|

|

Subject to Completion. Dated July 5, 2022. GS Finance Corp. $ Autocallable Goldman Sachs Momentum Builder® Focus ER Index-Linked Notes due guaranteed by The Goldman Sachs Group, Inc. |

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-253421

The information in this preliminary pricing supplement is not complete and may be changed. This preliminary pricing supplement is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

|

|

Subject to Completion. Dated July 5, 2022. GS Finance Corp. $ Autocallable Goldman Sachs Momentum Builder® Focus ER Index-Linked Notes due guaranteed by The Goldman Sachs Group, Inc. |

The notes do not bear interest. Unless your notes are automatically called on any annual call observation date, the amount that you will be paid on your notes on the stated maturity date (expected to be August 3, 2027) will be based on the performance of the Goldman Sachs Momentum Builder® Focus ER Index (the “index”) as measured from the trade date (expected to be July 29, 2022) to and including the determination date (expected to be July 29, 2027).

If the final index level (the closing level of the index on the determination date) is greater than or equal to the initial index level (set on the trade date and may be higher or lower than the actual closing level of the index on that date), the return on your notes will be positive and you will receive the maximum settlement amount of $1,500 for each $1,000 face amount of your notes.

Your notes will be called if the closing level of the index on any call observation date is greater than or equal to the initial index level, resulting in a payment on the corresponding call payment date (the third business day after the call observation date) equal to the face amount of your notes plus the product of $1,000 times the applicable call return (specified on page PS-7).

The index measures the performance of a “base index” and non-interest bearing cash positions subject to certain deductions, as described in further detail below. On each index business day, exposure to the base index will be reduced and exposure to the non-interest bearing cash positions increased if (i) the realized volatility of the base index exceeds a volatility control limit of 5% (we refer to the base index, after applying this volatility control limit, as the “volatility controlled index”) or (ii) the volatility controlled index has exhibited negative price momentum.

The base index is composed of underlying assets, which consist of (i) nine underlying indices, potentially providing exposure to the following asset classes: focused U.S. equities; other developed market equities; developed market fixed income; emerging market equities; and commodities; and (ii) a money market position that accrues interest at a rate equal to the federal funds rate (the “return-based money market position”). The base index rebalances on each index business day based on historical returns of the underlying assets, subject to a limitation on realized volatility (which is separate from the volatility control mechanism described in the paragraph above) and minimum and maximum weights for the underlying assets and asset classes. As a result of the rebalancing, the base index may include as few as 2 underlying assets (including the return-based money market position) and may never include some of the underlying indices or asset classes.

The daily base index return is subject to a deduction equal to the return on the federal funds rate and, in addition, the entire index is subject to a deduction of 0.65% per annum (accruing daily).

The net effect of the deduction for the federal funds rate on the base index and the 0.65% deduction on the full index means that any aggregate exposure to the return-based money market position or the non-interest bearing cash positions will reduce the index performance on a pro rata basis by 0.65%. A very significant portion of the index has been, and may be in the future, allocated to the return-based money market position and the non-interest bearing cash positions.

The description above is only a summary. For a more detailed description of the index, including information about the fees and deductions that are applied to the index, see “Index Summary” beginning on page PS-3.

If your notes are not called, at maturity, for each $1,000 face amount of your notes, you will receive an amount in cash equal to:

|

• |

if the final index level is greater than or equal to the initial index level, the maximum settlement amount; or |

|

• |

if the final index level is less than the initial index level, $1,000. |

You should read the disclosure herein to better understand the terms and risks of your investment, including the credit risk of GS Finance Corp. and The Goldman Sachs Group, Inc. See page PS-15.

The estimated value of your notes at the time the terms of your notes are set on the trade date is expected to be between $885 and $935 per $1,000 face amount. For a discussion of the estimated value and the price at which Goldman Sachs & Co. LLC would initially buy or sell your notes, if it makes a market in the notes, see the following page.

|

Original issue date: |

expected to be August 3, 2022 |

Original issue price: |

100% of the face amount |

|

Underwriting discount: |

% of the face amount* |

Net proceeds to the issuer: |

% of the face amount |

* See “Supplemental Plan of Distribution; Conflicts of Interest” on page PS-64 for additional information regarding the fees comprising the underwriting discount.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense. The notes are not bank deposits and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency, nor are they obligations of, or guaranteed by, a bank.

Goldman Sachs & Co. LLC

Pricing Supplement No. dated , 2022.

The issue price, underwriting discount and net proceeds listed above relate to the notes we sell initially. We may decide to sell additional notes after the date of this pricing supplement, at issue prices and with underwriting discounts and net proceeds that differ from the amounts set forth above. The return (whether positive or negative) on your investment in notes will depend in part on the issue price you pay for such notes.

GS Finance Corp. may use this prospectus in the initial sale of the notes. In addition, Goldman Sachs & Co. LLC or any other affiliate of GS Finance Corp. may use this prospectus in a market-making transaction in a note after its initial sale. Unless GS Finance Corp. or its agent informs the purchaser otherwise in the confirmation of sale, this prospectus is being used in a market-making transaction.

|

About Your Prospectus The notes are part of the Medium-Term Notes, Series F program of GS Finance Corp. and are fully and unconditionally guaranteed by The Goldman Sachs Group, Inc. This prospectus includes this pricing supplement and the accompanying documents listed below. This pricing supplement constitutes a supplement to the documents listed below, does not set forth all the terms of your notes and therefore should be read in conjunction with such documents: •June 2022 MOBU Focus ER index supplement addendum dated June 27, 2022 •MOBU Focus ER index supplement no. 16 dated June 27, 2022 •Prospectus supplement dated March 22, 2021 •Prospectus dated March 22, 2021 The information in this pricing supplement supersedes any conflicting information in the documents listed above. In addition, some of the terms or features described in the listed documents may not apply to your notes. We refer to the notes we are offering by this pricing supplement as the “offered notes” or the “notes”. Each of the offered notes has the terms described below. Please note that in this pricing supplement, references to “GS Finance Corp.”, “we”, “our” and “us” mean only GS Finance Corp. and do not include its subsidiaries or affiliates, references to “The Goldman Sachs Group, Inc.”, our parent company, mean only The Goldman Sachs Group, Inc. and do not include its subsidiaries or affiliates and references to “Goldman Sachs” mean The Goldman Sachs Group, Inc. together with its consolidated subsidiaries and affiliates, including us. The notes will be issued under the senior debt indenture, dated as of October 10, 2008, as supplemented by the First Supplemental Indenture, dated as of February 20, 2015, each among us, as issuer, The Goldman Sachs Group, Inc., as guarantor, and The Bank of New York Mellon, as trustee. This indenture, as so supplemented and as further supplemented thereafter, is referred to as the “GSFC 2008 indenture” in the accompanying prospectus supplement. The notes will be issued in book-entry form and represented by master note no. 3, dated March 22, 2021. |

PS-2

The Goldman Sachs Momentum Builder® Focus ER Index (the index) measures the weighted performance of a base index composed of the underlying indices and a money market position (the return-based money market position), calculated on an excess return basis over the federal funds rate, together with non-interest bearing hypothetical cash positions that are not components of the base index. The non-interest bearing hypothetical cash positions arise either from the application of a 5% volatility control to the base index (the deleverage cash position) or a momentum risk control adjustment mechanism (the momentum risk control cash position). In addition to the base index deduction described above, the entire index is subject to a deduction of 0.65% per annum (accruing daily), as described below.

The index rebalances on each index business day from among 10 eligible underlying assets (considering the return-based money market position and non-interest bearing cash positions as a single eligible underlying asset) that have been categorized in the following asset classes: focused U.S. equities; other developed market equities; developed market fixed income; emerging market equities; commodities; and cash equivalent. The index attempts to track the positive price momentum in the eligible underlying assets (as defined below), subject to limitations on volatility, a minimum and maximum weight for each base index underlying asset and each asset class, and reduced exposure to the extent that the realized volatility of the base index exceeds a volatility control level of 5% or the volatility controlled index has exhibited negative price momentum, each as described below. The return-based money market position reflects the notional returns accruing to a hypothetical investor from an investment in a money market account denominated in U.S. dollars that accrues interest at the notional interest rate (a rate equal to the federal funds rate). As used in this index description, “realized volatility” is a measure of the degree of variation in historical returns.

On each index business day, the index is rebalanced as follows:

|

• |

First the base index is calculated. |

|

|

o |

The return of the base index reflects a deduction at the federal funds rate. |

|

• |

Next, the volatility control is applied to produce the “volatility controlled index” as an interim step. In applying the volatility control, exposure to the base index may be reduced by ratably allocating a portion of the base index exposure to the deleverage cash position to the extent that the realized volatility of the base index exceeds the volatility control level of 5%. |

|

|

o |

The return of the volatility controlled index reflects a deduction of 0.65% per annum (accruing daily). |

|

• |

Finally, the momentum risk control is applied to produce the index. In applying the momentum risk control, exposure to the volatility controlled index (and therefore to the base index) may be reduced by ratably allocating a portion of the index exposure to the momentum risk control cash position. |

|

|

o |

The portion of the index ratably allocated to the momentum risk control cash position reflects a deduction of 0.65% per annum (accruing daily). |

At this level, the deduction rate of 0.65% applies only to the momentum risk control cash position, rather than the index as a whole, because the deduction rate has already been factored into the calculation of the volatility controlled index. As a result, the deduction rate applies to the entire index.

Base Index Rebalancing

On each index business day (in the following contexts, a rebalancing day), the base index is rebalanced as follows:

|

• |

For each index business day, the hypothetical portfolios of eligible base index underlying assets (i.e., the eligible underlying indices and the return-based money market position) that would have provided the highest historical returns during each of three look-back periods (nine months, six months and three months) are calculated. The look-back periods are measured from (and excluding) the day which falls respectively nine (9), six (6) or three (3) calendar months before the third index business day prior to the given index business day (or, if any such date is not an index business day, the index business day immediately preceding such day) to (and including) the third index business day prior to the given index business day. Each portfolio is subject to (i) a 5% volatility limit (which may be relaxed in certain circumstances) on the degree of variation in the closing levels of the aggregate of such eligible base index underlying assets over the relevant look-back period and (ii) a minimum and maximum weight for each eligible base index underlying asset and each base index asset class. This results in three hypothetical portfolios of eligible base index underlying assets (one for each look-back period) for each index business day. |

|

• |

For each index business day, a target weight is calculated for each eligible base index underlying asset as the average of the weights of such eligible base index underlying asset in the three hypothetical portfolios. |

|

• |

For each rebalancing day, the weight of each eligible base index underlying asset for the base index rebalancing will equal the average of the target weights for such eligible base index underlying asset over the weight averaging period related to such rebalancing day. The weight averaging period for any rebalancing day will be the period from (but |

PS-3

|

excluding) the tenth index business day on which no index market disruption event occurs or is continuing with respect to any eligible base index underlying asset prior to such day to (and including) such day. |

|

• |

The basket of base index underlying assets resulting from the application of the weights calculated above is the base index. As a result of the constraints applied in its methodology, the base index may include as few as two eligible base index underlying assets (including the return-based money market position) and may not include some of the eligible base index underlying assets or base index asset classes during the entire term of the notes. The base index is calculated on an excess return basis, reflecting a deduction of the return that could be earned on a notional cash deposit at the notional interest rate, which is a rate equal to the federal funds rate. |

The following is a list of the eligible base index underlying assets for the index, including the related base index asset classes, base index asset class minimum and maximum weights and base index underlying asset minimum and maximum weights.

|

BASE INDEX ASSET CLASS |

BASE INDEX ASSET CLASS MINIMUM WEIGHT |

BASE INDEX ASSET CLASS MAXIMUM |

ELIGIBLE BASE INDEX UNDERLYING |

TICKER |

BASE INDEX UNDERLYING ASSET MINIMUM WEIGHT |

BASE INDEX UNDERLYING ASSET MAXIMUM WEIGHT |

|

Focused US Equities |

20% |

50% |

US Equity Futures Rolling Strategy Index |

FRSIUSE |

0%** |

30% |

|

US Technology Equity Futures Rolling Strategy Series Q Total Return Index |

GSISNQET |

0%** |

30% |

|||

|

Other Developed Market Equities |

0% |

50% |

European Equity Futures Rolling Strategy Index |

FRSIEUE |

0% |

30% |

|

Japanese Equity Futures Rolling Strategy Index |

FRSIJPE |

0% |

30% |

|||

|

Developed Market Fixed Income |

0% |

80% |

US Government Bond Futures Rolling Strategy Index |

FRSIUSB |

0% |

60% |

|

European Government Bond Futures Rolling Strategy Index |

FRSIEUB |

0% |

60% |

|||

|

Japanese Government Bond Futures Rolling Strategy Index |

FRSIJPB |

0% |

60% |

|||

|

Emerging Market Equities |

0% |

20% |

Emerging Markets Equity Futures Rolling Strategy Index |

FRSIEME

|

0%

|

20%

|

|

Commodities |

0% |

25% |

Bloomberg Gold Subindex Total Return |

BCOMGCTR |

0% |

25% |

|

Cash Equivalent |

0% |

80%* |

Return-Based Money Market Position |

N/A |

0% |

80%* |

* The base index asset class maximum weight and base index underlying asset maximum weight applicable to the Cash Equivalent in the table only apply to the return-based money market position in the base index, and not the deleverage cash position or the momentum risk control cash position (which are outside of the base index). As a result of the volatility control and momentum risk control adjustment features, the index may allocate nearly its entire exposure to hypothetical cash positions.

** Although the underlying asset weight of each of the US Large-Cap Equities (US Equity Futures Rolling Strategy Index) and US Technology Equities (US Technology Equity Futures Rolling Strategy Series Q Total Return Index) may be as low as 0%, their minimum combined weight must equal at least 20%.

Volatility Control

After a base index rebalancing, if on such rebalancing day the realized volatility of the base index’s excess returns (which take into account daily deductions at the notional interest rate) exceeds the volatility control level of 5%, the index will be rebalanced again in order to reduce such realized volatility to 5% by ratably reallocating a portion of the index exposure from the base index to the deleverage cash position.

The weighted basket resulting from the application of the volatility control is referred to as the “volatility controlled index”. The volatility controlled index measures the performance of the base index and the non-interest bearing deleverage cash position, with respective weights determined on each index business day as described above, minus 0.65% per annum (accruing daily).

The volatility measure used to calculate the volatility controlled index is based on the higher of two realized volatilities of base index excess returns using (i) a short-term “decay factor” of 0.94 giving relatively greater weight to more recent

PS-4

volatilities and (ii) a long-term “decay factor” of 0.97 giving relatively greater weight to older volatilities. Generally, a higher “decay factor” gives relatively greater weight to older data, reflecting a longer-term perspective. For a discussion of decay factors and other issues relating to the volatility control feature, see “The Index — What is realized volatility and how are the weights of the underlying assets influenced by it?”.

Momentum Risk Control

After a volatility controlled index rebalancing, if on such rebalancing day the volatility controlled index has exhibited negative price momentum (i.e., negative returns), the index will be rebalanced again by ratably reallocating a portion of the index exposure from the volatility controlled index to the momentum risk control cash position. Negative price momentum is deemed to occur if, on one or more index business days during the 21 index business day period from (but excluding) the 23rd index business day, to (and including) the 2nd index business day, prior to such rebalancing day, the volatility controlled index level is lower than its level 100 index business days prior to such day. Such 21 index business day period is defined as the momentum measurement period with respect to such rebalancing day, and each index business day in such period is defined as a momentum measurement day. The returns on the portion of the index allocated to the momentum risk control cash position are subject to a deduction of 0.65% per annum (accruing daily).

On any rebalancing day, the exposure of the index to the volatility controlled index will be based on a weighted percentage of the number of momentum measurement days during which the volatility controlled index level equals or exceeds its level on the 100th index business day preceding such momentum measurement day, with a value of 1 assigned to each momentum measurement day for which such condition is satisfied and a value of 0.25 assigned to each momentum measurement day for which such condition is not satisfied. For example, if the level of the volatility controlled index on each of the 21 momentum measurement days was greater than or equal to its level 100 index business days prior to such momentum measurement day, the index would be allocated 100% to the volatility controlled index and 0% to the momentum risk control cash position on such rebalancing day. Conversely, if the level of the volatility controlled index on each of the momentum measurement days was less than its level 100 index business days prior to such momentum measurement day, the index would be allocated 25% to the volatility controlled index and 75% to the momentum risk control cash position on such rebalancing day.

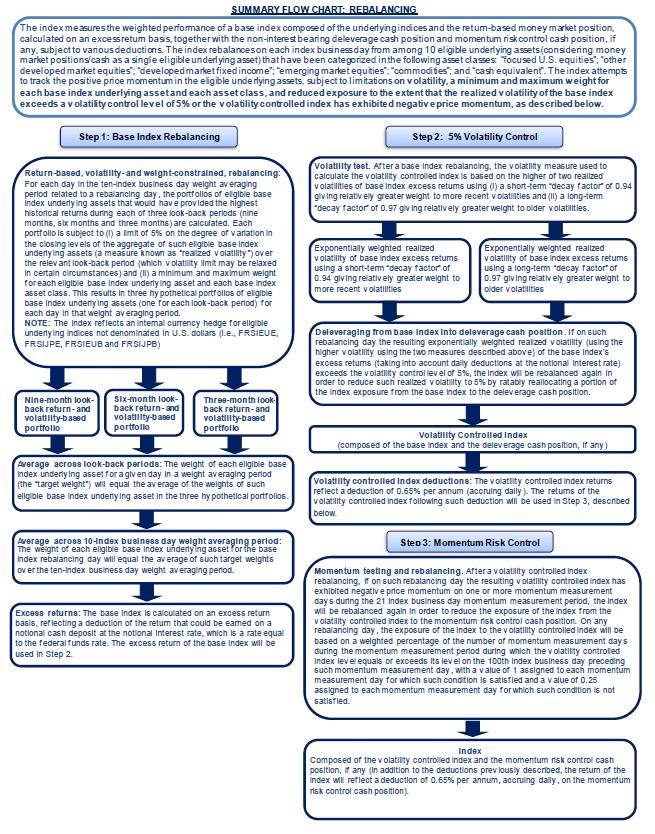

Index Values and Deductions

The image below depicts the calculation of the index values of each of the three layers of the index. This image is presented as a summary and should be read together with the more complete description of the calculation of the index immediately above.

|

• |

Base index: First, the orange innermost layer of the image represents the base index, which is comprised of the underlying indices and the return-based money market position (if any). The base index is calculated on an excess return basis, meaning that the return of the base index reflects a deduction of the return that could be earned on a notional cash deposit at the notional interest rate (a rate equal to the federal funds rate). The image shows that the value of the base index is based on the weighted sum of: |

|

|

o |

the performance of the underlying indices |

|

|

o |

plus the performance of any return-based money market position (which performance will equal the federal funds rate), less a deduction at the federal funds rate (applied to each base index component). |

|

• |

Volatility controlled index: Second, the green middle layer of the image represents the volatility controlled index, which is comprised of the base index and the deleverage cash position (if any) based on a measure of volatility. The image shows that the value of the volatility controlled index (composed of the base index and the deleverage cash position) is based on the weighted sum of: |

|

|

o |

the excess returns of the base index, as described above |

|

|

o |

plus a zero return attributable to any non-interest bearing deleverage cash position, less a deduction rate of 0.65% per annum (accruing daily) (applied to each component of the volatility controlled index). |

|

• |

Index: Finally, the blue outer layer of the image represents the index, which is comprised of the volatility controlled index and the momentum risk control cash position (if any) based on a measure of momentum. The image shows that the value of the index is based on the weighted sum of: |

|

|

o |

the performance of the volatility controlled index, as described above |

|

|

o |

plus a zero return attributable to the non-interest bearing momentum risk control cash position less a deduction rate of 0.65% per annum (accruing daily) that applies solely to the momentum risk control cash position (if any). |

At this level, the deduction rate of 0.65% applies only to the momentum risk control cash position, rather than the index as a whole, because the deduction rate has already been factored into the calculation of the volatility controlled index.

PS-5

As a result, any portion of the index attributable to a return-based money market position, a deleverage cash position or a momentum risk control cash position will effectively have a zero net return on an excess return basis before deducting 0.65% per annum (accruing daily) at the index level.

The final row of the image (no color) shows the cumulative impact of fees and deductions on each component of the index.

|

Index |

||||||

|

|

Volatility controlled index |

Momentum risk control cash position (if any)

|

||||

|

|

Base index |

Deleverage cash position (if any) |

||||

|

|

Underlying indices |

Return-based money market position (if any) |

||||

|

|

Returns |

+ underlying asset return* |

+ Fed Funds Rate |

0** |

0** |

|

|

Base index-level deductions |

- Fed Funds Rate |

Not applicable |

Not applicable |

|||

|

Volatility controlled index-level deductions |

- 0.65%/ annum |

Not applicable |

||||

|

Index-level deductions |

0 |

- 0.65%/ annum |

||||

|

Underlying Assets |

Underlying indices |

Return-based money market position (if any) |

Deleverage cash position (if any) |

Momentum risk control cash position (if any) |

||

|

Net Impact |

underlying asset return* – Fed Funds Rate – 0.65% / annum |

- 0.65%/ annum |

- 0.65%/ annum |

- 0.65%/ annum |

||

*The return contribution of the underlying indices to the base index is the weighted sum of underlying index returns weighted according to their respective weights in the base index, and the return contribution of the underlying indices to the index may be reduced by deleveraging of volatility controlled index exposure to the base index resulting from the application of the 5% volatility control to the base index or deleveraging of the index exposure to the volatility controlled index resulting from application of the momentum risk control adjustment mechanism to the volatility controlled index.

**The deleverage cash position and momentum risk control cash position represent hypothetical non-interest bearing cash positions. As neither position bears interest, the return attributable to these positions will always be zero.

Internal Currency Hedge

With respect to the eligible underlying assets denominated in a currency other than U.S. dollars (i.e., European Equity Futures Rolling Strategy Index (FRSIEUE), the Japanese Equity Futures Rolling Strategy Index (FRSIJPE), the European Government Bond Futures Rolling Strategy Index (FRSIEUB) and the Japanese Government Bond Futures Rolling Strategy Index (FRSIJPB)), the index reflects an internal simulated currency hedge, which, through a series of hypothetical currency hedging transactions, seeks to partially mitigate such eligible underlying assets’ exposure to exchange rate fluctuations in such currencies.

PS-6

CUSIP / ISIN: 40057MML0 / US40057MML09

Company (Issuer): GS Finance Corp.

Guarantor: The Goldman Sachs Group, Inc.

Index: Goldman Sachs Momentum Builder® Focus ER Index (current Bloomberg symbol: “GSMBFC5 Index”), or any successor index, as it may be modified, replaced or adjusted from time to time as provided herein

Face amount: $ in the aggregate on the original issue date; the aggregate face amount may be increased if the company, at its sole option, decides to sell an additional amount on a date subsequent to the trade date.

Authorized denominations: $1,000 or any integral multiple of $1,000 in excess thereof

Principal amount: Subject to redemption by the company as provided under “— Company’s redemption right (automatic call feature)” below, on the stated maturity date, the company will pay, for each $1,000 of the outstanding face amount, an amount in cash equal to the cash settlement amount

Cash settlement amount:

|

• |

if the final index level is greater than or equal to the initial index level, the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the maturity date return; or |

|

• |

if the final index level is less than the initial index level, $1,000. |

Initial index level (set on the trade date and may be higher or lower than the actual closing level of the index on that date):

Final index level: the closing level of the index on the determination date, subject to adjustment as provided in “— Consequences of a non-trading day” and “— Discontinuance or modification of the index” below

Company’s redemption right (automatic call feature): If a redemption event occurs, then the outstanding face amount will be automatically redeemed in whole and the company will pay an amount in cash on the following call payment date for each $1,000 of the outstanding face amount equal to the sum of (i) $1,000 plus (ii) the product of $1,000 times the applicable call return specified under “Call observation dates” below.

Redemption event: a redemption event will occur if, as measured on any call observation date, the closing level of the index is greater than or equal to the initial index level

Maturity date return: 50%

Call return: with respect to any call payment date, the applicable call return specified in the table set forth under “Call observation dates” below; as shown in such table, the call return increases the longer the notes are outstanding

Call payment dates (set on the trade date): expected to be the third business day after each call observation date. If a call observation date is postponed as described under “— Call observation dates” below, the related call payment date will be postponed by the same number of business day(s) from but excluding the originally scheduled call observation date to and including the actual call observation date.

Call observation dates (set on the trade date): expected to be the dates specified as such in the table below, commencing July 2023 and ending July 2026, unless the note calculation agent determines that such day is not a trading day. In that event, the applicable call observation date will be the first following trading day. In no event, however, will the applicable call observation date be postponed to a date later than the applicable originally scheduled call payment date or, if such originally scheduled call payment date is not a business day, later than the first business day after the applicable originally scheduled call payment date. If a call observation date is postponed to the last possible day for that period, but that day is not a trading day, that day will nevertheless be the applicable call observation date.

|

Call Observation Date |

Call Return |

|

July 31, 2023 |

10% |

|

July 29, 2024 |

20% |

|

July 29, 2025 |

30% |

|

July 29, 2026 |

40% |

Trade date: expected to be July 29, 2022

Original issue date (set on the trade date): expected to be August 3, 2022

PS-7

Determination date (set on the trade date): expected to be July 29, 2027, unless the note calculation agent determines that such day is not a trading day. In that event, the determination date will be the first following trading day. In no event, however, will the determination date be postponed to a date later than the originally scheduled stated maturity date or, if the originally scheduled stated maturity date is not a business day, later than the first business day after the originally scheduled stated maturity date. If the determination date is postponed to the last possible day, but such day is not a trading day, that day will nevertheless be the determination date.

Stated maturity date (set on the trade date): expected to be August 3, 2027, unless that day is not a business day, in which case the stated maturity date will be the next following business day. If the determination date is postponed as described under “— Determination date” above, the stated maturity date will be postponed by the same number of business day(s) from but excluding the originally scheduled determination date to and including the actual determination date.

Closing level of the index: the official closing level of the index or any successor index published by the index sponsor (including any index calculation agent acting on the index sponsor’s behalf) on any trading day for the index

Level of the index: at any time on any trading day, the official level of the index or any successor index published by the index sponsor (including any index calculation agent acting on the index sponsor’s behalf) at such time on such trading day

Business day: each Monday, Tuesday, Wednesday, Thursday and Friday that is not a day on which banking institutions in New York City generally are authorized or obligated by law, regulation or executive order to close

Trading day: a day on which the index is calculated and published by the index sponsor (including any index calculation agent acting on the index sponsor’s behalf). For the avoidance of doubt, if the index calculation agent determines that an index market disruption event occurs or is continuing on any day, such day will not be a trading day. A day is a scheduled trading day with respect to the index if, as of the trade date, the index is expected to be calculated and published by the index sponsor (including any index calculation agent acting on the index sponsor’s behalf) on such day.

Index calculation agent: Solactive AG or any replacement index calculation agent

Index sponsor: at any time, the person or entity, including any successor sponsor, that determines and publishes the index as then in effect (current index sponsor: Goldman Sachs & Co. LLC (“GS&Co.”)).

Successor index: any substitute index approved by the note calculation agent as a successor index as provided under “— Discontinuance or modification of the index” below

Underlying indices: with respect to the index, at any time, the indices that comprise the index as then in effect, after giving effect to any additions, deletions or substitutions.

Consequences of a non-trading day: If a day that would otherwise be the applicable originally scheduled call observation date or the originally scheduled determination date, as applicable, is not a trading day, then such call observation date or the determination date, as applicable, will be postponed as described under “— Call observation dates” or “— Determination date” above.

If the note calculation agent determines that the closing level of the index is not available on the last possible applicable call observation date or the final index level is not available on the last possible determination date because of a non-trading day or for any other reason (other than as described under “— Discontinuance or modification of the index” below), then the note calculation agent will nevertheless determine the level of the index based on its assessment, made in its sole discretion, of the level of the index on that day.

Discontinuance or modification of the index: If the index sponsor discontinues publication of the index and the index sponsor or anyone else publishes a substitute index that the note calculation agent determines is comparable to the index, or if the note calculation agent designates a substitute index, then the note calculation agent will determine the cash settlement amount payable on the stated maturity date or the amount payable on a call payment date, as applicable, by reference to the substitute index. We refer to any substitute index approved by the note calculation agent as a successor index.

If the note calculation agent determines that the publication of the index is discontinued and there is no successor index, the note calculation agent will determine the amount payable on the applicable call payment date or on the stated maturity date, as applicable, by a computation methodology that the note calculation agent determines will as closely as reasonably possible replicate the index.

If the note calculation agent determines that (i) the index or the method of calculating the index is changed at any time in any respect — including any addition, deletion or substitution and any reweighting or rebalancing of the index or the underlying indices and whether the change is made by the index sponsor under its existing policies or following a modification of those policies, is due to the publication of a successor index, is due to events affecting one or more of the

PS-8

underlying indices or its sponsor or is due to any other reason — and is not otherwise reflected in the level of the index by the index sponsor pursuant to the then-current index methodology of the index or (ii) there has been a split or reverse split of the index, then the note calculation agent will be permitted (but not required) to make such adjustments in the index or the method of its calculation as it believes are appropriate to ensure that the level of the index used to determine the amount payable on a call payment date or the stated maturity date, as applicable, is equitable.

All determinations and adjustments to be made by the note calculation agent with respect to the index may be made by the note calculation agent in its sole discretion. The note calculation agent is not obligated to make any such adjustments.

Note calculation agent (calculation agent): GS&Co.

Default amount: If an event of default occurs and the maturity of this note is accelerated, the company will pay the default amount in respect of the principal of this note at the maturity, instead of the amount payable on the stated maturity date as described earlier. The default amount for this note on any day (except as provided in the last sentence under “— Default quotation period” below) will be an amount, in the specified currency for the face amount of this note, equal to the cost of having a qualified financial institution, of the kind and selected as described below, expressly assume all of the company’s payment and other obligations with respect to this note as of that day and as if no default or acceleration had occurred, or to undertake other obligations providing substantially equivalent economic value to you with respect to this note. That cost will equal:

|

• |

the lowest amount that a qualified financial institution would charge to effect this assumption or undertaking, plus |

|

• |

the reasonable expenses, including reasonable attorneys’ fees, incurred by the holder of this note in preparing any documentation necessary for this assumption or undertaking. |

During the default quotation period for this note, which is described below, the holder of the notes and/or the company may request a qualified financial institution to provide a quotation of the amount it would charge to effect this assumption or undertaking. If either party obtains a quotation, it must notify the other party in writing of the quotation. The amount referred to in the first bullet point above will equal the lowest — or, if there is only one, the only — quotation obtained, and as to which notice is so given, during the default quotation period. With respect to any quotation, however, the party not obtaining the quotation may object, on reasonable and significant grounds, to the assumption or undertaking by the qualified financial institution providing the quotation and notify the other party in writing of those grounds within two business days after the last day of the default quotation period, in which case that quotation will be disregarded in determining the default amount.

Default quotation period: The default quotation period is the period beginning on the day the default amount first becomes due and ending on the third business day after that day, unless:

|

• |

no quotation of the kind referred to above is obtained, or |

|

• |

every quotation of that kind obtained is objected to within five business days after the day the default amount first becomes due. |

If either of these two events occurs, the default quotation period will continue until the third business day after the first business day on which prompt notice of a quotation is given as described above. If that quotation is objected to as described above within five business days after that first business day, however, the default quotation period will continue as described in the prior sentence and this sentence.

In any event, if the default quotation period and the subsequent two business day objection period have not ended before the determination date, then the default amount will equal the principal amount of this note.

Qualified financial institutions: For the purpose of determining the default amount at any time, a qualified financial institution must be a financial institution organized under the laws of any jurisdiction in the United States of America, Europe or Japan, which at that time has outstanding debt obligations with a stated maturity of one year or less from the date of issue and that is, or whose securities are, rated either:

|

• |

A-1 or higher by Standard & Poor’s Ratings Services or any successor, or any other comparable rating then used by that rating agency, or |

|

• |

P-1 or higher by Moody’s Investors Service, Inc. or any successor, or any other comparable rating then used by that rating agency. |

Overdue principal rate: the effective Federal Funds rate

Defeasance: not applicable

PS-9

DEFAULT AMOUNT ON ACCELERATION

If an event of default occurs and the maturity of your notes is accelerated, the company will pay the default amount in respect of the principal of your notes at the maturity, instead of the amount payable on the stated maturity date as described earlier. We describe the default amount under “Terms and Conditions” above. For the purpose of determining whether the holders of our Series F medium-term notes, which include your notes, are entitled to take any action under the indenture, we will treat the outstanding face amount of your notes as the outstanding principal amount of that note. Although the terms of the offered notes differ from those of the other Series F medium-term notes, holders of specified percentages in principal amount of all Series F medium-term notes, together in some cases with other series of our debt securities, will be able to take action affecting all the Series F medium-term notes, including your notes, except with respect to certain Series F medium-term notes if the terms of such notes specify that the holders of specified percentages in principal amount of all of such notes must also consent to such action. This action may involve changing some of the terms that apply to the Series F medium-term notes or waiving some of our obligations under the indenture. In addition, certain changes to the indenture and the notes that only affect certain debt securities may be made with the approval of holders of a majority in principal amount of such affected debt securities. We discuss these matters in the accompanying prospectus under “Description of Debt Securities We May Offer — Default, Remedies and Waiver of Default” and “Description of Debt Securities We May Offer — Modification of the Debt Indentures and Waiver of Covenants”.

PS-10

The following examples are provided for purposes of illustration only. They should not be taken as an indication or prediction of future investment results and are intended merely to illustrate the impact that the various hypothetical closing levels of the index on a call observation date and on the determination date could have on the amount of cash payable on a call payment date or on the stated maturity date, as the case may be, assuming all other variables remain constant.

The examples below are based on a range of index levels that are entirely hypothetical; no one can predict what the index level will be on any day throughout the life of your notes, and no one can predict what the closing level of the index will be on any call observation date or what the final index level will be on the determination date. The index has been highly volatile in the past — meaning that the index level has changed considerably in relatively short periods — and its performance cannot be predicted for any future period.

The information in the following examples assumes that the offered notes are purchased on the original issue date at the face amount and held to a call payment date or the stated maturity date, as the case may be. If you sell your notes in a secondary market prior to the stated maturity date, your return will depend upon the market value of your notes at the time of sale, which may be affected by a number of factors that are not reflected in the examples below such as the volatility of the index, the creditworthiness of GS Finance Corp., as issuer, and the creditworthiness of The Goldman Sachs Group, Inc., as guarantor. In addition, the estimated value of your notes at the time the terms of your notes are set on the trade date (as determined by reference to pricing models used by GS&Co.) is less than the original issue price of your notes. For more information on the estimated value of your notes, see “Additional Risk Factors Specific to Your Notes — The Estimated Value of Your Notes At the Time the Terms of Your Notes Are Set On the Trade Date (as Determined By Reference to Pricing Models Used By GS&Co.) Is Less Than the Original Issue Price Of Your Notes” on page PS-15 of this pricing supplement. The information in the examples also reflects the key terms and assumptions in the box below.

|

Key Terms and Assumptions |

|

|

Face amount |

$1,000 |

|

Call return |

The applicable call premium amount for each call payment date is specified on page PS-7 of this pricing supplement |

|

50% |

|

|

No non-trading day occurs on any originally scheduled call observation date or the originally scheduled determination date No change in or affecting any of the eligible underlying assets or the method by which the index sponsor calculates the index |

|

|

Notes purchased on original issue date at the face amount and held to a call payment date or the stated maturity date |

|

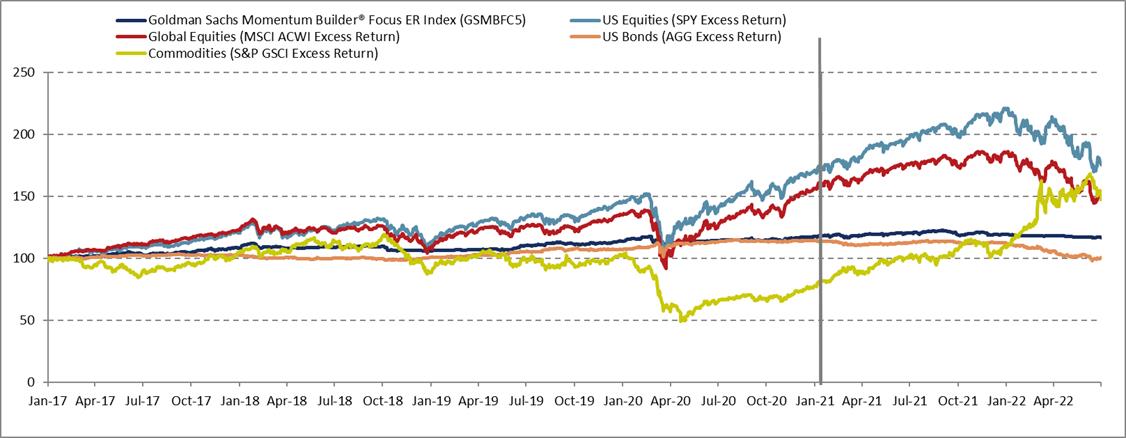

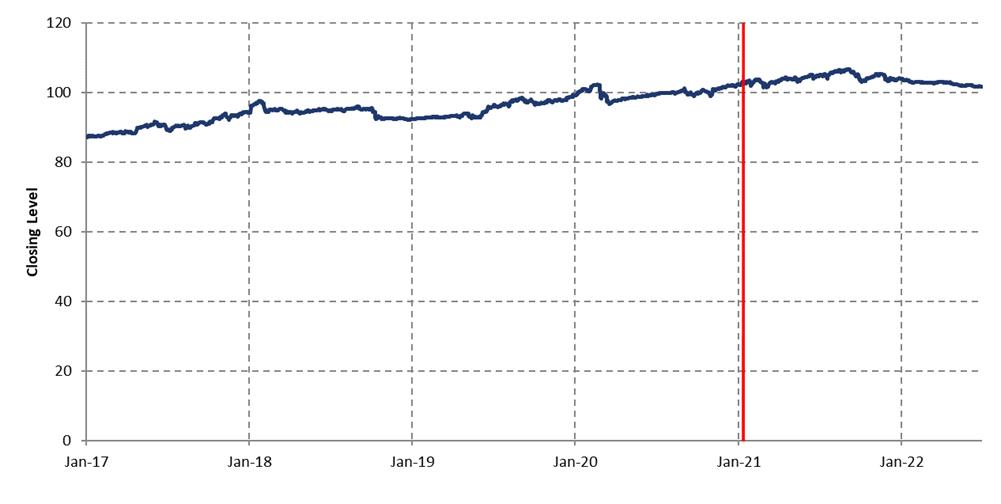

Moreover, we have not yet set the initial index level that will serve as the baseline for determining if the notes will be called and the amount that we will pay on your notes on the call payment date or at maturity. We will not do so until the trade date. As a result, the initial index level may differ substantially from the index level prior to the trade date. For these reasons, the actual performance of the index over the life of your notes, particularly on each call observation date and the determination date, as well as the amount payable at maturity, may bear little relation to the hypothetical examples shown below or to the historical index performance information or hypothetical performance data shown elsewhere in this pricing supplement. For information about the historical index performance levels and hypothetical performance data of the index during recent periods, see “The Index —Daily Closing Levels of the Index” on page PS-51. Before investing in the offered notes, you should consult publicly available information to determine the level of the index between the date of this pricing supplement and the date of your purchase of the offered notes.

Any rate of return you may earn on an investment in the notes may be lower than that which you could earn on a comparable investment in the index underlying assets.

Also, the hypothetical examples shown below do not take into account the effects of applicable taxes. Because of the U.S. tax treatment applicable to your notes, tax liabilities could affect the after-tax rate of return on your notes to a comparatively greater extent than the after-tax return on the underlying indices.

PS-11

Hypothetical Amount In Cash Payable on a Call Payment Date

The following examples reflect hypothetical amounts that you could receive on the applicable call payment dates. While there are four potential call payment dates with respect to your notes, the examples below only illustrate the amount you will receive, if any, on the first and second call payment date.

If, for example, your notes are automatically called on the first call observation date (i.e., on the first call observation date the closing level of the index is greater than or equal to the initial index level), the amount in cash that we would deliver for each $1,000 face amount of your notes on the applicable call payment date would be the sum of $1,000 plus the product of the applicable call return times $1,000. Therefore, for example, if the closing level of the index on the first call observation date were determined to be 120% of the initial index level, your notes would be automatically called and the amount in cash that we would deliver on your notes on the corresponding call payment date would be 110% of the face amount of your notes or $1,100 for each $1,000 face amount of your notes. Even if the closing level of the index on a call observation date exceeds the initial index level, causing the notes to be automatically called, the amount in cash payable on the call payment date will be limited due to the applicable call return.

If, for example, the notes are not automatically called on the first call observation date and are automatically called on the second call observation date (i.e., on the first call observation date the closing level of the index is less than the initial index level and on the second call observation date the closing level of the index is greater than or equal to the initial index level), the amount in cash that we would deliver for each $1,000 face amount of your notes on the applicable call payment date would be the sum of $1,000 plus the product of the applicable call return times $1,000. Therefore, for example, if the closing level of the index on the second call observation date were determined to be 140% of the initial index level, your notes would be automatically called and the amount in cash that we would deliver on your notes on the corresponding call payment date would be 120% of the face amount of your notes or $1,200 for each $1,000 face amount of your notes. Even if the closing level of the index on a call observation date exceeds the initial index level, causing the notes to be automatically called, the amount in cash payable on the call payment date will be limited due to the applicable call return.

PS-12

Hypothetical Cash Settlement Amount at Maturity

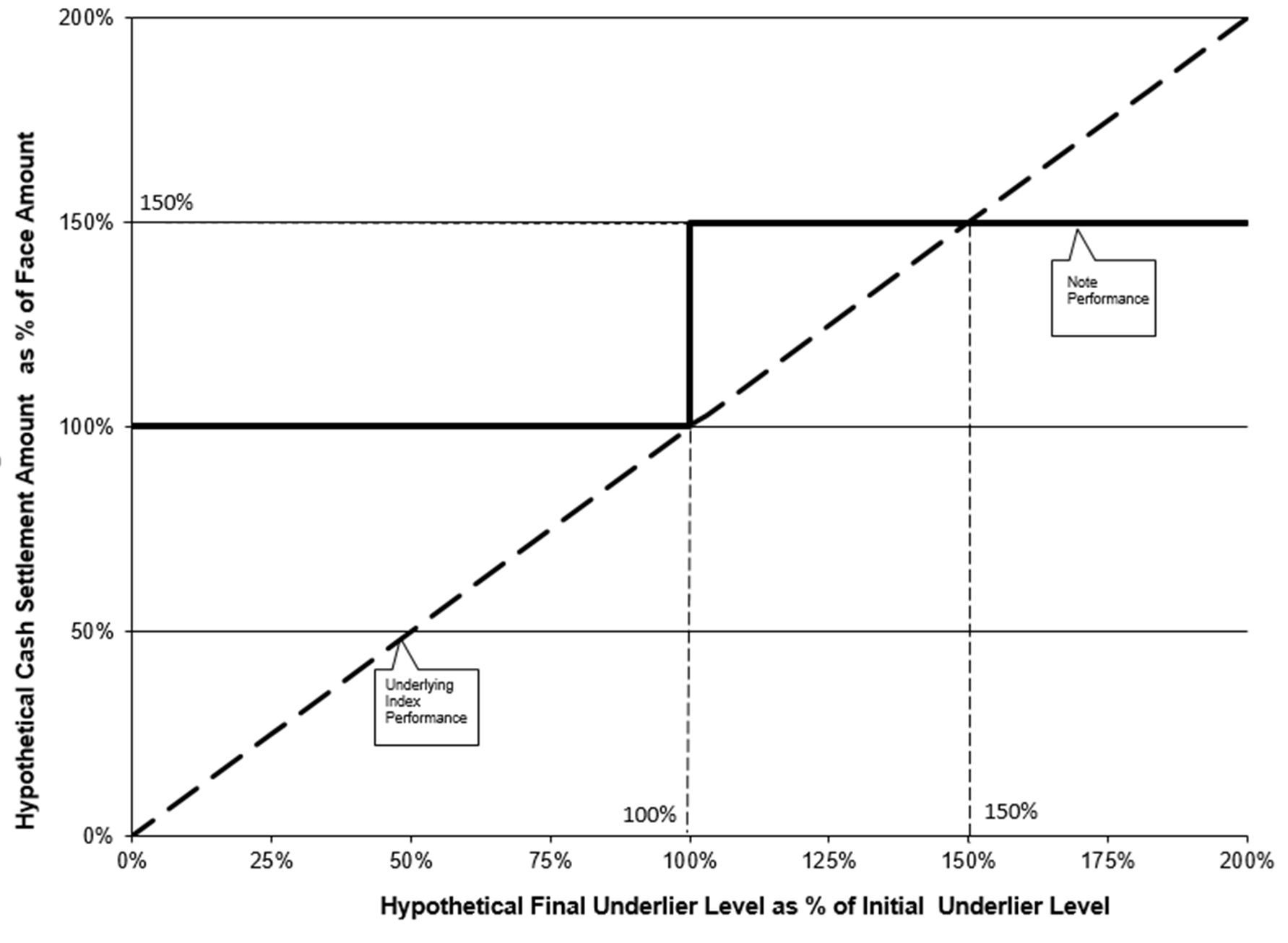

If the notes are not automatically called on any call observation date (i.e., on each call observation date the closing level of the index is less than the initial index level), the cash settlement amount we would deliver for each $1,000 face amount of your notes on the stated maturity date will depend on the performance of the index on the determination date, as shown in the table below. The table below shows the hypothetical cash settlement amounts that we would deliver on the stated maturity date in exchange for each $1,000 face amount of the notes if the final index level (expressed as a percentage of the initial index level) were any of the hypothetical levels shown in the left column.

The levels in the left column of the table below represent hypothetical final index levels and are expressed as percentages of the initial index level. The amounts in the right column represent the hypothetical cash settlement amounts, based on the corresponding hypothetical final index level, and are expressed as percentages of the face amount of a note (rounded to the nearest one-hundredth of a percent). Thus, a hypothetical cash settlement amount of 100.00% means that the value of the cash payment that we would deliver for each $1,000 of the outstanding face amount of the offered notes on the stated maturity date would equal 100.00% of the face amount of a note, based on the corresponding hypothetical final index level and the assumptions noted above.

The Notes Have Not Been Automatically Called

|

Hypothetical Final Index Level (as Percentage of Initial Index Level) |

Hypothetical Cash Settlement Amount (as Percentage of Face Amount) |

|

175.00% |

150.00% |

|

150.00% |

150.00% |

|

125.00% |

150.00% |

|

150.00% |

|

|

100.00% |

150.00% |

|

90.00% |

100.00% |

|

75.00% |

100.00% |

|

50.00% |

100.00% |

|

25.00% |

100.00% |

|

0.00% |

100.00% |

If, for example, the notes have not been automatically called on a call observation date and the final index level were determined to be 25.00% of the initial index level, the cash settlement amount that we would deliver on your notes at maturity would be 100.00% of the face amount of your notes, as shown in the table above. As a result, if you purchased your notes on the original issue date and held them to the stated maturity date, you would receive no return on your investment. In addition, if the notes have not been automatically called on a call observation date and the final index level were determined to be 175.00% of the initial index level, the cash settlement amount that we would deliver on your notes at maturity would be 150.00% of the face amount of your notes, as shown in the table above. As a result, if you held your notes to the stated maturity date, the cash settlement amount will be capped, and you would not benefit from any increase in the final index level over the initial index level on the determination date.

PS-13

The amounts shown above are entirely hypothetical; they are based on closing levels of the index that may not be achieved on a call observation date or the determination date, as the case may be, and on assumptions that may prove to be erroneous. The actual market value of your notes on a call payment date, the stated maturity date or at any other time, including any time you may wish to sell your notes, may bear little relation to the hypothetical amounts shown above, and these amounts should not be viewed as an indication of the financial return on an investment in the offered notes. The hypothetical amounts on notes held to a call payment date or the stated maturity date, as the case may be, in the examples above assume you purchased your notes at their face amount and have not been adjusted to reflect the actual issue price you pay for your notes. The return on your investment (whether positive or negative) in your notes will be affected by the amount you pay for your notes. If you purchase your notes for a price other than the face amount, the return on your investment will differ from, and may be significantly lower than, the hypothetical returns suggested by the above examples. Please read “Additional Risk Factors Specific to Your Notes — The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors” on page PS-17.

Payments on the notes are economically equivalent to the amounts that would be paid on a combination of other instruments. For example, payments on the notes are economically equivalent to a combination of a zero coupon bond bought by the holder and one or more options entered into between the holder and us (with one or more implicit option premiums paid over time). The discussion in this paragraph does not modify or affect the terms of the notes or the U.S. federal income tax treatment of the notes, as described elsewhere in this pricing supplement.

|

|

We cannot predict the actual closing levels of the index on each of the call observation dates or final index level on the determination date or what the market value of your notes will be on any particular trading day, nor can we predict the relationship between the index level and the market value of your notes at any time prior to the stated maturity date. The actual amount in cash that you will receive and the rate of return on the offered notes will depend on whether or not the notes are called, the actual initial index level, which we will set on the trade date, and the actual closing level of the index on each call observation date and the actual final index level on the determination date, each as determined by the note calculation agent as described above. Moreover, the assumptions on which the hypothetical examples are based may turn out to be inaccurate. Consequently, the amount in cash to be paid in respect of your notes on a call payment date or the stated maturity date, as the case may be, may be very different from the information reflected in the examples above. |

|

PS-14

ADDITIONAL RISK FACTORS SPECIFIC TO YOUR NOTES

|

|

An investment in your notes is subject to the risks described below, as well as the risks and considerations described in the accompanying index supplement, the accompanying prospectus supplement and the accompanying prospectus. You should carefully review these risks and considerations as well as the terms of the notes described herein and in the accompanying index supplement, the accompanying prospectus supplement and the accompanying prospectus. Your notes are a riskier investment than ordinary debt securities. Also, your notes are not equivalent to investing directly in any eligible underlying asset or the assets held by any eligible underlying index or in notes that bear interest at the notional interest rate. You should carefully consider whether the offered notes are appropriate given your particular circumstances. Although we have classified the risks described below into two categories (risk overview and risks related to the index), and the accompanying index supplement includes a third category of risks (risks related to the eligible underlying indices), the order and document in which any category of risks appears is not intended to signify any decreasing (or increasing) materiality of these risks. You should read all of the risks described below and in the accompanying index supplement, the accompanying prospectus supplement and the accompanying prospectus. |

|

Risk Overview

Risks Related to Structure, Valuation and Secondary Market Sales

The Estimated Value of Your Notes At the Time the Terms of Your Notes Are Set On the Trade Date (as Determined By Reference to Pricing Models Used By GS&Co.) Is Less Than the Original Issue Price Of Your Notes

The original issue price for your notes exceeds the estimated value of your notes as of the time the terms of your notes are set on the trade date, as determined by reference to GS&Co.’s pricing models and taking into account our credit spreads. Such estimated value on the trade date is set forth above under “Estimated Value of Your Notes”; after the trade date, the estimated value as determined by reference to these models will be affected by changes in market conditions, the creditworthiness of GS Finance Corp., as issuer, the creditworthiness of The Goldman Sachs Group, Inc., as guarantor, and other relevant factors. The price at which GS&Co. would initially buy or sell your notes (if GS&Co. makes a market, which it is not obligated to do), and the value that GS&Co. will initially use for account statements and otherwise, also exceeds the estimated value of your notes as determined by reference to these models. As agreed by GS&Co. and the distribution participants, this excess (i.e., the additional amount described under “Estimated Value of Your Notes”) will decline to zero on a straight line basis over the period from the date hereof through the applicable date set forth above under “Estimated Value of Your Notes”. Thereafter, if GS&Co. buys or sells your notes it will do so at prices that reflect the estimated value determined by reference to such pricing models at that time. The price at which GS&Co. will buy or sell your notes at any time also will reflect its then current bid and ask spread for similar sized trades of structured notes.

In estimating the value of your notes as of the time the terms of your notes are set on the trade date, as disclosed above under “Estimated Value of Your Notes”, GS&Co.’s pricing models consider certain variables, including principally our credit spreads, interest rates (forecasted, current and historical rates), volatility, price-sensitivity analysis and the time to maturity of the notes. These pricing models are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. As a result, the actual value you would receive if you sold your notes in the secondary market, if any, to others may differ, perhaps materially, from the estimated value of your notes determined by reference to our models due to, among other things, any differences in pricing models or assumptions used by others. See “— The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors” below.

The difference between the estimated value of your notes as of the time the terms of your notes are set on the trade date and the original issue price is a result of certain factors, including principally the underwriting discount and commissions, the expenses incurred in creating, documenting and marketing the notes, and an estimate of the difference between the amounts we pay to GS&Co. and the amounts GS&Co. pays to us in connection with your notes. We pay to GS&Co. amounts based on what we would pay to holders of a non-structured note with a similar maturity. In return for such payment, GS&Co. pays to us the amounts we owe under your notes.

In addition to the factors discussed above, the value and quoted price of your notes at any time will reflect many factors and cannot be predicted. If GS&Co. makes a market in the notes, the price quoted by GS&Co. would reflect any changes in market conditions and other relevant factors, including any deterioration in our creditworthiness or perceived creditworthiness or the creditworthiness or perceived creditworthiness of The Goldman Sachs Group, Inc. These changes may adversely affect the value of your notes, including the price you may receive for your notes in any market making transaction. To the extent that GS&Co. makes a market in the notes, the quoted price will reflect the estimated value determined by reference to GS&Co.’s pricing models at that time, plus or minus its then current bid and ask spread for similar sized trades of structured notes (and subject to the declining excess amount described above).

PS-15

Furthermore, if you sell your notes, you will likely be charged a commission for secondary market transactions, or the price will likely reflect a dealer discount. This commission or discount will further reduce the proceeds you would receive for your notes in a secondary market sale.

There is no assurance that GS&Co. or any other party will be willing to purchase your notes at any price and, in this regard, GS&Co. is not obligated to make a market in the notes. See “— Your Notes May Not Have an Active Trading Market” below.

The Notes Are Subject to the Credit Risk of the Issuer and the Guarantor

Although the return on the notes will be based on the performance of the index, the payment of any amount due on the notes is subject to the credit risk of GS Finance Corp., as issuer of the notes, and the credit risk of The Goldman Sachs Group, Inc., as guarantor of the notes. The notes are our unsecured obligations. Investors are dependent on our ability to pay all amounts due on the notes, and therefore investors are subject to our credit risk and to changes in the market’s view of our creditworthiness. Similarly, investors are dependent on the ability of The Goldman Sachs Group, Inc., as guarantor of the notes, to pay all amounts due on the notes, and therefore are also subject to its credit risk and to changes in the market’s view of its creditworthiness. See “Description of the Notes We May Offer — Information About Our Medium-Term Notes, Series F Program — How the Notes Rank Against Other Debt” on page S-5 of the accompanying prospectus supplement and “Description of Debt Securities We May Offer — Guarantee by The Goldman Sachs Group, Inc.” on page 67 of the accompanying prospectus.

You May Receive Only the Face Amount of Your Notes at Maturity

If the final index level is less than the initial index level on the determination date, the return on your notes will be limited to the face amount.

Even if the amount paid on your notes at maturity exceeds the face amount of your notes, the overall return you earn on your notes may be less than you would have earned by investing in a note with the same stated maturity that bears interest at the prevailing market rate.

Your Notes Do Not Bear Interest

You will not receive any interest payments on your notes. As a result, even if the cash settlement amount payable for your notes on the stated maturity date exceeds the face amount of your notes, the overall return you earn on your notes may be less than you would have earned by investing in a non-indexed debt security of comparable maturity that bears interest at a prevailing market rate.

The Amount In Cash That You Will Receive on a Call Payment Date or on the Stated Maturity Date is Not Linked to the Closing Level of the Index at Any Time Other Than on the Applicable Call Observation Date or the Determination Date, as the Case May Be

The amount in cash that you will receive on a call payment date, if any, will be paid only if the closing level of the index on the applicable call observation date is greater than or equal to the initial index level. Therefore, the closing level of the index on dates other than the call observation dates will have no effect on any amount paid in respect of your notes on the call payment date. In addition, the cash settlement amount you will receive on the stated maturity date (if the notes were not previously automatically called) will be based on the closing level of the index on the determination date and, therefore, the closing level of the index on dates other than the determination date will have no effect on any cash settlement amount paid in respect of your notes on the stated maturity date. Therefore, for example, if the closing level of the index dropped precipitously on the determination date, the cash settlement amount for the notes may be significantly less than it otherwise would have been had the cash settlement amount been linked to the closing level of the index prior to such drop. Although the actual closing level of the index on the applicable call payment dates, the stated maturity date or at other times during the life of the notes may be higher than the closing level of the index on the call observation dates or the final index level on the determination date, you will not benefit from the closing level of the index at any time other than on the call observation dates or on the determination date.

The Amount You Will Receive on a Call Payment Date or on the Stated Maturity Date, as the Case May Be, Will Be Limited

Regardless of the closing level of the index on a call observation date, the amount in cash that you may receive on the call payment date is limited. Even if the closing level of the index on a call observation date exceeds the initial index level, causing the notes to be automatically called, the amount in cash payable on the call payment date will be limited due to the applicable call return, regardless of the amount by which the closing level of the index on the call observation date exceeds the initial index level. If your notes are automatically called on a call observation date, the maximum payment you will receive for each $1,000 face amount of your notes will depend on the applicable call return. In addition, the cash settlement amount you may receive on the stated maturity date is capped due to the maturity date return.

PS-16

Your Notes Are Subject to Automatic Redemption

We will automatically call and redeem all, but not part, of your notes on a call payment date, if, as measured on any call observation date, the closing level of the index is greater than or equal to the initial index level. Therefore, the term for your notes may be reduced and you will not receive any further payments on the notes since your notes will no longer be outstanding. You may not be able to reinvest the proceeds from an investment in the notes at a comparable return for a similar level of risk in the event the notes are called prior to maturity. For the avoidance of doubt, if your notes are automatically called, no discounts, commissions or fees described herein will be rebated or reduced.

The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors

When we refer to the market value of your notes, we mean the value that you could receive for your notes if you chose to sell them in the open market before the stated maturity date. A number of factors, many of which are beyond our control, will influence the market value of your notes, including:

|

• |

the level and performance of the index, including the initial index level; |

|

• |

the volatility — i.e., the frequency and magnitude of changes — in the level of the index (even though the index attempts to limit volatility with daily rebalancing), the eligible underlying assets and the assets that comprise the eligible underlying indices; |

|

• |

the market prices of the eligible underlying indices; |

|

• |

the currency exchange rates of non-U.S. denominated eligible underlying indices; |

|

• |

the Federal Funds Rate and interest rates for non-U.S. currencies (8.5bps plus €STR with respect to euro-denominated eligible underlying indices and JPY-BOJ-TONAT with respect to the yen-denominated eligible underlying indices); |

|

• |

economic, financial, regulatory, political, military, public health and other events that affect markets generally and the assets held by the eligible underlying indices, and which may affect the closing levels of the index; |

|

• |

interest rates and yield rates in the market; |

|

• |

the time remaining until your notes mature; and |

|

• |

our creditworthiness and the creditworthiness of The Goldman Sachs Group, Inc., whether actual or perceived, including actual or anticipated upgrades or downgrades in our credit ratings or the credit ratings of The Goldman Sachs Group, Inc., or changes in other credit measures. |

In particular, the market value of your notes may be negatively impacted by increasing interest rates. Such adverse impact of increasing interest rates could be significantly enhanced in notes with longer-dated maturities, the market values of which are generally more sensitive to increasing interest rates.

These factors, and many other factors, will influence the price you will receive if you sell your notes before maturity, including the price you may receive for your notes in any market making transaction. If you sell your notes before maturity, you may receive less than the face amount of your notes.

You cannot predict the future performance of the index based on its historical performance or on any hypothetical performance data. The actual performance of the index over the life of the notes, as well as the cash settlement amount on the stated maturity date, may bear little or no relation to the historical index performance information, hypothetical performance data or hypothetical return examples shown elsewhere in this pricing supplement.

If You Purchase Your Notes at a Premium to Face Amount, the Return on Your Investment Will Be Lower Than the Return on Notes Purchased at Face Amount and the Impact of Certain Key Terms of the Notes Will Be Negatively Affected

The amount in cash that you will be paid for your notes on a call payment date or the stated maturity date will not be adjusted based on the issue price you pay for the notes. If you purchase notes at a price that differs from the face amount of the notes, then the return on your investment in such notes held to a call payment date or the stated maturity date will differ from, and may be substantially less than, the return on notes purchased at face amount. If you purchase your notes at a premium to face amount and hold them to a call payment date or the stated maturity date, the return on your investment in the notes will be lower than it would have been had you purchased the notes at face amount or a discount to face amount.

PS-17

You Have No Shareholder Rights or Rights to Receive Any Shares or Units of Any Eligible Underlying Index, or Any Assets Held by Any Eligible Underlying Index or the Money Market Position

Investing in the notes will not make you a holder of any shares or units of any eligible underlying index or any asset held by any eligible underlying index or the money market position. Investing in the notes will not cause you to have any voting rights, any rights to receive dividends or other distributions or any other rights with respect to any eligible underlying index, the assets held by any eligible underlying index or the money market position. Your notes will be paid in cash, and you will have no rights to receive delivery of any shares or units of any eligible underlying index or the assets held by any eligible underlying index.

The Note Calculation Agent Will Have the Authority to Make Determinations That Could Affect the Market Value of Your Notes, When Your Notes Mature and the Amount You Receive at Maturity

As of the date of this pricing supplement, we have appointed GS&Co. as the note calculation agent. As note calculation agent, GS&Co. will make all determinations and calculations relating to any amount payable on the note, which includes determinations regarding: the initial index level; the closing level of the index on the call observation dates, which we will use to determine whether your notes will be automatically called; the final index level on the determination date, which we will use to determine the amount we must pay on the stated maturity date; the call observation dates; whether to postpone any call observation date or the determination date because of a non-trading day; the determination date; the stated maturity date; business days; trading days and the default amount. The note calculation agent also has discretion in making certain adjustments relating to a discontinuation or modification of the index. See “Terms and Conditions — Discontinuance or modification of the index” above. The exercise of this discretion by GS&Co. could adversely affect the value of your notes and may present GS&Co. with a conflict of interest. We may change the note calculation agent at any time without notice and GS&Co. may resign as note calculation agent at any time upon 60 days’ written notice to GS Finance Corp.

Your Notes May Not Have an Active Trading Market

Your notes will not be listed or displayed on any securities exchange or included in any interdealer market quotation system, and there may be little or no secondary market for your notes. Even if a secondary market for your notes develops, it may not provide significant liquidity and we expect that transaction costs in any secondary market would be high. As a result, the difference between bid and asked prices for your notes in any secondary market could be substantial.

The Note Calculation Agent Can Postpone Any Call Observation Date or the Determination Date if a Non-Trading Day Occurs

If the note calculation agent determines that, on a day that would otherwise be a call observation date or the determination date, such day is not a trading day for the index, the applicable call observation date or the determination date, as applicable, will be postponed until the first following trading day, subject to limitation on postponement as described under “Terms and Conditions — Call observation dates” above and “Terms and Conditions — Determination Date” above. If any call observation date or the determination date is postponed to the last possible day and such day is not a trading day, such day will nevertheless be the applicable call observation date or the determination date, as applicable. In such a case, the note calculation agent will determine the closing level or the final index level, as applicable, based on the procedures described under “Terms and Conditions — Consequences of a non-trading day” above.

We May Sell an Additional Aggregate Face Amount of the Notes at a Different Issue Price

At our sole option, we may decide to sell an additional aggregate face amount of the notes subsequent to the date of this pricing supplement. The issue price of the notes in the subsequent sale may differ substantially (higher or lower) from the original issue price you paid as provided on the cover of this pricing supplement.

Risks Related to Conflicts of Interest

Hedging Activities by Goldman Sachs or Our Distributors May Negatively Impact Investors in the Notes and Cause Our Interests and Those of Our Clients and Counterparties to be Contrary to Those of Investors in the Notes