar

Having recently dipped to around

90, the Dollar Index (DXY)8 is now approaching 5-year lows around

89.

Chart 14

Chart created by Teucrium using

Bloomberg Finance LP on 12/19/2020

Dollar Index (DXY) Weekly Price

Chart 12/31/2015–12/18/2020

Past performance is not indicative

of future results

We see a weakening US dollar as

providing additional incentive for China and other countries to

purchase US grains. A weak US dollar has historically been a

tailwind for US grain exports as well as for global grain prices.

The dollar/grain commodity relationship is relatively

straightforward. Globally, commodities are priced in dollars. A

weakening US dollar means that commodities in general, and US

exports in particular, become more competitive relative to other

non-dollar currencies. For example, if the US dollar depreciates

against the euro, then it will take fewer euros to purchase the

same amount of goods priced in dollars. All else being equal, the

increase in demand for dollar-denominated US goods would generally

be supportive of prices.

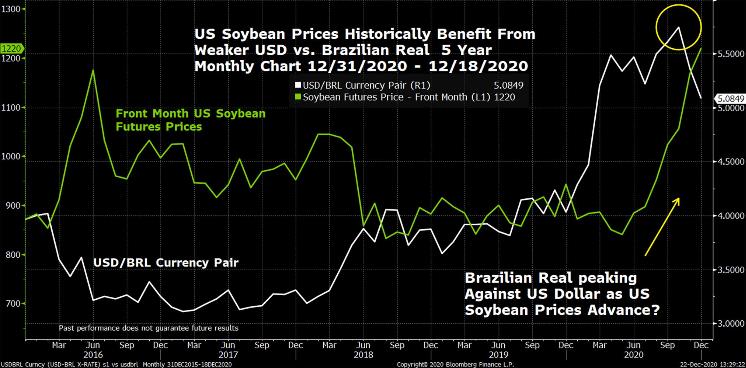

While the Dollar Index (DXY)

provides a quick read on dollar strength/weakness, the dollar/real

and dollar/ruble currency pairs are more important indicators

relating to global grain prices. Historically, global soybean

prices have moved higher as the dollar weakens versus the Brazilian

real because Brazilian soybean farmers are less likely to export

soybeans versus selling soybeans domestically.

Chart 15

Chart created by Teucrium using

Bloomberg Finance LP on 12/22/2020

Front Month Soybean Futures vs

USD/BRL Currency Pair

Monthly Price Chart

12/31/2015–12/18/2020

Past performance is not indicative

of future results

The same relationship exists

between the dollar/ruble currency pair and US wheat prices. Note,

however, that the US is among a handful of large global wheat

exporters. While a weaker dollar vs. the ruble makes US wheat

“cheaper” vs. Russian wheat, global importers still

have a multitude of options. Even so, given that Russia is the

world’s largest wheat exporter, dollar weakness against the

ruble is seen as being supportive for global wheat

prices.

Note that the USD is simultaneously

weakening against currencies of some of the world’s largest

wheat exporting nations. The US dollar declining across the board

could provide a tailwind for global wheat

prices.

The world’s top wheat

exporting nations according to the USDA are as follows: Argentina,

Australia, Canada, European Union, Russia, and the Ukraine. The

appreciation of the USD vs the Argentinian peso is beyond the chart

and is not depicted in Chart 16. Argentina is the smallest of the

seven major global wheat exporters.

Chart 16

Chart created by Teucrium using

Bloomberg Finance LP on 12/22/2020

USDCAD, USDEUR, USDUAH, USDRUB,

USDAUD Currency Pairs

Monthly Price Chart

12/31/2015–12/18/2020

Past performance is not indicative

of future results

Inflated

Inflation Expectations?

Many are pointing to the

unprecedented US fiscal and monetary response to the COVID-19

pandemic as the key driver for a weaker dollar globally.

Additionally, market participants seem to be increasingly weary of

the potential for inflation in the US. Caution is warranted,

however, as we do not believe that security purchases by the

Federal Reserve (i.e., Quantitative Easing or QE) alone are enough

to spark broad based inflation in the US.9 Consider that 12 years after QE 1 was

announced, headline CPI remains below 2% year over

year.

We do think inflation concerns are

warranted when considering the Federal Reserve’s potential to

adopt Modern Monetary

Policy combined with fiscal experimentation with some level

of Universal Basic Income.

The combination of these two policies would amount to something new

that we will call Monetary

Spending.10 Monetary spending could lead to a

scenario where demand for consumer goods outpaces the supply of

those goods thereby sparking broad based

inflation.

More immediately and far more

likely in our opinion, is the effect rising crude oil and natural

gas prices will have on future moves in headline inflation. New

policy shifts in the U.S., and indeed throughout the globe, toward

the “greening” of the current carbon-based energy

industry will accelerate the already developing inflationary trends

in crude oil and natural gas. New administrative, environmental,

and tax policy burdens that disincentivize the production of fossil

fuels will cause crude oil and gas prices to rise, raising overall

inflation rates across the globe. In the end, this could create

more demand for grains via increased usage of alternative fuels

like ethanol and biodiesel.

While broad-based inflation would

likely provide an additional tailwind to grain prices, food prices

are already running far north of headline CPI. As of November 30,

food prices are up 3.94% year over year versus a headline CPI of

1.175%.

We believe investors who are

actively positioning their portfolios for future inflation might do well to

consider current

opportunities in grains, especially if the trend of a weaker dollar

continues well into 2021.

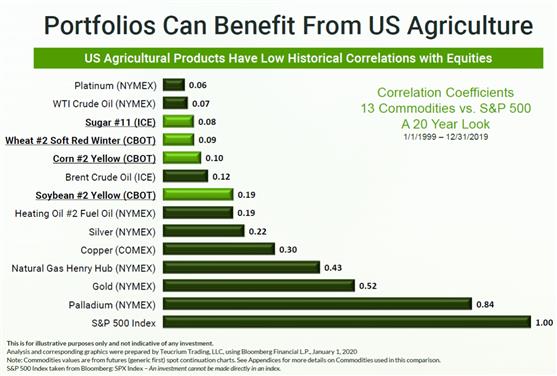

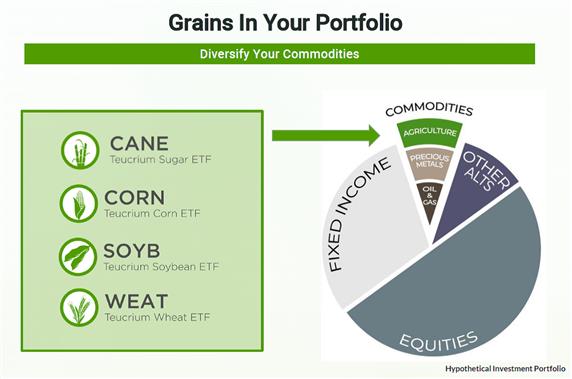

Grains in Your

Portfolio

Grains historically have low

correlations to equities. Low correlations have the potential to

improve portfolio outcomes during periods of stock market

volatility.

Chart 17

In our 2020 Outlook, we shared the

view that investors would likely be looking to commodities as an

alternative asset class, specifically looking at grains to further

diversify their commodity exposure.

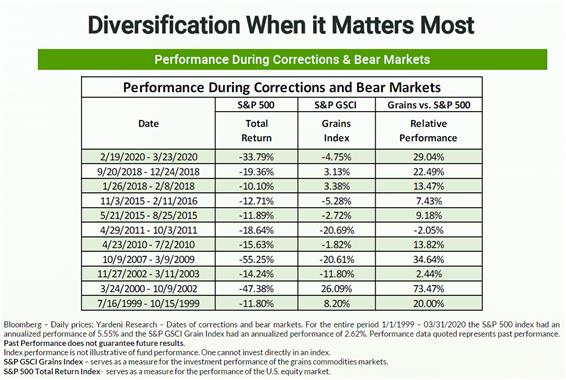

In fact, the GSCI Grains Index has

outperformed the S&P 500 in 10 out of the last 11 stock market

corrections of 10% or more. We included this data point in our 2020

Outlook last December. At that time, we had no idea that the next

equity bear market was just around the corner. The S&P 500 fell

nearly 35% peak to trough through March 2009. During that time the

GSCI Grains declined by 4.75%, outperforming stocks once again by

approximately 29%.

Chart 18

The historical tendency for grain

prices to outperform equity prices during stock market corrections

suggests that investors may benefit from an allocation to grains

precisely when it matters most, i.e., during significant stock

market declines.

While an investment in grains comes

with upside potential and downside risks, the potential portfolio

diversification benefits should not be overlooked. In 2020, grains

investors have experienced both portfolio diversification benefits

and upside price moves.

Stressing the importance of

diversification may be cliché, yet too many investors tend to

overlook the importance of diversifying their commodity exposure.

Our experience has shown that many investors’ commodity

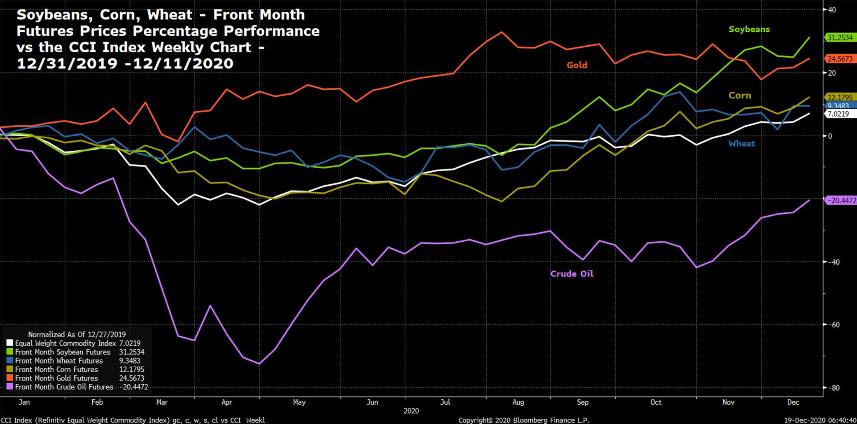

allocations remain overweight in gold and oil. The chart below

shows the percentage performance of corn, wheat, soybeans, gold,

and oil versus the Refinitiv Equal Weight Commodity Index this year

(through 12/11/2020). Note that gold, soybeans, corn, and wheat all

outperformed the index while oil trailed significantly. Markets in

2020 clearly demonstrated why it’s important to diversify

one’s commodity exposure beyond the most commonly held

commodities of precious metals and energy by also considering an

allocation to grains. We are confident in this view and point to

the 67% increase in shares outstanding for Teucrium’s

grain-based ETFs over the past 11 months.

Chart 19

Chart created by Teucrium using

Bloomberg Finance LP on 12/19/2020

Front Month: Soybean Futures, Wheat

Futures, Corn Futures, Gold Futures, Crude Oil Futures and the

Refinitiv Equal Weight Continuous Commodity Futures Price

Index

Weekly Price Chart

12/31/2019–12/18/2020

Past performance is not indicative

of future results

Chart 20

Calling The

Big

Shift

Price performance of commodities in

general, and grains specifically, is pointing to the potential

shift to a secular bull market. Macro drivers, such as a weakening

US dollar, increasing annual grain demand, and production

uncertainties, seem to be providing tailwinds at the moment.

Ultimately, the fundamental drivers of supply and demand will

dictate where grain prices go from here. Weather is largely

unpredictable and appears to be the biggest threat to production

and therefore supply. Global demand appears to be steady and

Chinese demand is expected to remain robust through the

2020–21 crop year.

A Big Shift in grain prices may

ultimately be realized in a scenario where production struggles to

keep pace with growing global demand.

Of course, production increases

and/or a decrease in demand could potentially halt or reverse the

Big

Shift.

Time will tell.

For ongoing grain market commentary

and analysis, please follow us on Twitter

@TeucriumETFs

and visit our website at

www.teucrium.com

Portfolio

Diversification That Grows

Disclosure:

An investor should consider

investment objectives, risks, charges and expenses carefully before

investing. The prospectus contains this and other information. Read

the prospectus carefully before investing. The Teucrium Corn,

Sugar, Soybean, Wheat and Agricultural Funds (the

“Funds”) are not mutual funds or any other type of

Investment Company within the meaning of the

Investment Company Act of 1940, as amended, and are not subject to

regulation thereunder. Foreside Fund Services, LLC is the

distributor for the Teucrium Funds. Teucrium’s FINRA Office

of Supervisory Jurisdiction is located at Three Main Street, Suite

215, Burlington, Vermont 05401.

A

copy of the prospectus for each Fund may be obtained at:

https://teucrium.com/

Futures Risks: Commodities and futures

generally are volatile and are not suitable for all

investors.

Futures investing is highly

speculative and involves a high degree of risk. An investor may

lose all or substantially all of an investment. Investing in

commodity interests subject each Fund to the risks of its related

industry. These risks could result in large fluctuations in the

price of a particular Fund's respective shares. Funds that focus on

a single sector generally experience

greater volatility. Futures may be affected by Backwardation: a market condition in

which a futures price is lower in the distant delivery months than

in the near delivery months. As a result, the fund may benefit

because it would be selling more expensive contracts and buying

less expensive ones on an ongoing basis; and Contango: A condition in which distant

delivery prices for futures exceeds spot prices, often due to costs

of storing and inuring the underlying commodity. Opposite of

backwardation. As a result, the Fund’s total return may be

lower than might otherwise be the case because it would be selling

less expensive contracts and buying more expensive

one.

_________________________