UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of July 2021

Commission File Number: 000-55899

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE, GRUPO FINANCIERO SANTANDER MÉXICO

(Exact Name of Registrant as Specified in Its Charter)

Avenida Prolongación Paseo de la Reforma 500

Colonia Lomas de Santa Fe

Alcaldía Álvaro Obregón

01219, Ciudad de México

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

| Form 20-F |

X |

Form 40-F |

|

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

| Yes |

|

No |

X |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

| Yes |

|

No |

X |

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE, GRUPO FINANCIERO SANTANDER MÉXICO

TABLE OF CONTENTS

| ITEM | |

| 1. | Second quarter 2021 earnings release of Banco Santander México, S.A., Institución De Banca Múltiple, Grupo Financiero Santander México |

| 2. | Second quarter 2021 earnings presentation of Banco Santander México, S.A., Institución De Banca Múltiple, Grupo Financiero Santander México |

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

|

BANCO SANTANDER MÉXICO, S.A., INSTITUCIÓN DE BANCA MÚLTIPLE, GRUPO FINANCIERO SANTANDER MÉXICO

| ||||

| By: | /s/ Hector Chávez Lopez | |||

| Name: | Hector Chávez Lopez | |||

| Title: | Executive Director of Investor Relations | |||

Date: July 30, 2021

Item 1

| |

| |

| TABLE OF CONTENTS | |

| I. Key Highlights for the Quarter | 2 |

| II. CEO Message | 3 |

| III. Summary of 2Q21 Consolidated Results | 3 |

| IV. Analysis of 2Q21 Consolidated Results | 11 |

| V. Relevant Events, Transactions and Activities | 26 |

| VI. Awards and Recognitions | 28 |

| VII. Credit Ratings | 29 |

| VIII. 2Q21 Earnings Call Dial-In Information | 30 |

| IX. Analyst Coverage | 30 |

| X. Definition of Ratios | 30 |

| XI. Consolidated Financial Statements | 34 |

| XII. Notes to Consolidated Financial Statements | 42 |

| XIII. Special Accounting Criteria — Subsidiaries | 174 |

Earnings Release | 2Q.2021 | |

Banco Santander México |  |

| 1 |

| |

| |

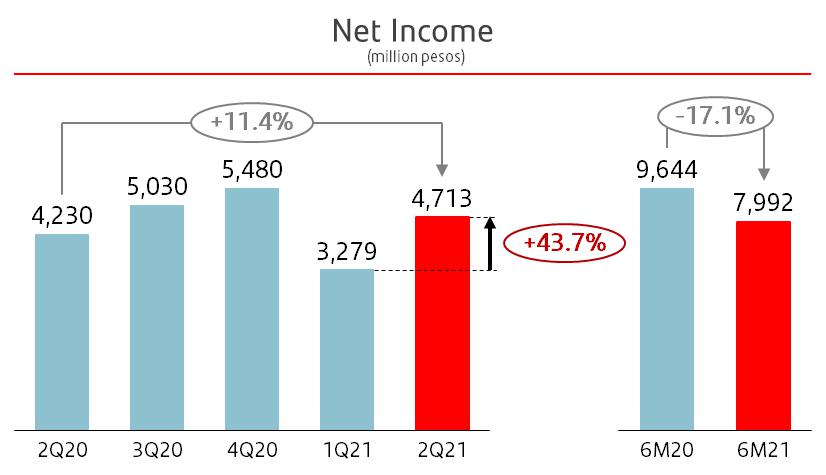

Banco Santander México Reports Second Quarter 2021 Net Income of Ps.4,713 Million

| - | Mortgages and auto loans continued to perform extremely well, along with government loans, as we continue to grow above market and gain market share while maintaining conservative origination standards. While loan volumes in commercial loans still reflected difficult YoY comps, there was sequential growth in middle-market loans and seems like SMEs loans reached an inflection point. Performance was in line with market trend and soft demand conditions. |

| - | Total deposits mix improved, driven by successful demand deposit attraction strategy. Meanwhile, total deposits also reflect difficult YoY comps, mainly in corporates, as their liquidity needs have normalized compared with year ago levels. |

| - | Net income increased 11.4% YoY in 2Q21, mainly due to lower provisions, stable NII, solid growth in fees and strict cost discipline. |

Mexico City – July 28th, 2021, Banco Santander México, S.A., Institución de Banca Múltiple, Grupo Financiero Santander México (NYSE: BSMX; BMV: BSMX), (“Banco Santander México” or “the Bank”), today announced financial results for the three-month and six-month periods ending June 30th, 2021.

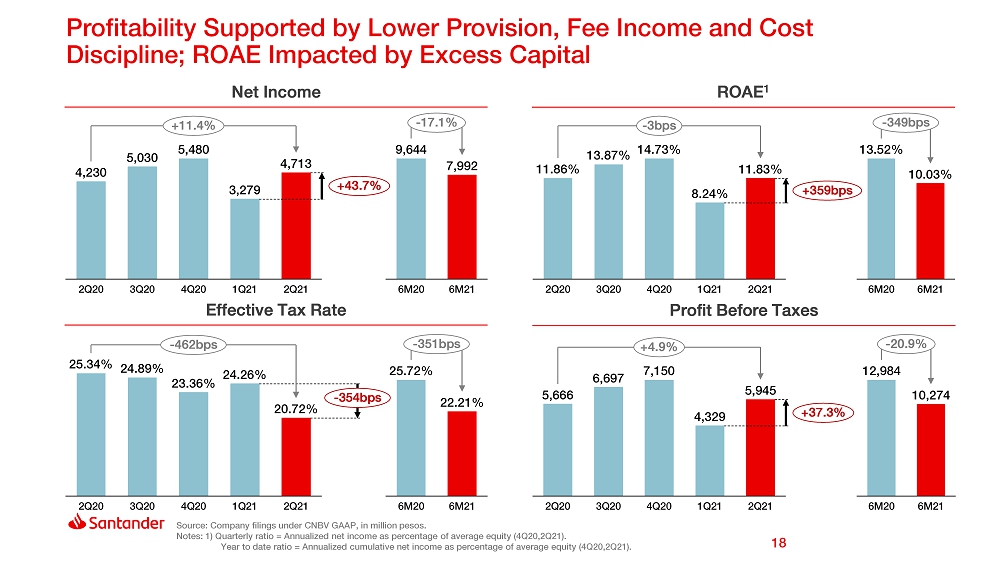

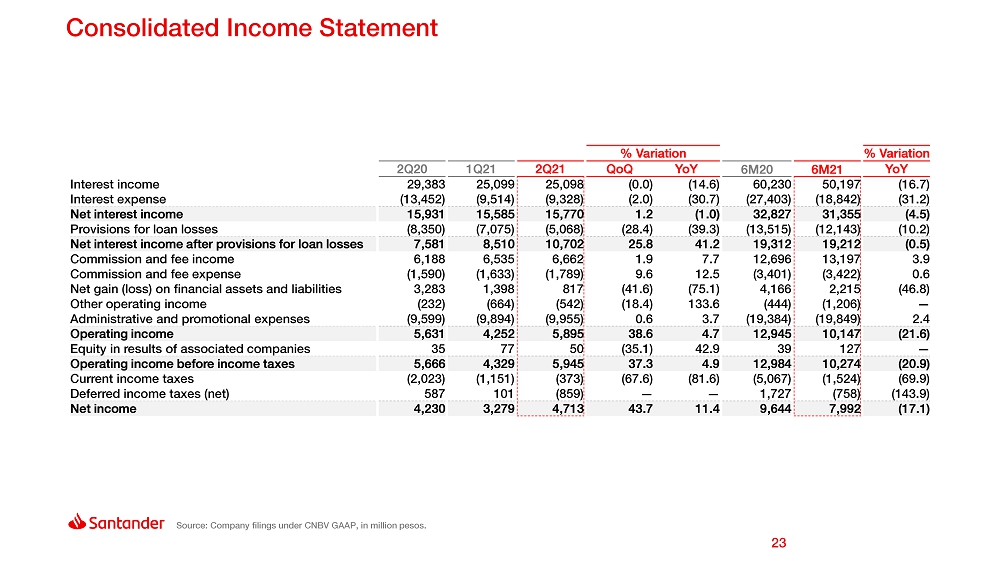

Banco Santander México reported net income of Ps.4,713 million in 2Q21, representing increases of 11.4% YoY and 43.7% QoQ. On a cumulative basis, net income for the first half of the year, reached Ps.7,992 million, representing a 17.1% YoY decrease.

| HIGHLIGHTS | ||||||||||||

| Results (Million pesos) | 2Q21 | 1Q21 | 2Q20 | %QoQ | %YoY | 6M21 | 6M20 | %YoY | ||||

| Net interest income | 15,770 | 15,585 | 15,931 | 1.2 | (1.0) | 31,355 | 32,827 | (4.5) | ||||

| Fee and commission, net | 4,873 | 4,902 | 4,598 | (0.6) | 6.0 | 9,775 | 9,295 | 5.2 | ||||

| Core revenues | 20,643 | 20,487 | 20,529 | 0.8 | 0.6 | 41,130 | 42,122 | (2.4) | ||||

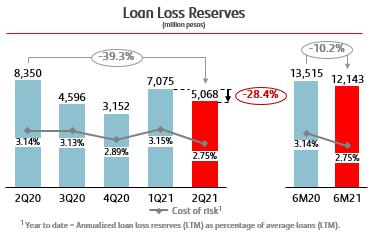

| Provisions for loan losses | 5,068 | 7,075 | 8,350 | (28.4) | (39.3) | 12,143 | 13,515 | (10.2) | ||||

| Administrative and promotional expenses | 9,955 | 9,894 | 9,599 | 0.6 | 3.7 | 19,849 | 19,384 | 2.4 | ||||

| Net income | 4,713 | 3,279 | 4,230 | 43.7 | 11.4 | 7,992 | 9,644 | (17.1) | ||||

| Net income per share1 | 0.70 | 0.48 | 0.62 | 43.7 | 11.4 | 1.18 | 1.42 | (17.1) | ||||

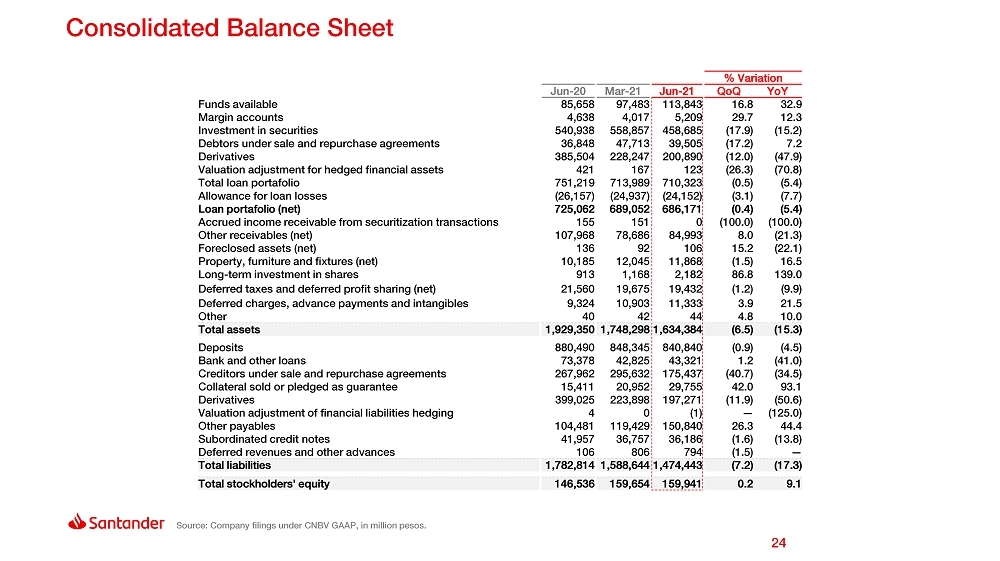

| Balance Sheet Data (Million pesos) | Jun-21 | Mar-21 | Jun-20 | %QoQ | %YoY | Jun-21 | Jun-20 | %YoY | ||||

| Total assets | 1,634,384 | 1,748,298 | 1,929,350 | (6.5) | (15.3) | 1,634,384 | 1,929,350 | (15.3) | ||||

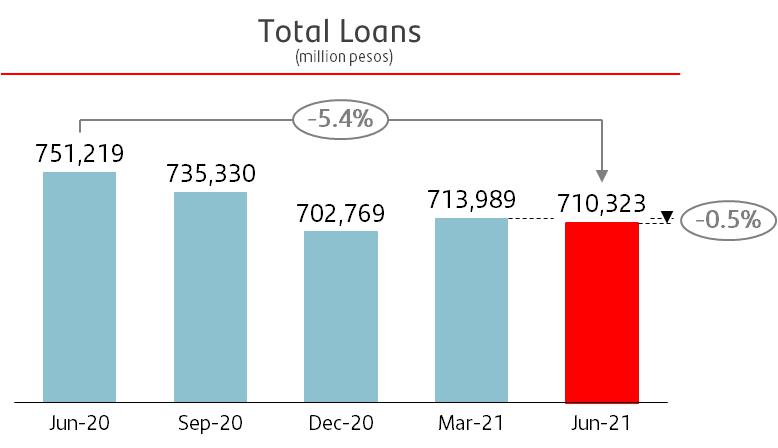

| Total loans | 710,323 | 713,989 | 751,219 | (0.5) | (5.4) | 710,323 | 751,219 | (5.4) | ||||

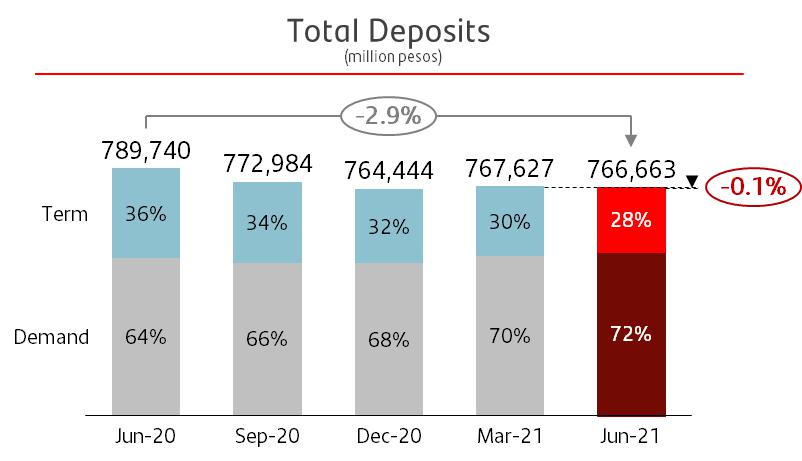

| Deposits | 766,663 | 767,627 | 789,740 | (0.1) | (2.9) | 766,663 | 789,740 | (2.9) | ||||

| Shareholders´ equity | 159,941 | 159,654 | 146,536 | 0.2 | 9.1 | 159,941 | 146,536 | 9.1 | ||||

| Key Ratios (%) | 2Q21 | 1Q21 | 2Q20 | bps QoQ | bps YoY | 6M21 | 6M20 | bps YoY | ||||

| Net interest margin | 4.52 | 4.42 | 4.48 | 10 | 4 | 4.47 | 4.93 | (46) | ||||

| Net loans to deposits ratio | 89.50 | 89.76 | 91.81 | (26) | (231) | 89.50 | 91.81 | (231) | ||||

| ROAE | 11.83 | 8.24 | 11.86 | 359 | (3) | 10.03 | 13.52 | (349) | ||||

| ROAA | 1.08 | 0.73 | 1.01 | 35 | 7 | 0.92 | 1.15 | (23) | ||||

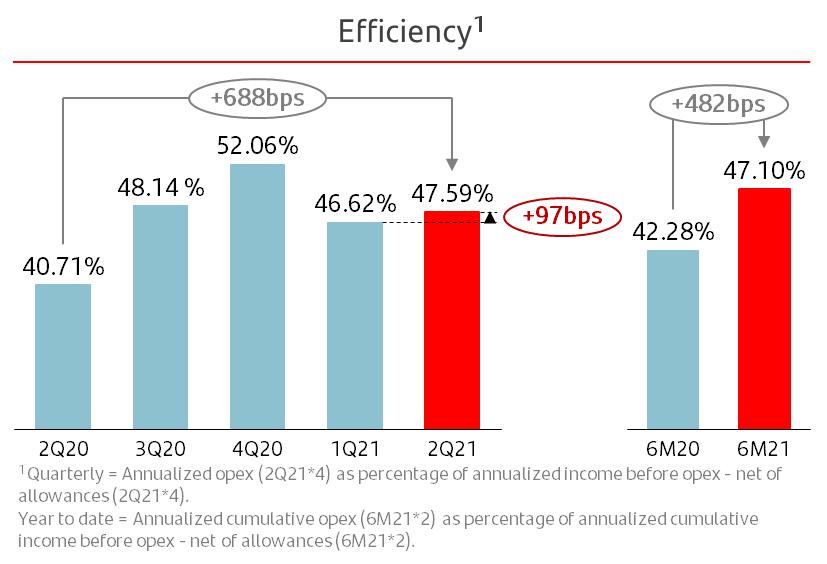

| Efficiency ratio | 47.59 | 46.62 | 40.71 | 97 | 688 | 47.10 | 42.28 | 482 | ||||

| Capital ratio | 18.91 | 19.73 | 16.69 | (82) | 222 | 18.91 | 16.69 | 222 | ||||

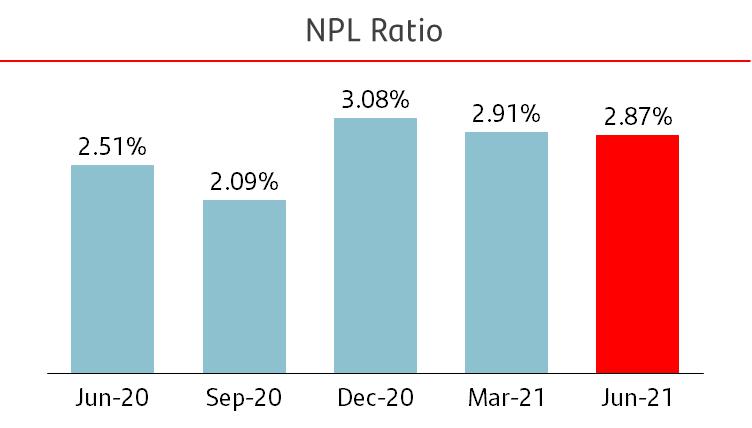

| NPLs ratio | 2.87 | 2.91 | 2.51 | (4) | 36 | 2.87 | 2.51 | 36 | ||||

| Cost of Risk | 2.75 | 3.15 | 3.14 | (40) | (39) | 2.75 | 3.14 | (39) | ||||

| Coverage ratio | 118.39 | 120.12 | 138.81 | (173) | — | 118.39 | 138.81 | — | ||||

| Operating Data | Jun-21 | Mar-21 | Jun-20 | %QoQ | %YoY | Jun-21 | Jun-20 | %YoY | ||||

| Branches | 1,039 | 1,007 | 1,050 | 3.2 | (1.0) | 1,039 | 1,050 | (1.0) | ||||

| Branches and offices2 | 1,352 | 1,352 | 1,406 | 0.0 | (3.8) | 1,352 | 1,406 | (3.8) | ||||

| ATMs | 9,534 | 9,497 | 9,142 | 0.4 | 4.3 | 9,534 | 9,142 | 4.3 | ||||

| Customers | 19,257,998 | 19,068,219 | 18,641,282 | 1.0 | 3.3 | 19,257,998 | 18,641,282 | 3.3 | ||||

| Employees | 23,512 | 22,280 | 20,007 | 5.5 | 17.5 | 23,512 | 20,007 | 17.5 |

| 1) | Accumulated EPS, net of treasury shares (compensation plan) and discontinued operations. Calculated by using weighted number of shares. |

| 2) | Includes cash desks (espacios select, box select and corner select) and SMEs business centers. Excluding brokerage house offices. |

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 2 |

| |

| |

Héctor Grisi, Banco Santander México’s Executive President and CEO, commented: “This quarter’s bottom line exceeded 2Q20’s level by 11% and was 44% higher than in the previous quarter. Although the wide ranging impact of the pandemic continues to affect the comparability of our results, this quarter we delivered a solid performance across the main line items of our P&L: NII and commissions were slightly higher than last year’s levels, we maintained tight control of expenses, and cost of risk converged to pre-pandemic levels. Together, this resulted in an ROE of 11.83%, very similar to the second quarter of 2020 and it was achieved despite the excess capital we had accumulated due to the regulatory restriction imposed on dividend payments.

In terms of individual loans, we continue to deliver the best performance among Mexican banks, with growth close to 10% and with market share gains in both mortgage and auto loans. Additionally, it appears we have reached an inflection point in credit cards, as balances have started to show modest growth. In commercial loans, we still reported a relevant contraction of 14%. Practically 60% of this contraction is explained by the reduction in loans to large corporates, with borrowings growing strongly last year when businesses drew down their committed lines of credit as a precautionary measure. By contrast, middle market loans grew compared to previous quarters, and in SMEs we expect to see a better performance in the second half of the year since the entire portfolio is not bound by the support program and we now have a greater risk appetite.

Deposits contracted by almost 3%, but with differentiated behavior. We expanded Demand deposits by 8%, while Term deposits decreased 23%. This market dynamic resulted from the significant reduction in interest rates. It is noteworthy that both Demand and Term deposits from individuals performed better than corporates. The former is in line with our strategy to continue attracting and building scale among individuals.

We continue to benefit from the boost that the pandemic has given banking digitalization. Digital customers grew 11% over the year, with digital transactions now representing 41% of our total transactions, up from 30% a year ago. Although the pandemic and the economic environment are still challenging us, we are making additional headway with our strategy, by continuing to execute with focus and discipline and by keeping intact our ambition to offer the best customer banking experience in Mexico. To that end, we continue to work on strengthening customer loyalty, seeking to consistently improve the quality of service and increase customer satisfaction levels. Further, we have certain plans and launches scheduled for the second half of the year that will take advantage of new digital tools and processes with which we continue to build a stronger franchise and seize the many growth opportunities ahead of us.”

III. Summary of 2Q21 Consolidated Results

Loan portfolio

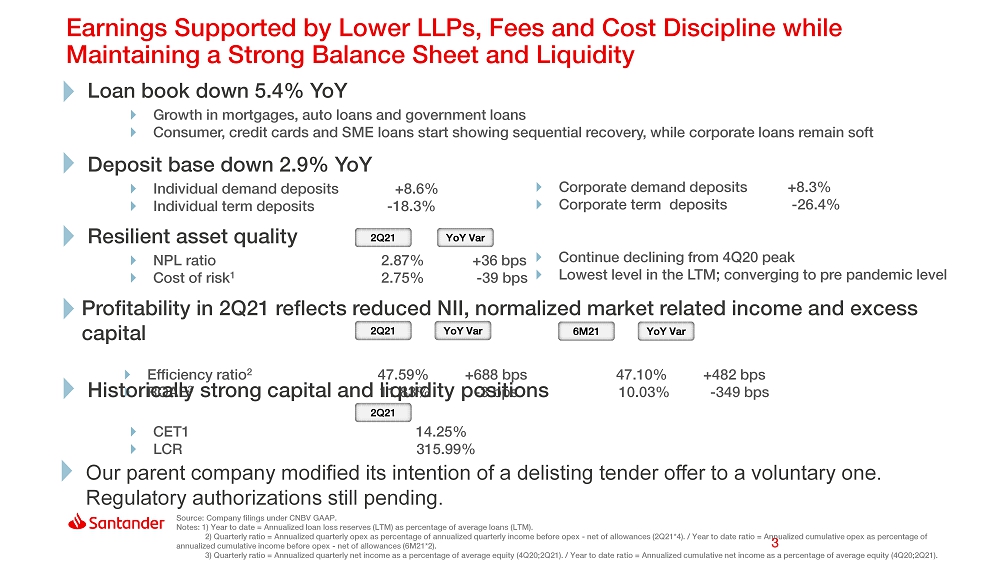

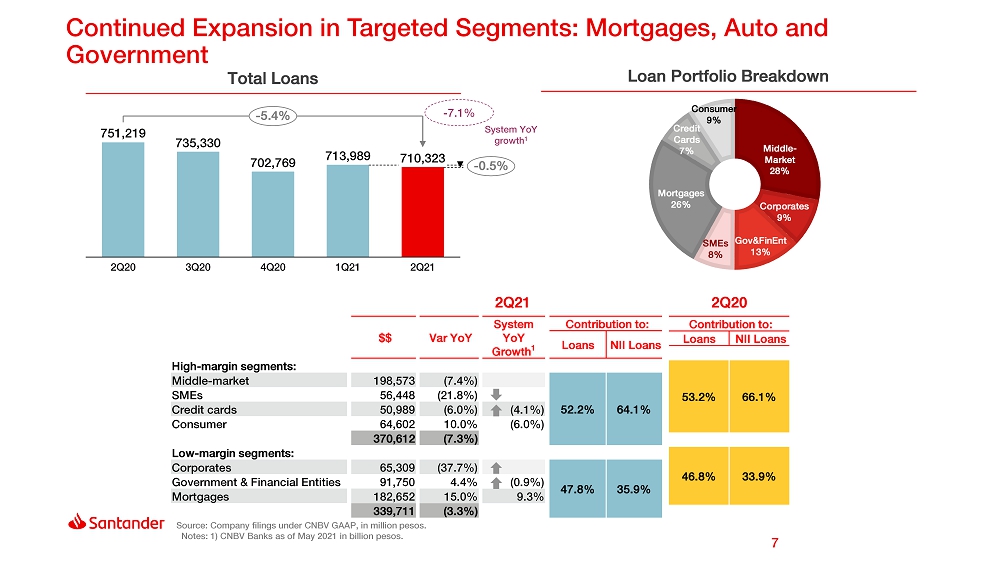

Banco Santander México’s total loan portfolio, as of June 2021, decreases 5.4% YoY, or Ps.40,896 million, to Ps.710,323 million, and 0.5%, or Ps.3,666 million, on a sequential basis.

During the quarter, the retail portfolio reflects solid performance, supported by mortgages and auto loans, while credit cards and personal loans remained weak. In addition, the commercial portfolio still faces a difficult comparison base as of June 2020, when companies drew on their committed lines of credit. As a result, the total loan portfolio contracted year over year.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 3 |

| |

| |

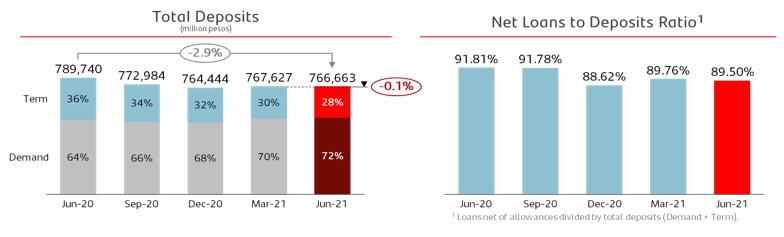

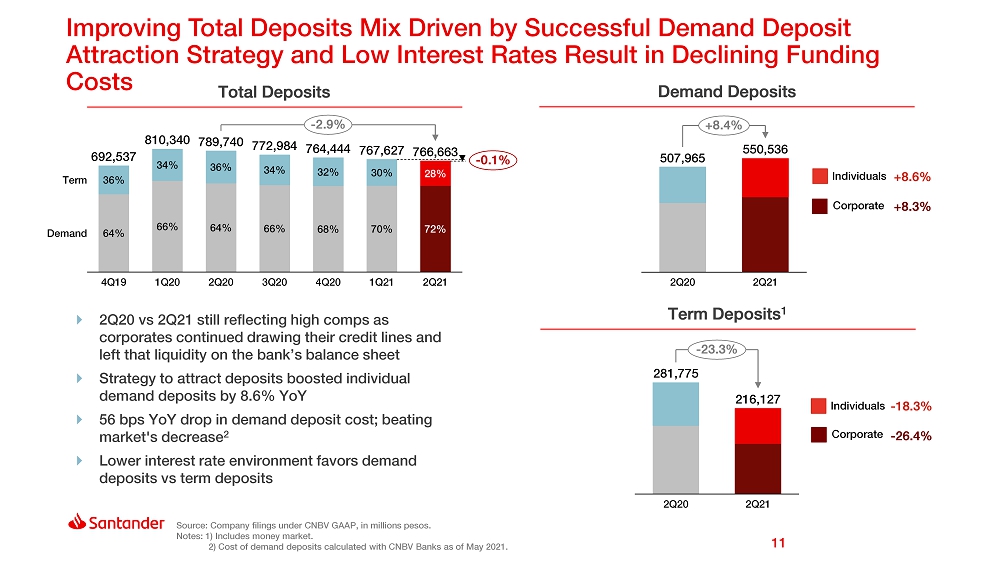

Deposits

Deposits, which represent 83.3% of Banco Santander México’s total funding1, decreased 2.9% YoY in June 2021, reflecting unusually high comps since March 2020, when corporates drew their committed lines of credit and left that liquidity on the Bank’s balance sheet, meanwhile deposits remained flat sequentially. In turn, demand deposits increased 8.4% YoY, while time deposits decreased 23.3% YoY, as lower interest rates made customers favor short term liquidity and supported by the Banks efforts to improve funding mix. On a sequential basis, demand deposits increased 2.2% while time deposits decreased 5.6%. It is worth noting that demand deposits from individuals grew 8.6% YoY, supported by the Bank ongoing efforts to attract these types of deposits, while demand deposits from corporates increased 8.3% YoY.

In June 2021, demand deposits from individuals represented 33.8% of total demand deposits, compared with 33.7% in June 2020. Time deposits from individuals represented 40.9% of total time deposits, compared with 38.4% a year ago.

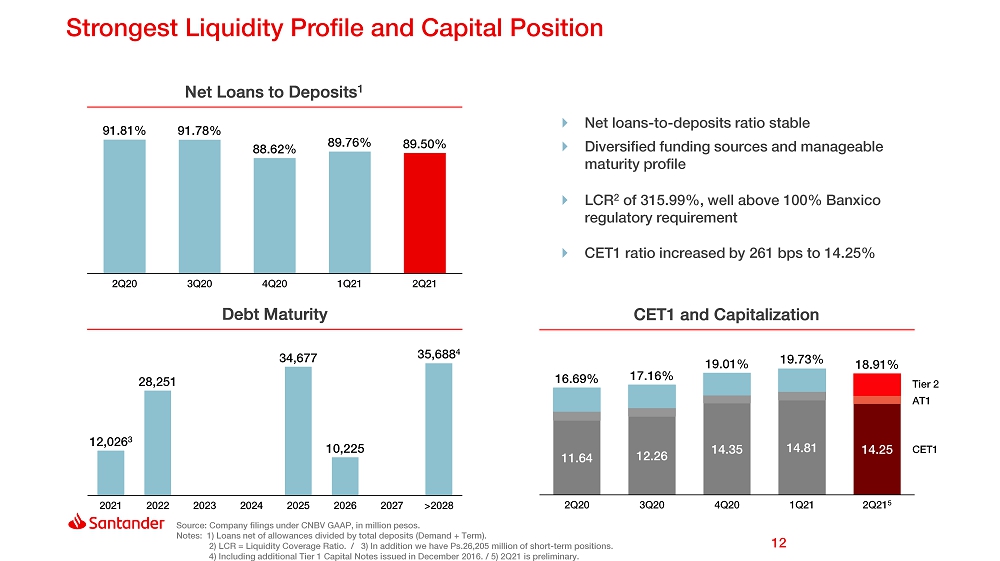

The loans-to-deposits ratio stood at 89.50% in June 2021, which compares to 91.81% in June 2020, and 89.76% in March 2021, maintaining a stable funding position.

Net income

Banco Santander México reported 2Q21 net income of Ps.4,713 million, representing increases of 11.4% YoY, and 43.7% QoQ, mainly due to lower provisions for loan losses, stable NII, solid growth in net commission and fee income and strict cost discipline. On a cumulative basis, net income for 6M21 reached Ps.7,992 million, representing a 17.1% YoY decrease.

1 Total funding includes: deposits, credit instruments issued, bank and other loans and subordinated credit notes.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 4 |

| |

| |

| Net income statement | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | 21/20 | ||||

| Net interest income | 15,770 | 15,585 | 15,931 | 1.2 | (1.0) | 31,355 | 32,827 | (4.5) | |||

| Provisions for loan losses | (5,068) | (7,075) | (8,350) | (28.4) | (39.3) | (12,143) | (13,515) | (10.2) | |||

| Net interest income after provisions for loan losses | 10,702 | 8,510 | 7,581 | 25.8 | 41.2 | 19,212 | 19,312 | (0.5) | |||

| Commission and fee income, net | 4,873 | 4,902 | 4,598 | (0.6) | 6.0 | 9,775 | 9,295 | 5.2 | |||

| Net gain (loss) on financial assets and liabilities | 817 | 1,398 | 3,283 | (41.6) | (75.1) | 2,215 | 4,166 | (46.8) | |||

| Other operating income | (542) | (664) | (232) | (18.4) | 133.6 | (1,206) | (444) | — | |||

| Administrative and promotional expenses | (9,955) | (9,894) | (9,599) | 0.6 | 3.7 | (19,849) | (19,384) | 2.4 | |||

| Operating income | 5,895 | 4,252 | 5,631 | 38.6 | 4.7 | 10,147 | 12,945 | (21.6) | |||

| Equity in results of associated companies | 50 | 77 | 35 | (35.1) | 42.9 | 127 | 39 | — | |||

| Operating income before income taxes | 5,945 | 4,329 | 5,666 | 37.3 | 4.9 | 10,274 | 12,984 | (20.9) | |||

| Income taxes (net) | (1,232) | (1,050) | (1,436) | 17.3 | (14.2) | (2,282) | (3,340) | (31.7) | |||

| Net income | 4,713 | 3,279 | 4,230 | 43.7 | 11.4 | 7,992 | 9,644 | (17.1) | |||

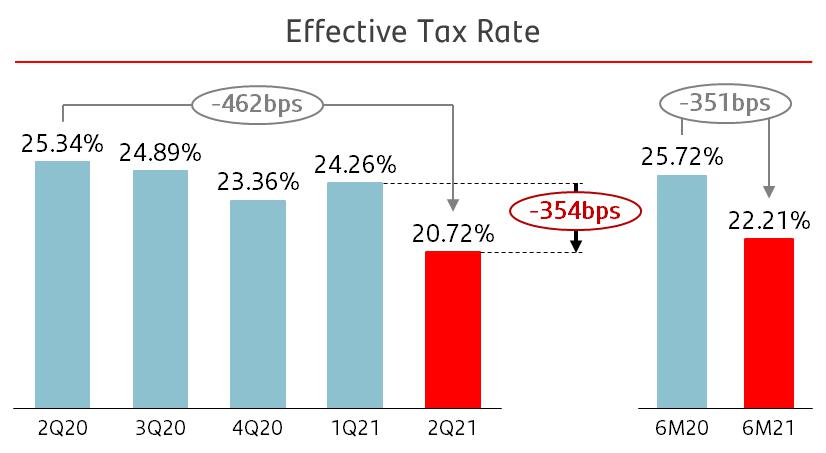

| Effective tax rate (%) | 20.72 | 24.26 | 25.34 | 22.21 | 25.72 | ||||||

2Q21 vs 2Q20

The 11.4% year-on-year increase in net income was principally driven by:

| i) | A 39.3%, or Ps.3,282 million, decrease in provisions for loan losses, reflecting easier comps, as the Bank made special charge of loan loss provisions in 2Q20 to face the COVID-19 pandemic; |

| ii) | A 6.0%, or Ps.275 million, increase in net commissions and fees, mainly due to increases in debit and credit card fees and insurance fees; |

| iii) | A 14.2%, or Ps.204 million, decrease in income taxes, which resulted in a 20.72% effective tax rate for the quarter, compared to 25.34% in 2Q20; and |

| iv) | A 42.9%, or Ps.15 million, increase in the results of associated companies due to the recognition of Elavon México investment. |

The increase in net income was partially offset by:

| i) | A 75.1%, or Ps.2,466 million, decrease in net gains on financial assets and liabilities, due to a higher base in 2Q20, due to extraordinary gains related to the sale of certain securities to strengthen the Bank liquidity position; |

| ii) | A 3.7%, or Ps.356 million, increase in administrative and promotional expenses, mainly due to increases in personnel expenses, depreciation and amortization and cash protection services, partly offset by decreases in other expenses and contributions to IPAB; |

| iii) | A 133.6%, or Ps.310 million, increase in other operating expenses, mostly resulting from lower cancellation of liabilities and reserves, higher write-offs, a decrease in other operating income, higher premiums paid on |

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 5 |

| |

| |

guarantees for the SMEs loan portfolio and higher legal expenses and costs related to portfolio recoveries; and

| i) | A 1.0%, or Ps.161 million, decrease in net interest income, reflecting lower interest rates and change in the loan portfolio mix. |

6M21 vs 6M20

The 17.1% year-on-year decrease in net income was principally driven by:

| i) | A 46.8%, or Ps.1,951 million, decrease in net gains on financial assets and liabilities, mostly resulting of a higher base in 6M20, due to extraordinary gains related to the sale of certain securities to strengthen the Bank liquidity position; |

| ii) | A 4.5%, or Ps.1,472 million, decrease in net interest income, reflecting lower interest rates and change in the loan portfolio mix; |

| iii) | A Ps.762 million, increase in other operating expenses, mostly resulting from higher legal expenses and costs related to portfolio recoveries, lower profit from sale of foreclosed assets, a decrease in cancellation of liabilities and reserves, higher write-offs and higher premiums paid on guarantees for the SMEs loan portfolio; and |

| iv) | A 2.4%, or Ps.465 million, increase in administrative and promotional expenses, mainly due to increases in personnel expenses, depreciation and amortization and technology services expenses, partly offset by decreases in other expenses, promotional and advertising expenses, leasehold expenses and taxes and duties. |

The decrease in net income was partially offset by:

| i) | A 10.2%, or Ps.1,372 million, decrease in provisions for loan losses, reflecting easier comps, as the Bank made special charge of loan loss provisions during 6M20 to face the COVID-19 pandemic; |

| ii) | A 31.7%, or Ps.1,058 million, decrease in income taxes, which resulted in a 22.21% effective tax rate in 6M21, compared to 25.72% in 6M20; |

| iii) | A 5.2%, or Ps.480 million, increase in net commissions and fees, mainly due to increases in debit and credit card fees and insurance fees; and |

| iv) | A Ps.88 million, increase in the results of associated companies due to the recognition of Elavon México investment |

Gross operating income

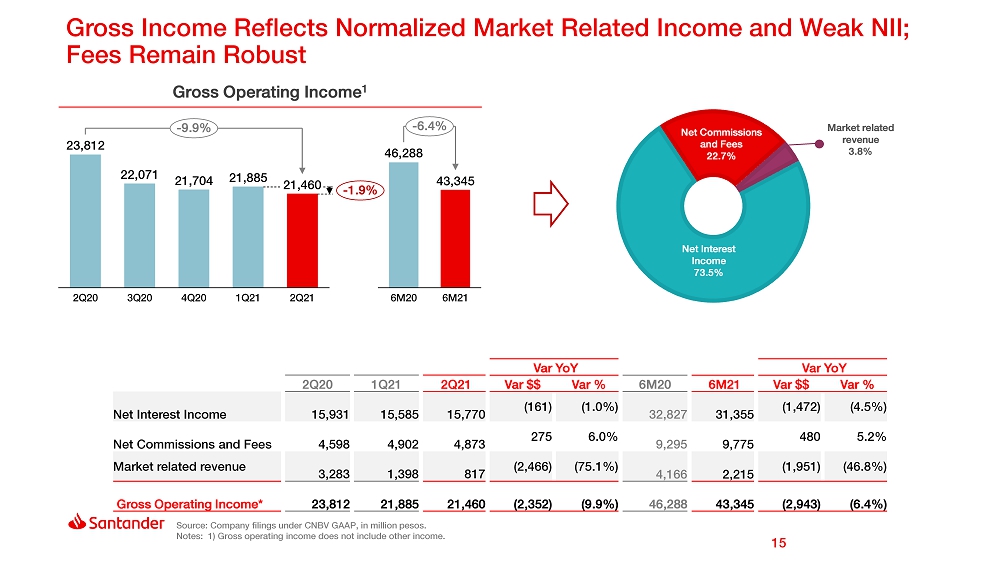

Banco Santander México’s gross operating income for 2Q21 totaled Ps.21,460 million, representing decreases of 9.9% YoY, or Ps.2,352 million, and 1.9% QoQ, or Ps.425 million, due to a more normalized result in market related income, partially offset by a solid increase in net commissions and fees. Gross operating income for 6M21 amounted Ps.43,345 million, decreasing 6.4% YoY, or Ps.2,943 million.

Gross operating income is broken down as follows.

| Breakdown gross operating Income (%) | |||||||||||

| Variation (bps) | Variation (bps) | ||||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | YoY | ||||

| Net Interest Income | 73.49 | 71.21 | 66.90 | 228 | 659 | 72.34 | 70.92 | 142 | |||

| Net Commissions and Fees | 22.71 | 22.40 | 19.31 | 31 | 340 | 22.55 | 20.08 | 247 | |||

| Market related revenue | 3.80 | 6.39 | 13.79 | (259) | (999) | 5.11 | 9.00 | (389) | |||

| Gross Operating Income* | 100.00 | 100.00 | 100.00 | 100.00 | 100.00 | ||||||

*Does not include other income

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 6 |

| |

| |

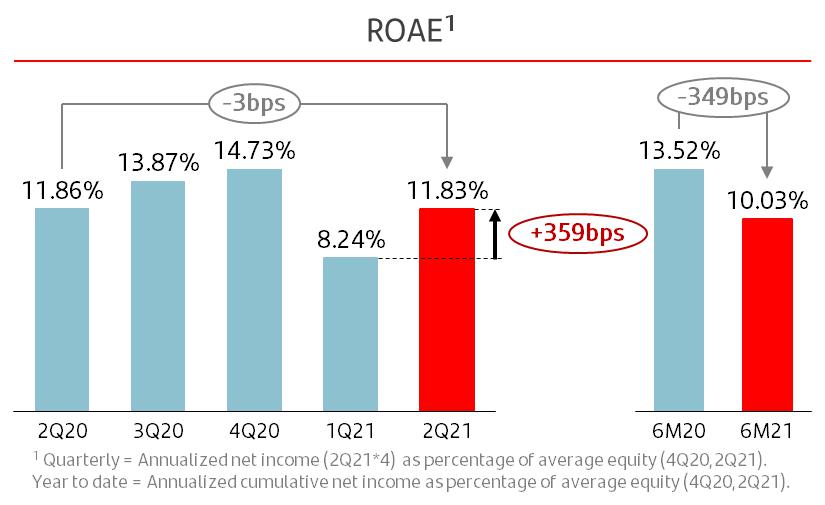

Return on average equity (ROAE)

ROAE for 2Q21 decreased 3 basis points to 11.83%, from 11.86% reported in 2Q20 and increased 359 basis points from 8.24% in 1Q21. For 6M21, ROAE stood at 10.03%, 349 basis points lower than the 13.52% reported in 6M20. The Bank is accumulating capital per regulator’s recommendation to limit the pay out dividend of 2019 and 2020 earnings.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 7 |

| |

| |

Strategic initiatives and commercial actions

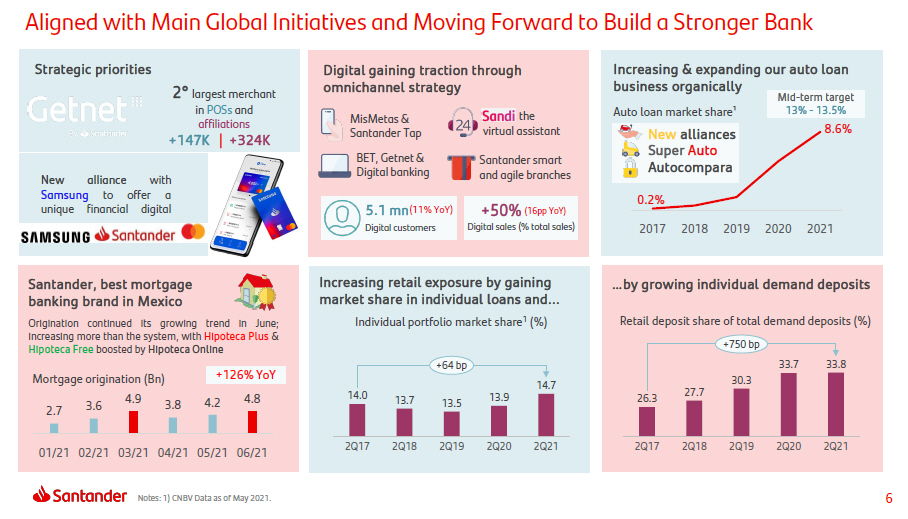

Banco Santander Mexico is one of the leading financial institutions in the country, focused on business transformation and innovation. The Bank's strategic priority is to become the best bank in customer experience, taking advantage of new tools and improving processes in order to accelerate technological transformation and digitalization, while increasing its capacity to improve the operating model and information security. Likewise, the Bank keeps strengthen its customer base to continue positioning itself as a market leader in value-added products to attract potential customers and increase loyalty.

The most relevant aspects of the second quarter are highlighted below:

| Ø | The Bank’s strategic priorities are complemented by a new range of products and services, which will allow to cater its customers more comprehensively. |

| § | Samsung, Santander México and Mastercard, leading companies in their respective sectors, announced a joint venture seeking to improve users' banking experiences through Members Wallet , a digital wallet that integrates all Santander services into the Samsung ecosystem, such as security, financing, payments and inquiries of balance and movements. Likewise, it is complemented by a Samsung Members debit card, which offers exclusive benefits for customers. The card provides innovative, easy and secure payment experiences through functions such as the dynamic and unique security code for online purchases, an "Infoless" card to protect customer data, and contactless payment technology, among others. It is worth to mention that Samsung is the biggest seller of mobile phones in Mexico with more than 30% market share. |

| § | In line with Santander Group’s strategy, Banco Santander México is working on the transformation of the collections and payments industry through “PagoNxt”. As part of this initiative, the bank re-launched its merchant business through GetNet México. Currently, GetNet México is the second largest merchant in POSs and affiliations in the market, and third in number of transactions processed through the acquirer. In this respect, the bank is developing new solutions to increase acceptance of the non-present card channel, adapting to the “new normality” and expecting to become the second most relevant player by the end of the year. |

| § | The bank is working on a new credit card value proposition based on three main matters (i) security and digital experience (ii) personalization and (iii) social responsibility. This innovative product includes enhanced security features, a digital and integrated experience, zero annual fee, and the possibility of customize benefits on a tailor made model. |

| § | Santander signed a commercial alliance with Farmacias del Ahorro chain to add its close to 1,500 establishments to the more than 28,500 service points that the bank currently has. These will allow the clients to make credit card payments or debit card deposits up to Ps. 20,000 per account per day at their nearest pharmacy, and the cost per operation will be 10 pesos. The incorporation of Farmacias del Ahorro as Santander's banking correspondent will complement the branch network by supporting financial inclusion, bringing banking services to unbanked and rural areas. |

| § | Global Brands Magazine, a magazine specialized in news and surveys on the world's leading brands, identified Banco Santander México as a benchmark in the mortgage market in the country, Santander is the only bank in Mexico that offers an interest rate tailored made based on customer profile. As a result, the bank is one of the leading mortgage originators in the market. |

| § | Santander México and the Business Center of Mexico City (COPARMEX CDMX by its acronym in Spanish) announced an alliance to benefit more than 5,000 associated companies with loans and other products, in order to support them in their growth and development with banking products and preferential rates. These loans can be requested in just 15 minutes in an agile, simple and completely digitally. |

| § | Santander Asset Management México launched its second equity fund with environmental, social and governance criteria together with Robeco Institutional Asset Management (Robeco). The new ESG Global Equity Fund (SAM-RVG) has an international focus and invests in shares of companies around the world with high return on capital, attractive value, ESG criteria and where the performance of the company is prioritized before the region where it is located, which differentiates this product from other funds available in the country. |

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 8 |

| |

| |

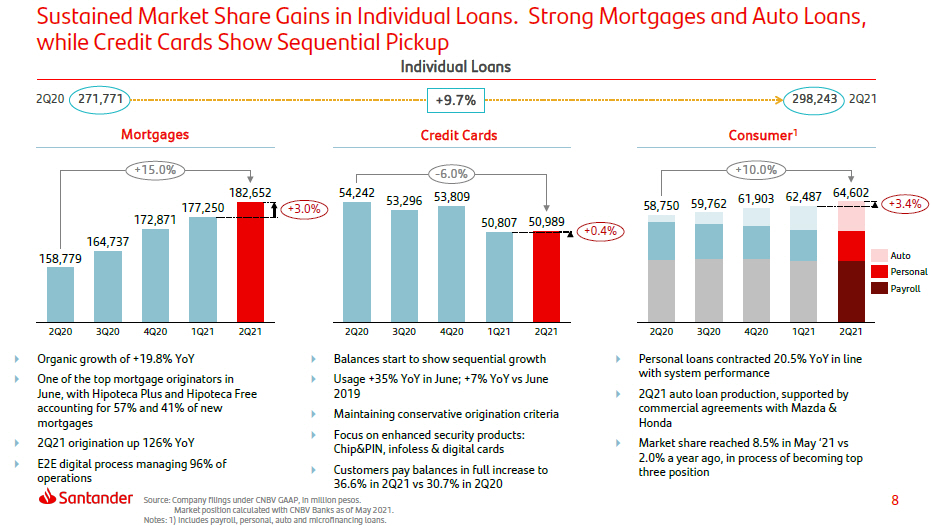

| § | This quarter, Santander moved up in the rankings and reached the 4th position in auto loans with 8.6% market share as of May. All this, thanks to the alliances that the bank has with Honda, Mazda, Tesla, Suzuki and Peugeot, together with Super Auto Santander platform that integrates the commercial and insurance offering in one place, allowing to offer an online pre-approval in less than 10 minutes, letting customers to have a brand-new car in less than 24 hours. |

| § | The consolidation of the Hipoteca Online digital platform continued, being the only platform in Mexico that connects all processes from end to end. In the quarter, the platform processed 96% of operations digitally, which helped the Bank consolidate as the second leading mortgage originator in the market; around 57% of originations came through Hipoteca Plus, which helps to drive cross-selling products, and 41% through Hipoteca Free. Santander continues to be the only bank in Mexico that offers a tailored interest rate based on the client's profile. |

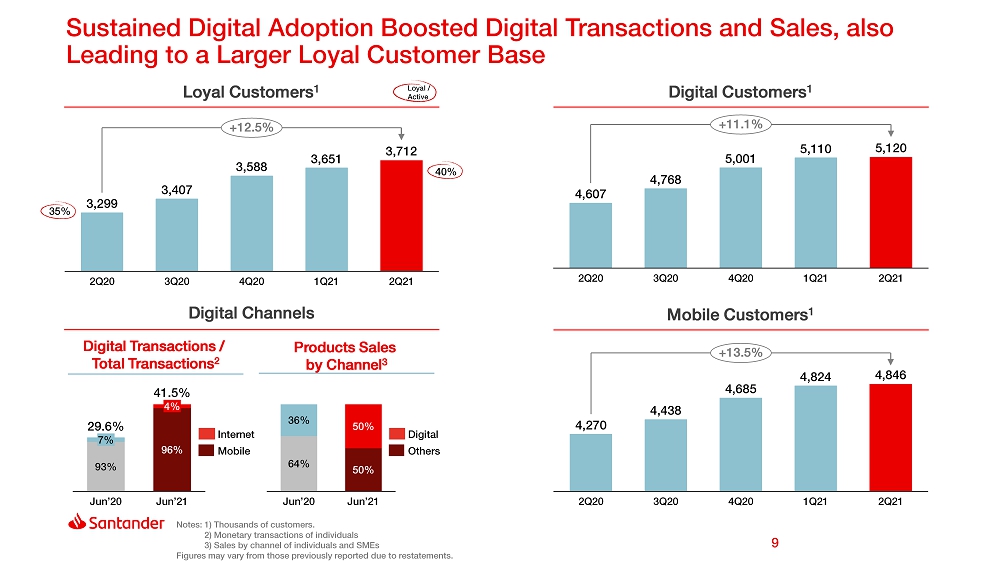

| § | The Bank continues to increase the number of its digital and mobile clients by 11% and 14% YoY, respectively. Moreover, the ratio of loyal customers continues to grow, now loyal clients represent 40% of active clients (vs 35% in the second quarter of 2020). In addition, digital transactions now account for almost 42% of total transactions, increasing from 30% compared to June 2020. As of June 2021, 50% of product sales were made through digital channels, compared to 36% a year ago. |

| Customers | ||||||

| (Thousands) | % Variation | |||||

| Jun-21 | Mar-21 | Jun-20 | QoQ | YoY | ||

| Loyal Customers1 | 3,712 | 3,651 | 3,299 | 1.7 | 12.5 | |

| Digital Customers2 | 5,120 | 5,110 | 4,607 | 0.2 | 11.1 | |

| Mobile Customers3 | 4,846 | 4,824 | 4,270 | 0.4 | 13.5 | |

| 1 | Loyal customers = Clients with non-zero balance and depending on the segment should have between two and four products and between three and ten transactions in the last 90 days. |

| 2 | Digital customers = Clients with at least one digital transaction per month in SuperNet or SuperMóvil. |

| 3 | Mobile customers = Clients using Supermóvil and/or Superwallet in the last 30 days. |

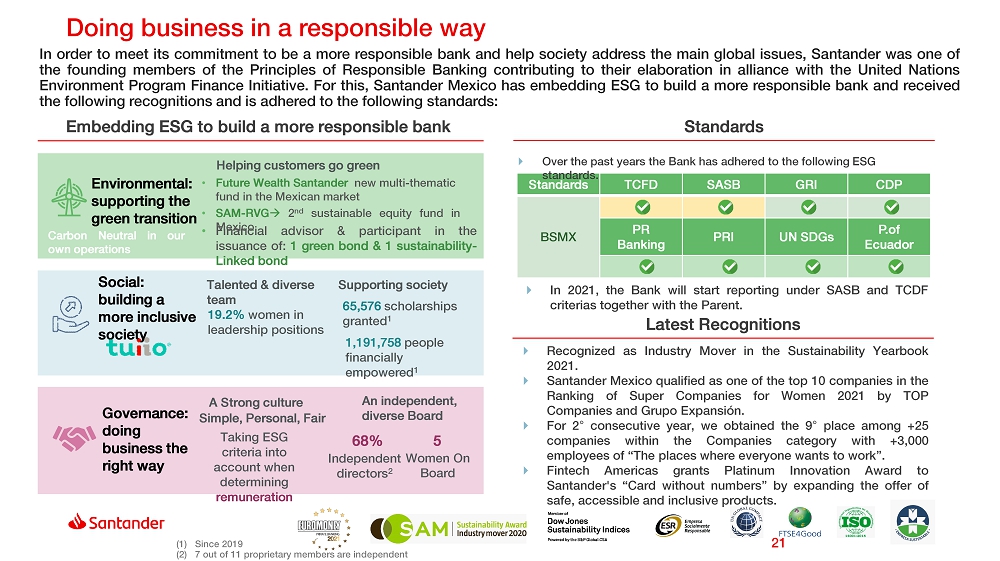

Responsible Banking

Santander has a strong commitment to financial inclusion, poverty reduction, care for the environment and the comprehensive well-being of the communities in which it operates.

It has initiatives that promote education, entrepreneurship, gender equality and social well-being. In addition, it allocates a significant amount of human and material resources in support of these causes.

The Bank seeks to become a leading participant in contributing to the progress of people and companies in Mexico. On this regard, it works on two main challenges: New Business Environment and Inclusive and Sustainable Growth.

The objective of the New Business Environment is for Santander employees to feel in a responsible, simple, diverse and inclusive work environment, where leadership and commitment follow the Simple, Personal and Fair culture, while designing products focused on customers.

The goal to achieve an Inclusive and Sustainable Growth aims to invest in the Bank’s community, financially empowering people, supporting higher education through scholarships and leaving a minimal environmental footprint while incentivizing ESG products across all business units.

In 2018, the Group defined eleven commitments to fulfill in the coming years. For more details, please visit the Responsible Banking section in the investor relations website.

As a result of these efforts, Banco Santander Mexico has achieved the following recognitions:

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 9 |

| |

| |

| § | In July 2021, International Finance Magazine (IFM) recognized Santander as the Best Financial Inclusion Bank and as the Most Socially Responsible Bank in Mexico. |

| § | In July 2021, Santander México qualified as one of the top 10 companies in the Ranking of Super Companies for Women 2021 by TOP Companies and Grupo Expansión. |

| § | In July 2021, Santander Investment Banking México was recognized by Euromoney as the Best Investment Bank in the country. |

| § | In May 2021, for second consecutive year, the Bank obtained the 9th place among +25 companies within the companies category with more than 3,000 employees of “The places where everyone wants to work”. |

| § | In May 2021, Santander Mexico was recognized within a LinkedIn ranking of the 25 companies to develop a career in Mexico. |

| § | In May 2021, Fintech Americas grants Platinum Innovation Award to Santander's “Card without numbers” by expanding the offer of safe, accessible and inclusive products. |

| § | Santander México is the only bank in the country included in the S&P “Sustainability Yearbook 2021”. |

| § | In 2021, Tuiio by Santander was recognized by the Mexico Global Pact office as an outstanding practice to end poverty in Mexico, one of the 17 Sustainable Development Goals proposed by the 2030 Agenda of the United Nations. |

| § | In 2021, Laura Diez Barroso, Chairman of the Board of Directors of Santander México, was named as one of "The 100 most powerful women in business" by Expansión within the framework of International Women's Day. In addition, Mrs. Diez Barroso participated in the signing of the commitment of banking to reduce the gender gap in the financial system in Mexico. |

| § | In 2020, it was included in the Dow Jones Sustainability Indices for its outstanding performance in sustainability in Latin America. |

| § | Also in 2020, it was included as constituted on the new S&P/BMV Total Mexico ESG Index, that replaced the IPC Sustainability Index, of which the Bank was part for seven consecutive years since 2013. |

| § | Included on the FTSE4Good Index since 2018. |

| § | Santander Private Banking, Best Private Banking according to Euromoney since 2017. |

| § | Member of the United Nations Global Compact since 2012. |

| § | Santander Mexico holds an ISO 14001:2015 certification since 2004. |

| § | It has a Responsible Banking recognition since 2004 by ESR (Empresa Socialmente Responsible by its acronym in Spanish). |

These indexes and recognitions evaluate the Bank’s performance across economic, environmental and social issues.

|

|

|

|

|

|

|

|

These are only some examples of the Bank’s effort to become a more responsible bank. For further information about Banco Santander México as a Responsible Bank go to:

https://servicios.santander.com.mx/comprometidos/eng/index.php

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 10 |

| |

| |

IV. Analysis of 2Q21 Consolidated Results

(Amounts expressed in millions of pesos, except where otherwise stated)

Loan portfolio

The evolution of the loan portfolio showed a contraction in an annual basis, mainly in the commercial portfolio, which still faces a difficult comparison base as of June 2020, when companies drew on their committed lines of credit, while credit cards and personal loans remained weak, these contractions were partially offset by the solid performance shown in the retail portfolio, on the back of mortgages and auto loans.

| Portfolio Breakdown | ||||||

| Million pesos | % Variation | |||||

| Jun-21 | Mar-21 | Jun-20 | QoQ | YoY | ||

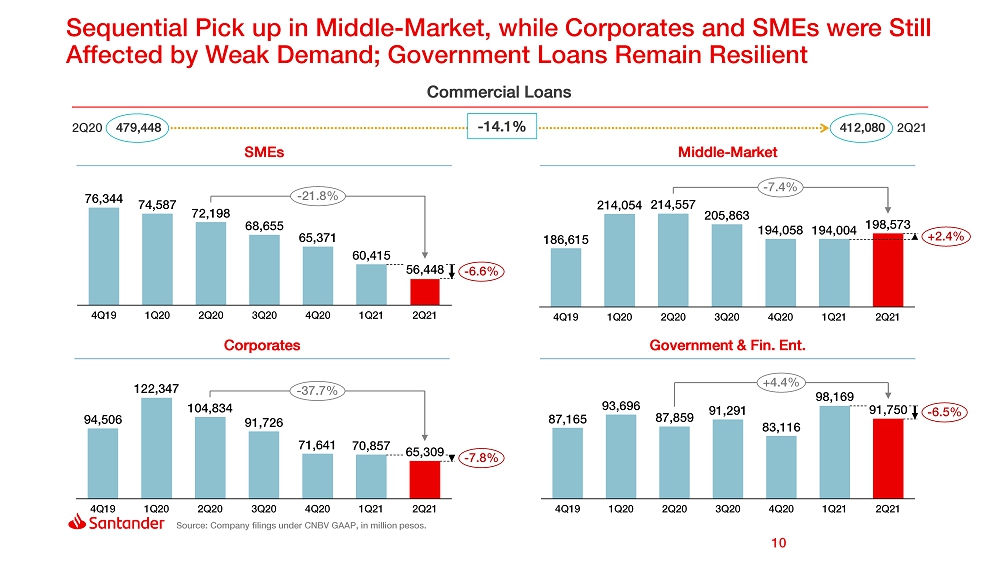

| Commercial | 412,080 | 423,445 | 479,448 | (2.7) | (14.1) | |

| Middle-market | 198,573 | 194,004 | 214,557 | 2.4 | (7.4) | |

| Corporates | 65,309 | 70,857 | 104,834 | (7.8) | (37.7) | |

| SMEs | 56,448 | 60,415 | 72,198 | (6.6) | (21.8) | |

| Government & Financial Entities | 91,750 | 98,169 | 87,859 | (6.5) | 4.4 | |

| Individuals | 298,243 | 290,544 | 271,771 | 2.6 | 9.7 | |

| Consumer | 115,591 | 113,294 | 112,992 | 2.0 | 2.3 | |

| Credit cards | 50,989 | 50,807 | 54,242 | 0.4 | (6.0) | |

| Other consumer | 64,602 | 62,487 | 58,750 | 3.4 | 10.0 | |

| Mortgages | 182,652 | 177,250 | 158,779 | 3.0 | 15.0 | |

| Total | 710,323 | 713,989 | 751,219 | (0.5) | (5.4) | |

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 11 |

| |

| |

Total loan portfolio declined 5.4% YoY, or Ps.40,896 million, to Ps.710,323 million in June 2021. On a sequential basis, total loan portfolio decreased 0.5%, or Ps.3,666 million.

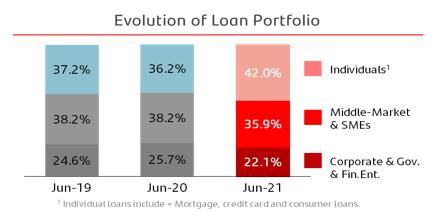

The commercial loan portfolio is comprised of loans to business and commercial entities, as well as loans to government entities and financial institutions, and represented 58.0% of the total loan portfolio. Excluding loans to government entities and financial institutions, the commercial loan portfolio accounted for 45.1% of the total. Middle-market, Corporate and SME loans represented 28.0%, 9.2% and 7.9% of the total loan portfolio, respectively.

The individuals loan portfolio, comprised of mortgages, consumer and credit card loans, represented 42.0% of the total loan portfolio. Mortgage, consumer and credit card loans, represented 25.7%, 9.1% and 7.2% of the total loan portfolio, respectively.

| Loan portfolio breakdown | ||||||||

| Million pesos | ||||||||

| Jun-21 | % | Mar-21 | % | Jun-20 | % | |||

| Performing loans | ||||||||

| Commercial | 405,407 | 57.1 | 416,942 | 58.4 | 472,748 | 62.9 | ||

| Individuals | 284,515 | 40.1 | 276,287 | 38.7 | 259,627 | 34.6 | ||

| Consumer | 110,756 | 15.6 | 107,758 | 15.1 | 108,292 | 14.4 | ||

| Credit cards | 48,339 | 6.8 | 47,641 | 6.7 | 51,628 | 6.9 | ||

| Other consumer | 62,417 | 8.8 | 60,117 | 8.4 | 56,664 | 7.5 | ||

| Mortgages | 173,759 | 24.5 | 168,529 | 23.6 | 151,335 | 20.1 | ||

| Total performing loans | 689,922 | 97.1 | 693,229 | 97.1 | 732,375 | 97.5 | ||

| Non-performing loans | ||||||||

| Commercial | 6,673 | 0.9 | 6,503 | 0.9 | 6,700 | 0.9 | ||

| Individuals | 13,728 | 1.9 | 14,257 | 2.0 | 12,144 | 1.6 | ||

| Consumer | 4,835 | 0.7 | 5,536 | 0.8 | 4,700 | 0.6 | ||

| Credit cards | 2,650 | 0.4 | 3,166 | 0.4 | 2,614 | 0.3 | ||

| Other consumer | 2,185 | 0.3 | 2,370 | 0.3 | 2,086 | 0.3 | ||

| Mortgages | 8,893 | 1.3 | 8,721 | 1.2 | 7,444 | 1.0 | ||

| Total non-performing loans | 20,401 | 2.9 | 20,760 | 2.9 | 18,844 | 2.5 | ||

| Total loan portfolio | ||||||||

| Commercial | 412,080 | 58.0 | 423,445 | 59.3 | 479,448 | 63.8 | ||

| Individuals | 298,243 | 42.0 | 290,544 | 40.7 | 271,771 | 36.2 | ||

| Consumer | 115,591 | 16.3 | 113,294 | 15.9 | 112,992 | 15.0 | ||

| Credit cards | 50,989 | 7.2 | 50,807 | 7.1 | 54,242 | 7.2 | ||

| Other consumer | 64,602 | 9.1 | 62,487 | 8.8 | 58,750 | 7.8 | ||

| Mortgages | 182,652 | 25.7 | 177,250 | 24.8 | 158,779 | 21.1 | ||

| Total loan portfolio | 710,323 | 100.0 | 713,989 | 100.0 | 751,219 | 100.0 |

As of June 2021, commercial loans decreased 14.1% YoY, or Ps.67,368 million, driven by corporate, middle-market, SMEs and financial institutions loans, which decreased 37.7% YoY, or Ps.39,526 million, 7.4% YoY, or Ps.15,983 million, 21.8% YoY, or Ps.15,751 million and 24.0% YoY, or Ps.3,142 million, respectively. Meanwhile, government entities loans increased 9.4% YoY, or Ps.7,033 million. Sequentially, commercial

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 12 |

| |

| |

loans decreased 2.7% or Ps.11,365 million. The YoY decrease still reflected the exceptionally high comps of 2020, when corporate and mid-market loans increased significantly in the first half of 2020. At the time, companies drew on their committed lines of credit in the face of uncertainty caused by the COVID-19 pandemic.

Mortgage loans continued showing robust growth, increasing 15.0% YoY, or Ps.23,873 million and 3.0%, or Ps.5,402 million sequentially. The “Hipoteca Plus” product remains a main driver behind this strong performance, accounting for 57% of total mortgage origination in the quarter, which also helps the Bank to increase cross-selling of other products, mainly insurance and credit cards, supporting fee income growth and build customer loyalty. In addition, the digital onboarding platform for mortgages, “Hipoteca Online”, has been key during the COVID-19 pandemic, as it helps streamline processes and eliminates the need to visit a branch. During 2Q21, 96% of the mortgages were processed through this digital platform. However, the total mortgage loan portfolio is still affected by the run-off of acquired portfolios, excluding this effect, the mortgage portfolio would have increased 19.8% YoY, almost twice as much as the market growth.

It is worth noting that auto loans showed a solid performance, increasing 4.0x in June 2021 with respect to June 2020 and a 24.7%, or Ps.2,678 million, sequentially. This was a result of the Bank alliances with leading automakers, the most recent addition being Honda, which is producing excellent results together with the alliances that already the Bank had with Mazda, Suzuki, Peugeot and Tesla, among others. According to the last information published by CNBV, as of May 2021, market share in this business was 8.5% vs. 2.0% a year ago.

Credit card loans contracted 6.0% YoY, or Ps.3,253 million, and increased 0.4% QoQ, or Ps.182 million, despite an average usage increase of 35% YoY, although a decrease of 3% QoQ, while, personal and payroll loans decreased 20.5% YoY, or Ps.3,830 million, and 1.5% YoY, or Ps.538 million, respectively, affected by weak demand conditions.

Total Deposits

Total deposits in June 2021 stood at Ps.766,663 million, a decrease of 2.9% YoY, or Ps.23,077 million, reflecting unusually high comps since March 2020, when corporates drew their credit lines and left that liquidity on the Bank’s balance sheet. On a sequential basis, total deposits remained flat. Demand deposits reached Ps.550,536 million, increasing 8.4% YoY, or Ps.42,571 million, while time deposits decreased 23.3% YoY, or Ps.65,648 million, as lower interest rates made customers favor short term liquidity and supported by the Banks efforts to improve funding mix. In turn, demand deposits increased 2.2%, or Ps.11,907 million, sequentially, while time deposits decreased 5.6% QoQ, or Ps.12,871 million. Deposits from individuals contracted 1.9% YoY, or Ps.5,183 million, and from corporates contracted 3.5% YoY, or Ps.17,894 million. The Bank continues working on the strategy focused on prioritizing individual deposits and foregoing certain expensive corporate deposits.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 13 |

| |

| |

Net interest income

| Net interest income | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | 21/20 | ||||

| Interest on funds available | 369 | 371 | 609 | (0.5) | (39.4) | 740 | 1,326 | (44.2) | |||

| Interest on margin accounts | 64 | 61 | 104 | 4.9 | (38.5) | 125 | 274 | (54.4) | |||

| Interest and yield on securities | 5,735 | 6,243 | 6,217 | (8.1) | (7.8) | 11,978 | 12,671 | (5.5) | |||

| Interest and yield on loan portfolio – excluding credit cards | 14,871 | 14,804 | 17,623 | 0.5 | (15.6) | 29,675 | 35,806 | (17.1) | |||

| Interest and yield on loan portfolio related to credit cards | 3,057 | 2,911 | 3,507 | 5.0 | (12.8) | 5,968 | 7,357 | (18.9) | |||

| Commissions collected on loan originations | 145 | 142 | 127 | 2.1 | 14.2 | 287 | 266 | 7.9 | |||

| Interest and premium on sale and repurchase agreements and securities loans | 857 | 567 | 1,196 | 51.1 | (28.3) | 1,424 | 2,530 | (43.7) | |||

| Interest income | 25,098 | 25,099 | 29,383 | (0.0) | (14.6) | 50,197 | 60,230 | (16.7) | |||

| Daily average interest-earnings assets | 1,395,784 | 1,410,705 | 1,423,671 | (1.1) | (2.0) | 1,403,245 | 1,332,120 | 5.3 | |||

| Interest from customer deposits – demand deposits | (1,869) | (1,572) | (2,583) | 18.9 | (27.6) | (3,441) | (5,006) | (31.3) | |||

| Interest from customer deposits – time deposits | (2,065) | (2,352) | (4,402) | (12.2) | (53.1) | (4,417) | (8,823) | (49.9) | |||

| Interest from credit instruments issued | (1,177) | (1,233) | (1,256) | (4.5) | (6.3) | (2,410) | (2,055) | 17.3 | |||

| Interest on bank and other loans | (484) | (510) | (946) | (5.1) | (48.8) | (994) | (1,976) | (49.7) | |||

| Interest on subordinated capital notes | (411) | (419) | (478) | (1.9) | (14.0) | (830) | (891) | (6.8) | |||

| Interest and premium on sale and repurchase agreements and securities loans | (3,322) | (3,428) | (3,787) | (3.1) | (12.3) | (6,750) | (8,652) | (22.0) | |||

| Interest expense | (9,328) | (9,514) | (13,452) | (2.0) | (30.7) | (18,842) | (27,403) | (31.2) | |||

| Daily average interest-bearing liabilities | 1,250,767 | 1,265,176 | 1,269,580 | (1.1) | (1.5) | 1,257,958 | 1,192,162 | 5.5 | |||

| Net interest income | 15,770 | 15,585 | 15,931 | 1.2 | (1.0) | 31,355 | 32,827 | (4.5) | |||

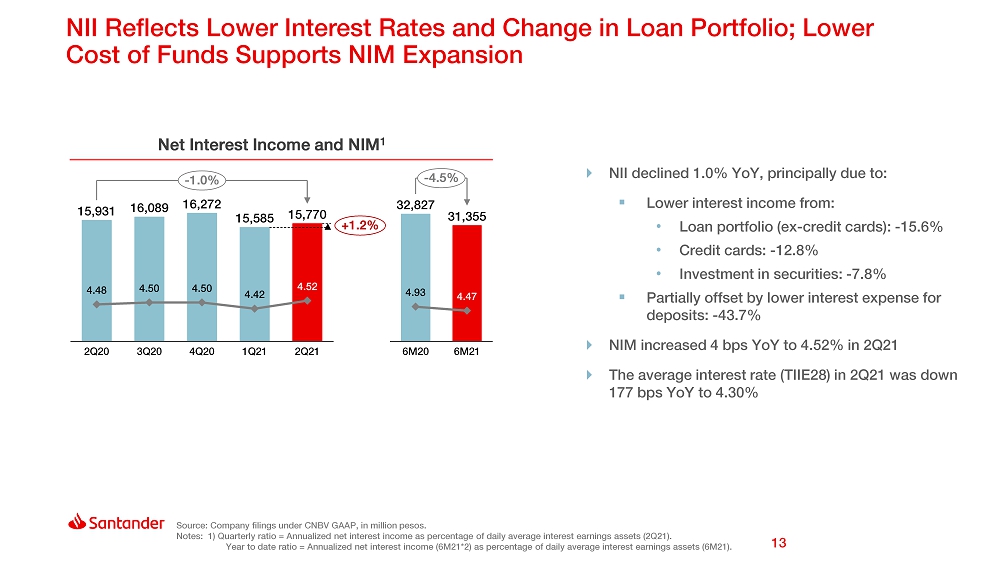

Net interest income in 2Q21 totaled Ps.15,770 million, decreasing 1.0% YoY, or Ps.161 million, and increasing 1.2% QoQ, or Ps.185 million.

The 1.0% YoY decrease in net interest income resulted from the combination of:

| i) | A 14.6%, or Ps.4,825 million, decrease in interest income, to Ps.25,098 million, which resulted from the combined effect of a 105 basis points decrease in the average interest rate received and a 2.0%, or Ps.27,887 million, decrease in average interest-earning assets; and |

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 14 |

| |

| |

| ii) | A 30.7%, or Ps.4,124 million, decrease in interest expense, to Ps.9,328 million, stemming from a 124 basis points decrease in the average interest rate paid and a 1.5%, or Ps.18,813 million, decrease in interest-bearing liabilities. |

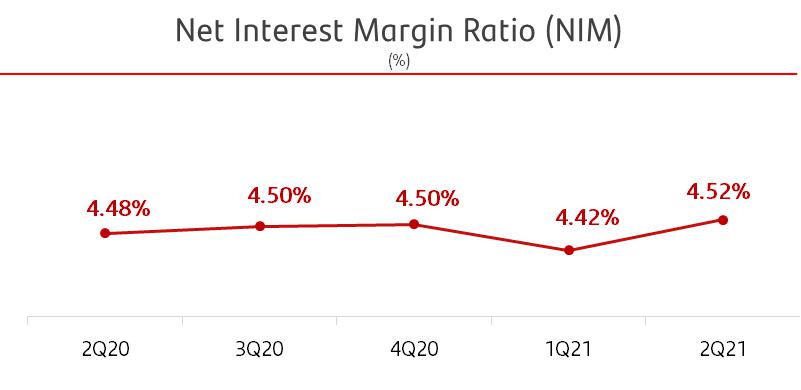

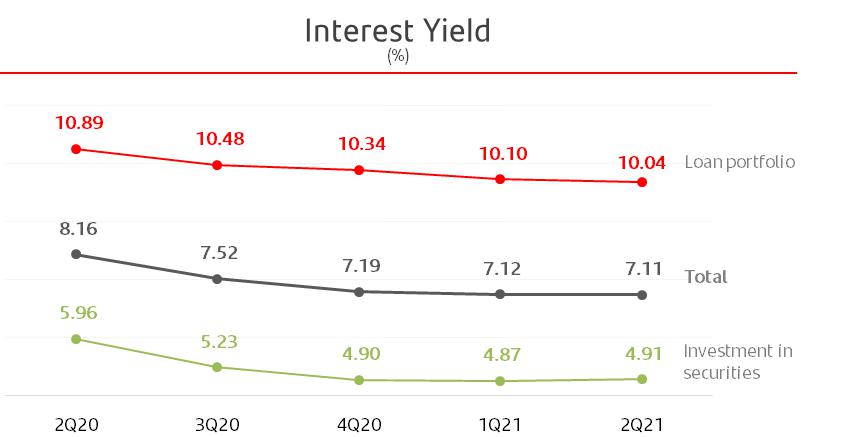

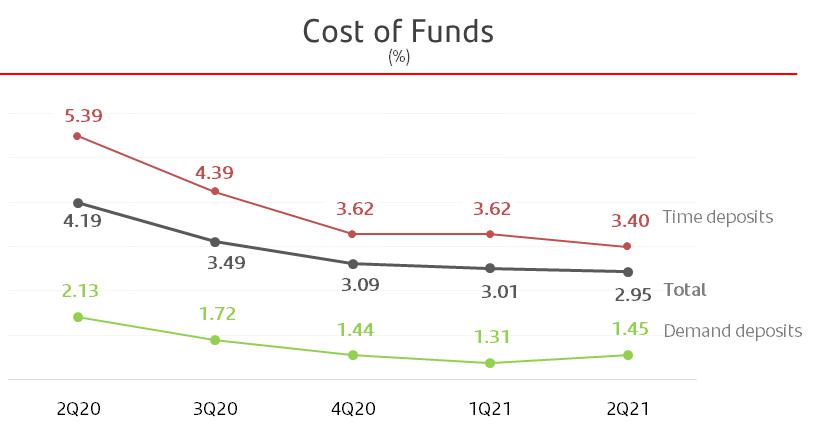

The net interest margin ratio (NIM), calculated using daily average interest-earning assets for 2Q21, stood at 4.52%, compared to 4.48% in 2Q20 and 4.42% in 1Q21. The increase in NIM mainly reflected a combination of lower contribution of loans to yielding assets and lower deposit cost. On a cumulative basis, NIM for 6M21 reached 4.47%, a decrease of 46 basis points from 6M20.

Interest Income

Total average interest earning assets in 2Q21 amounted to Ps.1,395,784 million, decreasing 2.0% YoY, or Ps.27,887 million, mainly driven by decreases of 7.9% YoY, or Ps.60,927 million, in the average loan portfolio, and a 58.8%, or Ps.27,333 million, in margin accounts, partly offset by a 12.1% growth, or Ps.49,958 million, in the average amount of investment in securities, by 5.2% growth, or Ps.6,007 million, in funds available, and by 5.4% increase, or Ps.4,408 million, in repurchase agreements. Banco Santander México’s interest earning assets are broken down as follows:

| Average Assets (Interest-Earnings Assets) | |||||

| Breakdown (%) | |||||

| 2Q20 | 3Q20 | 4Q20 | 1Q21 | 2Q21 | |

| Loan portfolio | 53.9 | 51.6 | 49.2 | 49.7 | 50.6 |

| Investment in securities | 29.0 | 32.8 | 35.4 | 36.3 | 33.1 |

| Funds available | 8.2 | 8.4 | 8.8 | 8.1 | 8.8 |

| Repurchase agreements | 5.7 | 4.3 | 4.3 | 3.9 | 6.1 |

| Margin accounts | 3.3 | 3.0 | 2.3 | 2.0 | 1.4 |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Banco Santander México’s interest income consists mainly of interest from the loan portfolio and commissions on loan originations, which in 2Q21 generated Ps.18,073 million and accounted for 72.0% of total interest income. The remaining interest income of Ps.7,025 million is broken down as follows: 22.8% from investment in securities, 3.4% from repurchase agreements, 1.5% from funds available, and 0.3% from margin accounts.

Interest income for 2Q21 decreased 14.6%, or Ps.4,285 million YoY, to Ps.25,098 million, reflecting lower interest income from total loan portfolio, investment in securities, repurchase agreements, funds available and margin accounts, which decreased 15.2%, or Ps.3,202 million, 7.8%, or Ps.482 million, 28.3%, or Ps.339 million, 39.4%, or Ps.240 million, and 38.5%, or Ps.40 million, respectively.

The average interest yield on interest-earning assets in 2Q21 stood at 7.11%, decreasing 105 basis points from 8.16% in 2Q20. Sequentially, the average interest yield on interest-earning assets remained flat, from 7.12% in 1Q21.

In 2Q21, the average interest rate on the total loan portfolio stood at 10.04%, a decrease of 85 basis points YoY, reflecting lower interest rates and change in the loan portfolio mix. Relative to 2Q20, the average reference rate (TIIE28) decreased 177 basis points. The average interest rate on the consumer loan portfolio stood at 22.80%, a decrease of 284 basis points YoY, while the yield of credit card loan portfolio stood at 23.68%, a decrease of 166 basis points YoY, the rate on the commercial loan portfolio stood at 6.71%, a decrease of 139 basis points YoY and the yield of the mortgage loan portfolio stood at 9.37%, an increase of 8 basis points YoY. The average interest rate on the investment in securities portfolio stood at 4.91%, decreasing 105 basis points YoY.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 15 |

| |

| |

| Interest income | |||||||||||

| Million Pesos | 2Q21 | 2Q20 | Var YoY | ||||||||

| Average Balance | Interest | Yield (%) | Average Balance | Interest | Yield (%) | Average Balance | Interest (%) | Yield (bps) | |||

| Funds available | 122,067 | 369 | 1.20 | 116,060 | 609 | 2.08 | 5.2 | (39.4) | (88) | ||

| Margin accounts | 19,114 | 64 | 1.32 | 46,447 | 104 | 0.89 | (58.8) | (38.5) | 43 | ||

| Investment in securities | 462,289 | 5,735 | 4.91 | 412,331 | 6,217 | 5.96 | 12.1 | (7.8) | (105) | ||

| Loan portfolio | 706,727 | 17,928 | 10.04 | 767,654 | 21,130 | 10.89 | (7.9) | (15.2) | (85) | ||

| Commissions collected on loan originations | — | 145 | — | — | 127 | — | — | 14.2 | — | ||

| Sale and repurchase agreements and securities loans | 85,587 | 857 | 3.96 | 81,179 | 1,196 | 5.83 | 5.4 | (28.3) | (187) | ||

| Interest income | 1,395,784 | 25,098 | 7.11 | 1,423,671 | 29,383 | 8.16 | (2.0) | (14.6) | (105) | ||

Interest income decline from the total loan portfolio was 15.2%, or Ps.3,202 million, which resulted from the combined effect of a 85 basis points decrease in the average interest rate, and a 7.9%, or Ps.60,927 million, decrease in average loan portfolio volume. The decrease in interest income from the loan portfolio resulted from the following YoY combined effects by product:

| § | Commercial: 17.0%, or Ps.84,984 million decrease, with a 6.71% interest yield, which decreased 139 bps; |

| § | Credit Cards: 6.7%, or Ps.3,690 million decrease, with a 23.68% interest yield, which decreased 166 bps; |

| § | Consumer: 9.1%, or Ps.5,234 million increase, with a 22.80% interest yield, which decreased 284 bps; and |

| § | Mortgages: 14.5%, or Ps.22,513 million increase, with a 9.37% interest yield, which increased 8 bps. |

Interest income from investment in securities decreased 7.8%, or Ps.482 million, which resulted from the combined effect of an increase of 12.1%, or Ps.49,958 million, in average volume, and a 105 basis points decrease in the average interest rate. Interest income from repurchase agreements decreased 28.3%, or Ps.339 million, which resulted from the increase of 5.4%, or Ps.4,408 million, in average volume, and a 187 basis points decrease in the average interest rate.

Interest expense

Total average interest-bearing liabilities amounted to Ps.1,250,767 million, decreasing 1.5% YoY, or Ps.18,813 million, and were driven by decreases of 25.7%, or Ps.82,840 million, in time deposits, 48.7%, or Ps.39,046 million, in bank and other loans, 7.7%, or Ps.6,385 million, in credit instruments issued, and 14.2%, or Ps.4,305 million, in subordinated capital notes. These decreases were partly offset by increases of 30.5%, or Ps.83,514 million, in repurchase agreements, and 6.3%, or Ps.30,249 million, in demand deposits.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 16 |

| |

| |

Banco Santander México’s interest-bearing liabilities are broken down as follows:

| Average liabilities (interest-bearing liabilities) | |||||

| Breakdown (%) | |||||

| 2Q20 | 3Q20 | 4Q20 | 1Q21 | 2Q21 | |

| Demand deposits | 37.7 | 37.9 | 37.1 | 37.9 | 40.7 |

| Sale and repurchase agreements and securities loans | 21.6 | 24.8 | 28.6 | 29.7 | 28.5 |

| Time deposits | 25.4 | 24.4 | 21.9 | 20.5 | 19.2 |

| Credit instruments issued | 6.6 | 6.9 | 6.3 | 6.4 | 6.2 |

| Bank and other loans | 6.3 | 3.8 | 4.0 | 3.4 | 3.3 |

| Subordinated capital notes | 2.4 | 2.2 | 2.1 | 2.1 | 2.1 |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Banco Santander México’s interest expense consists mainly of interest paid on customer deposits and repurchase agreements, which in 2Q21 amounted to Ps.3,934 million and Ps.3,322 million, respectively, accounting for 42.2% and 35.6% of interest expenses. The remaining Ps.2,072 million was paid as follows: 12.6% on credit instruments issued, 5.2% on bank and other loans, and 4.4% on subordinated debentures.

Interest expense for 2Q21 decreased 30.7% YoY, or Ps.4,124 million, to Ps.9,328 million, mainly driven by lower interest expenses on time deposits, demand deposits, repurchase agreements and bank and other loans.

The average interest rate on interest-bearing liabilities decreased 124 basis points to 2.95% in 2Q21. For 2Q21, the average interest rate on the main sources of funding decreased YoY as follows:

| § | 199 basis points in time deposits, at an average interest rate paid of 3.40%; |

| § | 179 basis points in repurchase agreements, at an average interest rate paid of 3.68%; and |

| § | 68 basis points in demand deposits, at an average interest rate paid of 1.45%. |

| Interest expense | |||||||||||

| Million pesos | 2Q21 | 2Q20 | Var YoY | ||||||||

| Average Balance | Interest | Yield (%) | Average Balance | Interest | Yield (%) | Average Balance | Interest (%) | Yield (bps) | |||

| Demand deposits | 509,339 | 1,869 | 1.45 | 479,090 | 2,583 | 2.13 | 6.3 | (27.6) | (68) | ||

| Time deposits | 240,044 | 2,065 | 3.40 | 322,884 | 4,402 | 5.39 | (25.7) | (53.1) | (199) | ||

| Credit instruments issued | 77,064 | 1,177 | 6.04 | 83,449 | 1,256 | 5.95 | (7.7) | (6.3) | 9 | ||

| Bank and other loans | 41,054 | 484 | 4.66 | 80,100 | 946 | 4.67 | (48.7) | (48.8) | (1) | ||

| Subordinated capital notes | 26,032 | 411 | 6.25 | 30,337 | 478 | 6.23 | (14.2) | (14.0) | 2 | ||

| Sale and repurchase agreements and securities loans | 357,234 | 3,322 | 3.68 | 273,720 | 3,787 | 5.47 | 30.5 | (12.3) | (179) | ||

| Interest expense | 1,250,767 | 9,328 | 2.95 | 1,269,580 | 13,452 | 4.19 | (1.5) | (30.7) | (124) | ||

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 17 |

| |

| |

Increases in retail deposits continue to reflect the Bank’s focus on driving profitability with a higher reliance on retail deposits. The average balance of demand deposits increased 6.3% YoY, or Ps.30,249 million, while the average balance of time deposits contracted 25.7% YoY, or Ps.82,840 million. Interest paid on demand deposits decreased 27.6% YoY, or Ps.714 million and interest paid on time deposits decreased 53.1% YoY, or Ps.2,337.

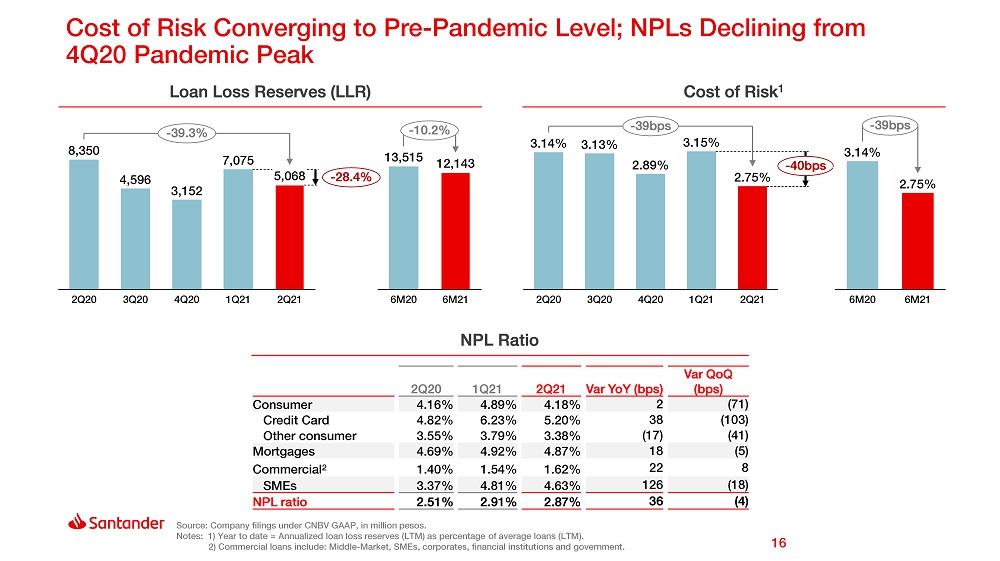

Provisions for loan losses and asset quality

During 2Q21, provisions for loan losses amounted to Ps.5,068 million, which represented a decrease of 39.3%, or Ps.3,282 million, YoY, and a 28.4%, or Ps.2,007 million, on a sequential basis, reflecting easier comps due to provisions for loan losses made in 1Q21, as some customers in the entertainment and retail sectors were affected by the COVID-19 pandemic, although remaining current, and to the additional provisions made in the 2Q20 to face the COVID-19 pandemic.

| Loan Loss Reserves | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | YoY | ||||

| Commercial | 1,823 | 3,414 | 3,149 | (46.6) | (42.1) | 5,237 | 3,933 | 33.2 | |||

| Consumer | 2,826 | 3,120 | 3,902 | (9.4) | (27.6) | 5,946 | 7,073 | (15.9) | |||

| Mortgages | 419 | 541 | 1,299 | (22.6) | (67.7) | 960 | 2,509 | (61.7) | |||

| Total | 5,068 | 7,075 | 8,350 | (28.4) | (39.3) | 12,143 | 13,515 | (10.1) | |||

| Cost of Risk (%) | |||||||||||

| Variation (bps) | Variation (bps) | ||||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | YoY | ||||

| Commercial | 1.63 | 1.85 | 1.49 | (22) | 14 | 1.63 | 1.49 | 14 | |||

| Consumer | 10.65 | 11.58 | 11.32 | (93) | (67) | 10.65 | 11.32 | (67) | |||

| Mortgages | 0.36 | 0.90 | 1.93 | (54) | (157) | 0.36 | 1.93 | (157) | |||

| Total | 2.75 | 3.15 | 3.14 | (40) | (39) | 2.75 | 3.14 | (39) | |||

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 18 |

| |

| |

Non-performing loans as of June 2021 increased 8.3% YoY, or Ps.1,557 million, to Ps.20,401 million, and decreased Ps.359 million, or 1.7% on a sequential basis. The YoY increase in non-performing loans was due to increases of 19.5%, or Ps.1,449 million, in mortgage loans and 2.9%, or Ps.135 million, in consumer loans (including credit cards). These increases were partially offset by a decrease of 0.4%, or Ps.27 million, in commercial loans.

NPL ratio for the SMEs loan portfolio increased 126 basis points YoY and decreased 18 basis points sequentially, further affected by the economic environment. Commercial loans NPL ratio increased 22 basis points YoY and 8 basis points QoQ. At the same time, mortgage loans NPL ratio increased 18 basis points YoY and decreased 5 basis points QoQ. While consumer loan portfolio (including credit cards) NPL ratio increased 2 basis point YoY and decreased 71 basis points sequentially.

The breakdown of the non-performing loan portfolio is as follows: mortgage loans 43.6%, commercial loans 32.7% and consumer loans (including credit cards) 23.7%.

| Non-Performing loan ratio (%) | ||||||

| Variation (bps) | ||||||

| Jun-21 | Mar-21 | Jun-20 | QoQ | YoY | ||

| Commercial | 1.62 | 1.54 | 1.40 | 8 | 22 | |

| SMEs | 4.63 | 4.81 | 3.37 | (18) | 126 | |

| Others | 1.15 | 1.00 | 1.06 | 15 | 9 | |

| Individuals | ||||||

| Consumer | 4.18 | 4.89 | 4.16 | (71) | 2 | |

| Credit Card | 5.20 | 6.23 | 4.82 | (103) | 38 | |

| Other consumer | 3.38 | 3.79 | 3.55 | (41) | (17) | |

| Mortgages | 4.87 | 4.92 | 4.69 | (5) | 18 | |

| Total | 2.87 | 2.91 | 2.51 | (4) | 36 | |

The aforementioned variations in non-performing loans led to an NPL ratio of 2.87% in June 2021, increasing 36 basis points from 2.51% in June 2020, still reflecting the impact of the COVID-19 pandemic, and decreasing 4 basis points compared to the 2.91% reported in March 2021.

Finally, the coverage ratio for June 2021 stood at 118.39%, decreasing from 138.81% in June 2020 and from the 120.12% in March 2021.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 19 |

| |

| |

Commission and fee income, net

| Commission and fee income, net | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 2Q21 | 1Q21 | 1Q20 | QoQ | YoY | 6M21 | 6M20 | 21/20 | ||||

| Commission and fee income | |||||||||||

| Debit and credit card | 2,291 | 2,235 | 1,983 | 2.5 | 15.5 | 4,526 | 4,259 | 6.3 | |||

| Account management | 658 | 650 | 641 | 1.2 | 2.7 | 1,308 | 1,289 | 1.5 | |||

| Collection services | 551 | 592 | 508 | (6.9) | 8.5 | 1,143 | 1,104 | 3.5 | |||

| Investment funds | 429 | 414 | 396 | 3.6 | 8.3 | 843 | 790 | 6.7 | |||

| Insurance | 1,471 | 1,285 | 1,369 | 14.5 | 7.5 | 2,756 | 2,600 | 6.0 | |||

| Purchase-sale of securities and money market transactions | 239 | 238 | 246 | 0.4 | (2.8) | 477 | 495 | (3.6) | |||

| Checks trading | 43 | 42 | 36 | 2.4 | 19.4 | 85 | 89 | (4.5) | |||

| Foreign trade | 408 | 394 | 388 | 3.6 | 5.2 | 802 | 787 | 1.9 | |||

| Financial advisory services | 343 | 435 | 435 | (21.1) | (21.1) | 778 | 871 | (10.7) | |||

| Other | 229 | 250 | 186 | (8.4) | 23.1 | 479 | 412 | 16.3 | |||

| Total | 6,662 | 6,535 | 6,188 | 1.9 | 7.7 | 13,197 | 12,696 | 3.9 | |||

| Commission and fee expense | |||||||||||

| Debit and credit card | (959) | (785) | (820) | 22.2 | 17.0 | (1,744) | (1,815) | (3.9) | |||

| Investment funds | (1) | 0 | 0 | 100.0 | 100.0 | (1) | 0 | 100.0 | |||

| Insurance | (34) | (37) | (29) | (8.1) | 17.2 | (71) | (61) | 16.4 | |||

| Purchase-sale of securities and money market transactions | (41) | (42) | (56) | (2.4) | (26.8) | (83) | (95) | (12.6) | |||

| Checks trading | (12) | (11) | (10) | 9.1 | 20.0 | (23) | (21) | 9.5 | |||

| Financial advisory services | 0 | (7) | (9) | (100.0) | (100.0) | (7) | (10) | (30.0) | |||

| Bank Correspondents | (219) | (216) | (173) | 1.4 | 26.6 | (435) | (381) | 14.2 | |||

| Other | (523) | (535) | (493) | (2.2) | 6.1 | (1,058) | (1,018) | 3.9 | |||

| Total | (1,789) | (1,633) | (1,590) | 9.6 | 12.5 | (3,422) | (3,401) | 0.6 | |||

| Commission and fee income, net | |||||||||||

| Debit and credit card | 1,332 | 1,450 | 1,163 | (8.1) | 14.5 | 2,782 | 2,444 | 13.8 | |||

| Account management | 658 | 650 | 641 | 1.2 | 2.7 | 1,308 | 1,289 | 1.5 | |||

| Collection services | 551 | 592 | 508 | (6.9) | 8.5 | 1,143 | 1,104 | 3.5 | |||

| Investment funds | 428 | 414 | 396 | 3.4 | 8.1 | 842 | 790 | 6.6 | |||

| Insurance | 1,437 | 1,248 | 1,340 | 15.1 | 7.2 | 2,685 | 2,539 | 5.8 | |||

| Purchase-sale of securities and money market transactions | 198 | 196 | 190 | 1.0 | 4.2 | 394 | 400 | (1.5) | |||

| Checks trading | 31 | 31 | 26 | 0.0 | 19.2 | 62 | 68 | (8.8) | |||

| Foreign trade | 408 | 394 | 388 | 3.6 | 5.2 | 802 | 787 | 1.9 | |||

| Financial advisory services | 343 | 428 | 426 | (19.9) | (19.5) | 771 | 861 | (10.5) | |||

| Bank Correspondents | (219) | (216) | (173) | 1.4 | 26.6 | (435) | (381) | 14.2 | |||

| Other | (294) | (285) | (307) | 3.2 | (4.2) | (579) | (606) | (4.5) | |||

| Total | 4,873 | 4,902 | 4,598 | (0.6) | 6.0 | 9,775 | 9,295 | 5.2 | |||

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 20 |

| |

| |

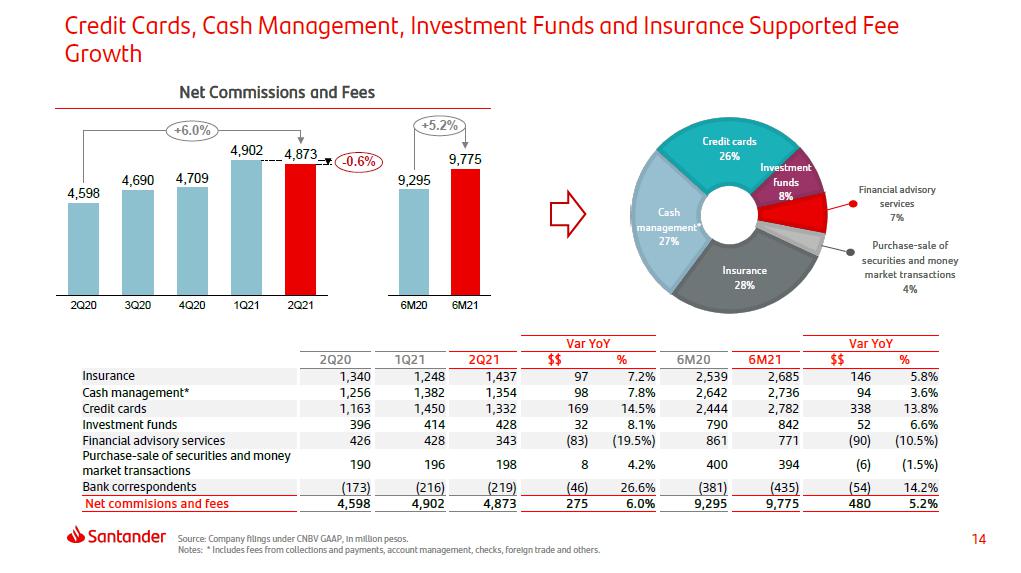

In 2Q21, net commission and fee income totaled Ps.4,873 million, increasing 6.0% YoY, or Ps.275 million, and decreased 0.6% QoQ, or Ps.29 million. Commission and fee income increased 7.7% YoY, or Ps.474 million, to Ps.6,662 million in 2Q21, while commission and fee expense increased 12.5% YoY, or Ps.199 million, to Ps.1,789 million in 2Q21.

The main contributors to net commissions and fees were insurance fees, which accounted for 29.5% of the total, followed by credit and debit card fees, account management and collection services fees, which accounted for 27.3%, 13.5% and 11.3% of total commissions and fees, respectively.

| Net commissions and fees | ||||||

| Breakdown (%) | ||||||

| 2Q21 | 1Q21 | 2Q20 | 6M21 | 6M20 | ||

| Insurance | 29.5 | 25.5 | 29.1 | 27.5 | 27.3 | |

| Credit cards | 27.3 | 29.6 | 25.3 | 28.5 | 26.3 | |

| Account management | 13.5 | 13.3 | 13.9 | 13.4 | 13.9 | |

| Collection services | 11.3 | 12.1 | 11.1 | 11.7 | 11.9 | |

| Investment funds | 8.8 | 8.4 | 8.6 | 8.6 | 8.5 | |

| Foreign trade | 8.4 | 8.0 | 8.5 | 8.2 | 8.5 | |

| Financial advisory services | 7.0 | 8.7 | 9.3 | 7.9 | 9.3 | |

| Purchase-sale of securities and money market transactions | 4.1 | 4.0 | 4.1 | 4.0 | 4.3 | |

| Checks trading | 0.6 | 0.6 | 0.6 | 0.6 | 0.7 | |

| Bank correspondents | (4.5) | (4.4) | (3.8) | (4.5) | (4.1) | |

| Other | (6.0) | (5.8) | (6.7) | (5.9) | (6.6) | |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 |

Net commissions and fees were up 6.0% YoY, or Ps.275 million in 2Q21, mostly as a result of the following increases:

| i) | A 14.5%, or Ps.169 million, in debit and credit card fees, as the economy reopens and was reflected in credit card transactions; |

| ii) | A 7.2%, or Ps.97 million, in insurance, driven by strong origination in mortgage and auto loans; and |

| iii) | An 8.5%, or Ps.43 million, in collection and payments, and a 2.7%, or Ps.17 million, in account management. |

These positive contributions to net commissions and fees were partly offset by:

| i) | A 19.5%, or Ps.83 million, decrease in financial advisory services, due to lower transactions. |

On a cumulative basis, net commissions and fees amounted Ps.9,775 million in 6M21, reflecting a YoY increase of 5.2%, or Ps.480 million. Commission and fee income increased 3.9%, or Ps.501 million, while commission and fee expense increased 0.6%, or Ps.21 million.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 21 |

| |

| |

Net gain (loss) on financial assets and liabilities

| Net gain (loss) on financial assets and liabilities | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | 21/20 | ||||

| Valuation | |||||||||||

| Foreign exchange | 668 | (1,218) | (143) | — | — | (550) | 2,599 | (121.2) | |||

| Derivatives | 1,055 | 2,999 | (4,656) | (64.8) | 122.7 | 4,054 | (1,812) | — | |||

| Equity securities | (49) | (73) | 942 | (32.9) | (105.2) | (122) | 21 | — | |||

| Debt instruments | (1,373) | (4,895) | 6,307 | (72.0) | (121.8) | (6,268) | 6,862 | — | |||

| Valuation result | 301 | (3,187) | 2,450 | 109.4 | (87.7) | (2,886) | 7,670 | (137.6) | |||

| Purchase / sale of securities | |||||||||||

| Foreign exchange | 330 | 2,301 | 1,109 | (85.7) | (70.2) | 2,631 | (3,023) | — | |||

| Derivatives | (17) | 1,180 | (53) | (101.4) | 67.9 | 1,163 | (902) | — | |||

| Equity securities | 40 | 166 | (240) | (75.9) | 116.7 | 206 | (315) | — | |||

| Debt instruments | 163 | 938 | 17 | (82.6) | — | 1,101 | 736 | 49.6 | |||

| Purchase -sale result | 516 | 4,585 | 833 | (88.7) | (38.1) | 5,101 | (3,504) | — | |||

| Total | 817 | 1,398 | 3,283 | (41.6) | (75.1) | 2,215 | 4,166 | (46.8) | |||

In 2Q21, Banco Santander México reported a Ps.817 million net gain from financial assets and liabilities, which compares with a gain of Ps.3,283 million in 2Q20 and a gain of Ps.1,398 million in 1Q21. The YoY decrease in net gain from financial assets and liabilities, resulted from a higher base in 2Q20, due to extraordinary gains related to the sale of certain securities to strengthen the Bank liquidity position.

The Ps.817 million net gain from financial assets and liabilities in the quarter is mostly a result of:

| i) | A Ps.516 million purchase-sale gain, related to gains of Ps.330 million, Ps.163 million and Ps.40 million, in foreign exchange, debt instruments and equity securities, respectively. These gains were partly offset by a loss of Ps.17 million in derivatives; and |

| ii) | A Ps.301 million valuation gain, which resulted from gains of Ps.1,055 million and Ps.668 million in derivatives and foreign exchange, respectively. These gains were partly offset by losses of Ps.1,373 million and Ps.49 million, in debt instruments and equity securities. |

On a cumulative basis, net gain from financial assets and liabilities for the first half of the year, reached Ps.2,215 million, representing a decrease of 46.8% YoY, or Ps.1,951 million.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 22 |

| |

| |

Other operating expense

| Other operating expense | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | 21/20 | ||||

| Cancellation of liabilities and reserves | (20) | 90 | 105 | (122.2) | (119.0) | 70 | 201 | (65.2) | |||

| Interest on personnel loans | 47 | 47 | 67 | 0.0 | (29.9) | 94 | 140 | (32.9) | |||

| Allowance for losses on foreclosed assets | (9) | (7) | (8) | 28.6 | 12.5 | (16) | (13) | 23.1 | |||

| Profit from sale of foreclosed assets | 18 | 103 | 21 | (82.5) | (14.3) | 121 | 296 | (59.1) | |||

| Technical advisory and technology services | 21 | 17 | 39 | 23.5 | (46.2) | 38 | 60 | (36.7) | |||

| Portfolio recovery legal expenses and costs | (239) | (352) | (206) | (32.1) | 16.0 | (591) | (328) | 80.2 | |||

| Premiums paid on guarantees for SMEs loans portfolio | (274) | (321) | (235) | (14.6) | 16.6 | (595) | (533) | 11.6 | |||

| Write-offs and bankruptcies | (175) | (251) | (124) | (30.3) | 41.1 | (426) | (360) | 18.3 | |||

| Provision for legal and tax contingencies | (53) | (54) | (77) | (1.9) | (31.2) | (107) | (168) | (36.3) | |||

| Others | 142 | 64 | 186 | 121.9 | (23.7) | 206 | 261 | (21.1) | |||

| Total | (542) | (664) | (232) | (18.4) | 133.6 | (1,206) | (444) | — | |||

Other operating expenses in 2Q21 totaled Ps.542 million, higher from Ps.232 million in 2Q20 and down from Ps.664 million reported in 1Q21.

The Ps.310 million, YoY increase, in other operating expenses in 2Q21 was mainly driven by a decrease in cancellation of liabilities and reserves of 119.0%, or Ps.125 million, higher write-offs of 41.1%, or Ps.51 million, a decrease in other operating income of 23.7%, or Ps.44 million, higher premiums paid on guarantees for the SMEs loan portfolio of 16.6%, or Ps.39 million and higher legal expenses and costs related to portfolio recoveries of 16.0%, or Ps.33 million.

On a cumulative basis, other operating expenses for 6M21, reached Ps.1,206 million, representing a Ps.762 million YoY increase.

Administrative and promotional expenses

Administrative and promotional expenses consist of personnel costs, such as payroll and benefits, promotion and advertising expenses, and other general expenses. Personnel expenses consist mainly of salaries, social security contributions, bonuses and a long-term incentive plan for the Bank’s executives. Other general expenses are mainly related to technology and systems, administrative services - mainly outsourced in the areas of information technology - taxes and duties, professional fees, contributions to IPAB, rental of properties and hardware, advertising and communication, surveillance and cash courier services, and expenses related to maintenance, conservation and repair, among others.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 23 |

| |

| |

| Administrative and promotional expenses | |||||||||||

| Million pesos | % Variation | % Variation | |||||||||

| 2Q21 | 1Q21 | 2Q20 | QoQ | YoY | 6M21 | 6M20 | 21/20 | ||||

| Salaries and employee benefits | 4,056 | 3,938 | 3,555 | 3.0 | 14.1 | 7,994 | 7,477 | 6.9 | |||

| Credit card operation | 47 | 52 | 57 | (9.6) | (17.5) | 99 | 106 | (6.6) | |||

| Professional fees | 218 | 185 | 245 | 17.8 | (11.0) | 403 | 407 | (1.0) | |||

| Leasehold | 616 | 620 | 659 | (0.6) | (6.5) | 1,236 | 1,309 | (5.6) | |||

| Promotional and advertising expenses | 165 | 147 | 205 | 12.2 | (19.5) | 312 | 420 | (25.7) | |||

| Taxes and duties | 542 | 588 | 494 | (7.8) | 9.7 | 1,130 | 1,193 | (5.3) | |||

| Technology services (IT) | 1,221 | 1,297 | 1,181 | (5.9) | 3.4 | 2,518 | 2,206 | 14.1 | |||

| Depreciation and amortization | 1,161 | 1,182 | 993 | (1.8) | 16.9 | 2,343 | 2,008 | 16.7 | |||

| Contributions to IPAB | 943 | 938 | 1,049 | 0.5 | (10.1) | 1,881 | 1,883 | (0.1) | |||

| Cash protection | 302 | 289 | 227 | 4.5 | 33.0 | 591 | 587 | 0.7 | |||

| Others | 684 | 658 | 934 | 4.0 | (26.8) | 1,342 | 1,788 | (24.9) | |||

| Total | 9,955 | 9,894 | 9,599 | 0.6 | 3.7 | 19,849 | 19,384 | 2.4 | |||

Banco Santander México’s administrative and promotional expenses are broken down as follows:

| Administrative and promotional expenses | ||||||

| Breakdown (%) | ||||||

| 2Q21 | 1Q21 | 2Q20 | 6M21 | 6M20 | ||

| Personnel | 40.7 | 39.8 | 37.0 | 40.3 | 38.6 | |

| Technology services (IT) | 12.3 | 13.1 | 12.3 | 12.7 | 11.4 | |

| Depreciation and amortization | 11.7 | 11.9 | 10.3 | 11.8 | 10.4 | |

| IPAB | 9.5 | 9.5 | 10.9 | 9.5 | 9.7 | |

| Others | 6.9 | 6.7 | 9.7 | 6.8 | 9.2 | |

| Leasehold | 6.2 | 6.3 | 6.9 | 6.2 | 6.8 | |

| Taxes and duties | 5.4 | 5.9 | 5.2 | 5.7 | 6.2 | |

| Cash protection | 3.0 | 2.9 | 2.4 | 3.0 | 3.0 | |

| Professional fees | 2.2 | 1.9 | 2.6 | 2.0 | 2.1 | |

| Promotional and advertising expenses | 1.6 | 1.5 | 2.1 | 1.6 | 2.2 | |

| Credit card operation | 0.5 | 0.5 | 0.6 | 0.4 | 0.4 | |

| Total | 100.0 | 100.0 | 100.0 | 100.0 | 100.0 | |

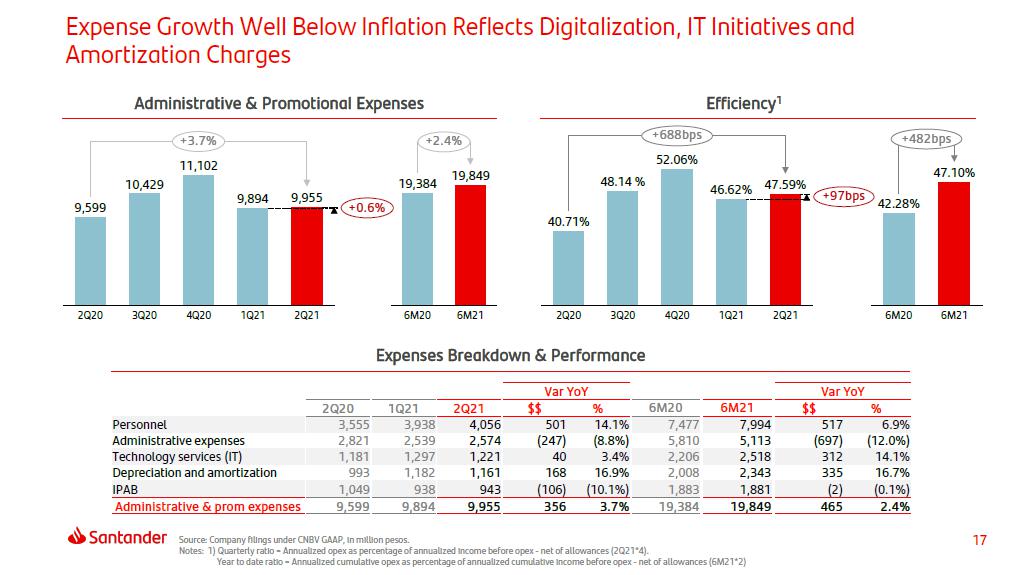

Administrative and promotional expenses in 2Q21 totaled Ps.9,955 million, compared to Ps.9,599 million in 2Q20 and Ps.9,894 million in 1Q21, increasing 3.7% YoY, or Ps.356 million and 0.6% QoQ, or Ps.61 million.

The 3.7% YoY, or Ps.356 million, increase in administrative and promotional expenses was mainly due to the following increases:

| i) | 14.1%, or Ps.501 million, in salaries and employee benefits, mainly due to the reinforcement of certain critical business units such as auto, IT and cybersecurity; |

| ii) | 16.9%, or Ps.168 million, in depreciations and amortizations, mainly related to the Bank’s strategic initiatives; and |

| iii) | 33.0%, or Ps.75 million, in cash protection. |

These increases were partly offset by the following decreases:

| i) | 26.8%, or Ps.250 million, in other expenses; and |

| ii) | 10.1%, or Ps.106 million, in contributions to IPAB. |

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 24 |

| |

| |

The efficiency ratio for the quarter increased 688 basis points YoY and 97 basis points QoQ to 47.59%.

The recurrence ratio for 2Q21 was 48.95%, up from 47.90% in 2Q20 and 49.55% reported in 1Q21.

On a cumulative basis, administrative and promotional expenses in 6M21 amounted Ps.19,849 million, reflecting an increase of 2.4%, or Ps.465 million. The efficiency ratio for the first half of the year increased 482 basis points YoY from 42.28% in 6M20 to 47.10% in 6M21.

Profit before taxes

Profit before taxes in 2Q21 was Ps.5,945 million, reflecting increases of 4.9%, or Ps.279 million, YoY, and 37.3%, or Ps.1,616 million, QoQ.

On a cumulative basis, profit before taxes for 6M21 amounted Ps.10,274 million, reflecting a YoY decrease of 20.9%, or Ps.2,710 million.

Income taxes

In 2Q21, Banco Santander México reported a tax expense of Ps.1,232 million compared to Ps.1,436 million in 2Q20 and Ps.1,050 million in 1Q21. The effective tax rate for the quarter was 20.72%, compared to 25.34% reported in 2Q20 and 24.26% in 1Q21.

On a cumulative basis, the effective tax rate for 6M21 stood at 22.21%, 351 basis points lower than the 25.72% for 6M20.

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 25 |

| |

| |

Capitalization and liquidity

| Capitalization | ||||||

| Million pesos | Jun-21 | Mar-21 | Jun-20 | |||

| CET1 | 113,511 | 114,711 | 96,915 | |||

| Tier 1 | 123,462 | 124,926 | 108,451 | |||

| Tier 2 | 27,128 | 27,855 | 30,507 | |||

| Total capital | 150,590 | 152,782 | 138,958 | |||

| Risk-weighted assets | ||||||

| Credit risk | 536,820 | 526,922 | 545,833 | |||

| Credit, market and operational risk | 796,432 | 774,368 | 832,610 | |||

| Credit risk ratios: | ||||||

| CET1 (%) | 21.15 | 21.77 | 17.76 | |||

| Tier 1 (%) | 23.00 | 23.71 | 19.87 | |||

| Tier 2 (%) | 5.05 | 5.29 | 5.59 | |||

| Capitalization ratio (%) | 28.05 | 29.00 | 25.46 | |||

| Total capital ratios: | ||||||

| CET1 (%) | 14.25 | 14.81 | 11.64 | |||

| Tier 1 (%) | 15.50 | 16.13 | 13.03 | |||

| Tier 2 (%) | 3.41 | 3.60 | 3.65 | |||

| Capitalization ratio (%) | 18.91 | 19.73 | 16.69 |

Banco Santander México’s capital ratio at June 2021 was 18.91%, compared to 16.69% and 19.73% at June 2020 and March 2021, respectively. The 18.91% capital ratio was comprised of 14.25% of fundamental capital (CET1), 1.25% of additional capital (AT1), and 3.41% of complementary capital (Tier 2).

As of May 2021, Banco Santander México was classified in Category 1, in accordance with Article 134 Bis of the Mexican Banking Law, and the Bank remains in this category per the preliminary results dated June 30th, 2021, which is the most recent available analysis.

Liquidity coverage ratio (LCR)

Pursuant to the regulatory requirements of Banxico and the Mexican National Banking and Securities Commission (Comisión Nacional Bancaria y de Valores, or “CNBV”), the average Liquidity Coverage Ratio (LCR or CCL by its Spanish acronym) for 2Q21 was 315.99%, which compares to 211.33% in 2Q20 and 316.00% in 1Q21. (Please refer to note 24 of this report).

Leverage ratio

In accordance with CNBV regulatory requirements, effective June 14, 2016, the leverage ratio was 7.95% for June 2021, 7.61% for March 2021, 7.39% for December 2020, 6.82% for September 2020 and 6.53% for June 2020.

This ratio is defined by regulators and is calculated by dividing core capital (according to Article 2 Bis 6 (CUB)) by adjusted assets (according to Article 1, II (CUB)).

V.Relevant Events, Transactions and Activities

Relevant Events

Organizational changes within its corporate and investment banking segment

On June 14, 2021 Banco Santander México announced that Felipe García Ascencio was appointed as Deputy General Director of Corporate and Investment Banking, reporting to Héctor Grisi Checa, subject to corresponding regulatory authorizations.

General Ordinary and Extraordinary Shareholders’ Meetings

On June 09, 2021 Banco Santander México held its General Ordinary and Extraordinary Shareholders’ Meeting, at which, among others, the following resolutions were adopted:

Earnings Release | 2Q.2021 | |

Banco Santander México | |

| 26 |

| |

| |

| § | The payment of a cash dividend in the amount of Ps.3,054 million paid on June 18, 2021; such payment was made, at a rate of Ps.0.45, in proportion to the number of shares that each shareholder held as of the record date. |

| § | Due to change in the intended conditions of the Tender Offer to become a voluntary tender offer and eliminating as a requirement the delisting, the discussion on the delisting was unnecessary and no resolution was adopted in this regard. Therefore, the shares of Banco Santander México will continue listed on the BMV and NYSE. |

Banco Santander México informed that its Parent Company, issued a material fact announcement

On June 8, 2021, Banco Santander México announced that Banco Santander, S.A., its Parent Company, had issued a material fact, announcing its intention to launch a voluntary Tender Offer, instead of a mandatory delisting tender offer as previously announced. This announcement complemented the ones issued on March 26 and May 24, 2021, related to the intention to make a Tender Offer.

Banco Santander México was designated a Level III Domestic Systemically Important Financial Institution by the Mexican National Banking and Securities Commission for the sixth consecutive year

On May 27, 2021, Banco Santander México was designated a Level III Domestic Systemically Important Financial Institution by the Mexican National Banking and Securities Commission (CNBV), for the sixth consecutive year. The Bank already complies with this regulatory requirement.

Banco Santander México informed that its Parent Company, issued a material fact announcement

On May 24, 2021, Banco Santander México announced that Banco Santander, S.A., its Parent Company, had issued a material fact to announce that it has determined to, if the tender offer is launched, maintain the price of Ps.24 per share and the U.S. Dollar equivalent of Ps.120.00 per ADS, despite the payment of a dividend amounting to Ps.0.45 per share (Ps.2.25 per American Depositary Share). This announcement complemented the one issued on March 26, 2021, related to the intention to make a Tender Offer.

Call to the General Ordinary and Extraordinary Shareholders’ Meetings

On May 10, 2021 Banco Santander México called to its Annual General Ordinary and Extraordinary Shareholders’ Meetings that was held on June 9, 2021 at which, among other items, it would be discussed for approval the payment of a cash dividend and the delisting.

Annual General Ordinary and Special Shareholders’ Meetings

On April 29, 2021, Banco Santander México held its Annual General Ordinary and Special Shareholders’ Meetings, and approved among other items:

| § | The integration of the Board of Directors as indicated below: |

| Series “F” Independent Directors | |

| Laura Renné Diez Barroso Azcárraga | Chairwoman |

| Cesar Augusto Montemayor Zambrano | Director |

| Juan Ignacio Gallardo Thurlow | Alternate Director |

| Guillermo Jorge Quiroz Abed | Alternate Director |

| Alberto Torrado Martínez | Alternate Director |

| Bárbara Garza Lagüera Gonda | Alternate Director |

| José Eduardo Carredano Fernández | Alternate Director |

| Series “F” Non-Independent Directors | |

| Héctor Blas Grisi Checa | Director |

| Magdalena Sofía Salarich Fernández de Valderrama | Director |

| Francisco Javier García-Carranza Benjumea | Director |

| Ángel Rivera Congosto | Director |

| Didier Mena Campos | Director |

| Rodrigo Brand de Lara | Alternate Director |