As filed with the Securities and Exchange Commission on March 3, 2014.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Opower, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 7372 | 26-0542549 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

1515 North Courthouse Road, 8th Floor

Arlington, Virginia 22201

703.778.4544

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Daniel Yates

Chief Executive Officer

Opower, Inc.

1515 North Courthouse Road, 8th Floor

Arlington, Virginia 22201

703.778.4544

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Richard A. Kline, Esq. Anthony J. McCusker, Esq. Joseph C. Theis, Esq. Goodwin Procter LLP 135 Commonwealth Drive Menlo Park, California 94025 650.752.3100 |

Michael Sachse, Esq. Senior Vice President and General Counsel Opower, Inc. 1515 North Courthouse Road, 8th Floor Arlington, Virginia 22201 703.778.4544 |

Mark R. Fitzgerald, Esq. Michael C. Labriola, Esq. Wilson Sonsini Goodrich & Rosati, Professional Corporation 1700 K Street NW, Fifth Floor Washington, District of Columbia 20006 202.973.8800 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(1)(2) |

Amount of registration fee | ||

| Common Stock, $0.000005 par value per share |

$100,000,000 | $12,880 | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the aggregate offering price of additional shares that the underwriters have the option to purchase to cover overallotments, if any. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to completion)

Issued , 2014

Shares

COMMON STOCK

Opower, Inc. is offering shares of its common stock. This is our initial public offering, and no public market currently exists for our shares. We anticipate that the initial public offering price of our common stock will be between $ and $ per share.

We have applied to list our common stock on the New York Stock Exchange under the symbol “OPWR.”

We are an “emerging growth company” under the U.S. federal securities laws and are subject to reduced public company reporting requirements. Investing in our common stock involves risks. See “Risk Factors” beginning on page 12.

PRICE $ A SHARE

| Price

to |

Underwriting |

Proceeds to Opower | ||||

| Per Share |

$ | $ | $ | |||

| Total |

$ |

$ | $ | |||

| (1) | See “Underwriters” for additional information regarding underwriting compensation. |

We have granted the underwriters the right to purchase up to an additional shares of common stock to cover over-allotments.

The Securities and Exchange Commission and any state securities regulators have not approved or disapproved of these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock to purchasers on , 2014.

| MORGAN STANLEY | GOLDMAN, SACHS & CO. | |

| Allen & Company LLC | Pacific Crest Securities | |

| Canaccord Genuity | Cowen and Company | |

, 2014

INFORMATION IS POWER

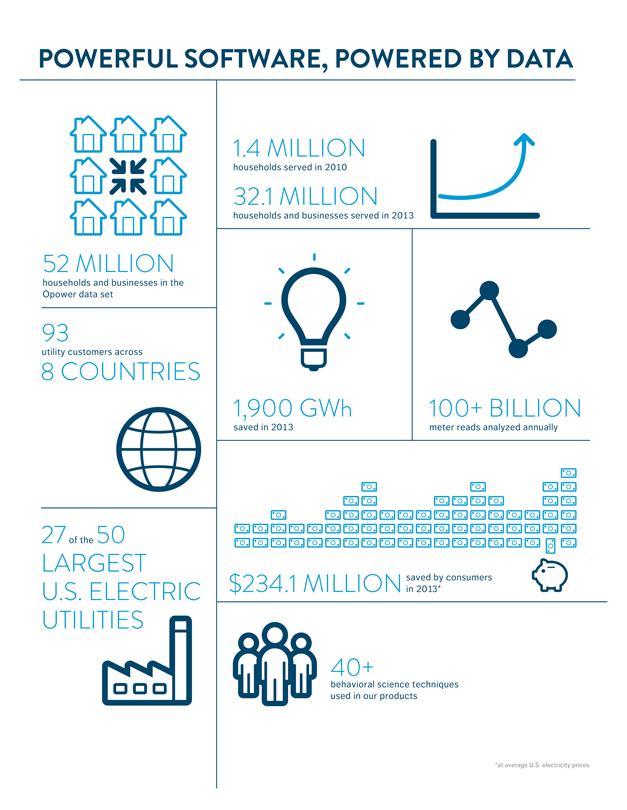

POWERFUL SOFTWARE, POWERED BY DATA 1.4 MILLION households served in 2010 32.1 MILLION households and businesses served in 2013 1,900 GWh saved in 2013 100+ BILLION meter reads analyzed annually $234.1 MILLIONsaved by consumers in 2013* 40+ behavioral science techniques used in our products *at average U.S. electricity prices 52 MILLION households and businesses in the Opower data set 93 utility customers across 8 COUNTRIES 27 of the 50 LARGEST U.S. ELECTRIC UTILITIES 52 MILLION households and businesses in the Opower data set

This is OPOWER

You should rely only on the information contained in this prospectus or contained in any free writing prospectus filed with the Securities and Exchange Commission. Neither we nor any of the underwriters have authorized anyone to provide any information or make any representations other than those contained in this prospectus or in any free writing prospectus filed with the Securities and Exchange Commission. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of the common stock. Our business, financial condition, results of operations and prospects may have changed since such date.

Through and including , 2014 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

For investors outside of the United States: Neither we nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. You are required to inform yourselves about, and to observe any restrictions relating to, this offering and the distribution of this prospectus outside of the United States.

i

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the sections titled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the related notes included elsewhere in this prospectus, before making an investment decision. Unless the context otherwise requires, the terms “Opower,” “the company,” “we,” “us,” and “our” in this prospectus refer to Opower, Inc.

OPOWER, INC.

Overview

Opower is a leading provider of cloud-based software to the $2.2 trillion utility industry. Utilities use our software platform to deliver key customer-facing applications that reduce energy demand and improve customer perception of the utility. Our software analyzes energy data and presents personalized insights to consumers in order to motivate reductions in energy consumption. These reductions are valued as a source of energy much like a conventional power plant. We believe that we are poised to transform the way the utility industry meets energy demand.

Utilities face two critical challenges that our software is built to address. First, utilities are under political, regulatory and environmental pressure to build fewer power plants, find cleaner sources of fuel and keep rates low. In order to accomplish these goals, utilities implement energy efficiency and demand response programs, which reduce overall and peak usage. Regulatory mechanisms support these programs by compensating utilities for reducing usage. Second, utilities need to strengthen their customer relationships. In many parts of the world, utilities compete for customers, and therefore customer engagement is critical. In regulated markets, which include much of the United States, regulators reward utilities for improving customer satisfaction. Utilities committed an estimated $11 billion to energy efficiency, demand response and customer engagement programs in 2013 in an effort to address these two challenges.

Our software is replacing low-tech and hardware-intensive products. Alternative efficiency programs today primarily consist of subsidies for energy efficient products, such as air conditioners and light bulbs. A common residential demand response program is a decades-old hardware switch connected to a pager network that shuts off the consumer’s air conditioner. Utility marketing efforts are often limited to traditional mass market approaches, such as bus stop advertisements and television commercials. We are able to replace these programs because our software offers measurable results and a better return on investment to utilities when scaled. Our approach has improved customer sentiment metrics by a median of 6% and up to 10% in some cases and we helped utilities and their customers save over 1,900 gigawatt hours of energy in 2013.

We can embed our solutions within utilities’ websites, mobile applications and customer service interfaces, and deliver individualized emails, text messages, automated phone calls and mail. In the design of these consumer touch points, we apply behavioral science insights to actionable patterns identified by our proprietary data analytics engine, which analyzes hundreds of billions of energy usage data points. Our cloud-based platform is extensible and configurable, a necessity to accommodate our customers’ diverse needs on a single code base.

We have developed four interconnected solutions on our platform:

| • | 2007: Opower Energy Efficiency – Reports and alerts, via mail and email, that compare consumers’ energy use to their neighbors’ and provide targeted energy saving recommendations. |

1

| • | 2010: Opower Customer Engagement – Web, mobile, digital alerts and customer service applications that improve customer experience and streamline operations. |

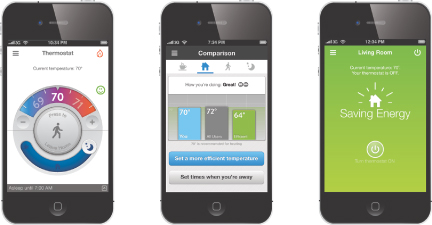

| • | 2012: Opower Thermostat Management – Mobile and web applications that connect to third-party thermostats in order to control and optimize peak and overall HVAC utilization. |

| • | 2013: Opower Demand Response – A zero-hardware solution consisting of near real-time text messages, email and automated phone alerts that motivates peak reductions in energy consumption. |

We generate revenue from utilities by selling primarily multi-year subscriptions to our software. As of December 31, 2013, we served 93 utility customers in eight countries, including 27 of the 50 largest electric utilities in the United States. We have the opportunity to expand within these existing customers; for example, the average penetration of our Energy Efficiency solution is approximately 10% of our utility clients’ customer base. We believe our addressable market includes 1,300 electric and gas utilities worldwide, serving 650 million households and 60 million businesses.

Because our clients often provide us all of their energy data even when launching smaller programs, we currently manage data representing 37% of all U.S. households. The scale and scope of this data enable us to better optimize the energy-saving performance of our programs and continually improve our pattern-matching algorithms. We share our proprietary cross-utility insights with our utility customers, and they see it as a valued benefit. We believe that as we grow, these network effects will continue to strengthen, and that these advantages give us a defensible leadership position.

We have experienced significant growth since our inception. Through our utility customers, we have increased the households we serve from 1.4 million in 2010 to 32.1 million in 2013. For the years ended December 31, 2011, 2012 and 2013, our revenue was $28.7 million, $51.8 million and $88.7 million, respectively, representing year-over-year revenue growth of 80% and 71%, respectively. We generated more than 90% of our revenue from annual recurring subscription fees in 2013. Because we believe our opportunity is large, we continue to invest significantly in our growth. As a result, we have generated net losses of $21.3 million, $12.3 million and $14.2 million in 2011, 2012 and 2013, respectively.

Utility Industry Background and Our Market Opportunity

Utilities operate in a highly regulated environment. Regulators review and approve capital expenditures and, in most markets, set the rates utilities charge their customers. In particular, regulators increasingly incentivize utilities to pursue energy efficiency and demand response, and place higher priority on better customer experience.

Key Industry Trends Affecting Utilities

Key trends affecting utilities include:

Regulators Prioritizing Energy Efficiency Over New Capacity. More than 25 U.S. states have enacted long-term energy efficiency resource standards, and these states account for over 61% of total U.S. electricity consumption. Similarly, the European Union adopted an Energy Efficiency Directive in October 2012 in order to ensure the achievement of its commitment to reduce emissions by 20% by 2020. In Asia and Latin America, rapid development, limited supply and government regulation and initiatives are also creating an imperative for energy saving measures.

Increasing Focus on Reducing Peak Demand. As it is for most large network providers, reducing peak demand is valuable for utilities. In fact, it has become even more valuable as peak supply prices have gone up and as changing regulations have made it easier to sell energy reductions on par with supply.

2

Changing Consumer Expectations. The widespread adoption of smartphones, mobile apps and social networking tools has changed the way consumers interact with their service providers. The change in consumer expectations has led utilities to seek new communication tools. As a result, utilities are looking for services that can improve their relationship with their customers.

Increasing Data Available to Utilities. Smart meter rollouts continue to accelerate globally. According to a January 2013 IMS Research report, smart meter penetration is expected to increase from 18% of all electricity meters in 2011 to 35% of all meters in 2016. Smart meters generate over 700 times more data than traditional meters, and this large increase creates an opportunity for utilities to offer new services and analytics-driven insights for their customers. In addition, the emergence of WiFi-enabled thermostats is likely to increase available energy data even further.

Increasing Competition. Over the past two decades, many countries and some U.S. states have separated the retail sale of energy from the generation, distribution and transmission of power. In these markets, competition among retail providers can be high, and customer retention is a challenge with some utilities experiencing customer churn of more than 25% per year. In noncompetitive, or regulated, energy markets, other providers, such as rooftop solar contractors, are entering the market with products and services that threaten to disintermediate the utility. All of these challenges mean that utilities must build deeper relationships with their customers.

The Opportunity for the Opower Solution

We believe our solutions give utilities greater returns than their historical options and, as a result, we expect to continue to grow our share of these large markets over time.

| • | Energy Efficiency. In the U.S. alone, utilities spent $6.9 billion on electric efficiency in 2012. Since 2007, this spending has grown at a 21% CAGR, according to a July 2013 report from the Institute for Electric Innovation. |

| • | Demand Response. The global demand response market is projected to grow from $3.0 billion in 2013 to $5.8 billion in 2020, representing a CAGR of 10%, according to a second quarter 2013 report published by Navigant Research. |

| • | Customer Engagement. We believe that customer engagement is at the intersection of a number of markets for utilities, including customer billing and information systems, home energy management solutions and smart grid analytics. These markets are expected to grow from $4.1 billion in 2013 to $12.1 billion in 2020, representing a 17% CAGR, according to Navigant Research and Greentech Media. |

Our solutions address a portion of each of these markets. Based on our internal analysis and industry experience, we estimate our addressable market opportunity to be at least $11 billion annually. Our newest solutions, Thermostat Management and Demand Response, offer significant growth potential, but both are still in a nascent stage with an immaterial impact on our revenue to date.

Key Benefits to Utilities

The key benefits utilities derive from our solutions include:

Low Cost, Large Scale Energy Efficiency. We are able to cost-effectively drive energy efficiency results across millions of homes. As a result, for some utilities, our efficiency solution has become their single biggest source of residential energy savings.

Low Cost, Large Scale Residential Demand Response. Our software enables utilities to scale residential peak demand reductions by rapidly communicating with energy consumers.

3

Improved Customer Satisfaction. Utilities have implemented our user-friendly solutions to increase customer satisfaction. We have surveyed over 30,000 energy consumers who receive our solutions. These consumers consistently report greater trust in their utility as a source of information, and they believe that the utility wants to help them save energy and money.

Reduced Cost to Serve. Utilities spend $6 billion annually on customer service. With our digital solutions, utilities can communicate with their customers through web and mobile applications, making interactions more cost effective and efficient. We believe this reduces customer service costs. Customer service software has been reducing the cost of service for a wide set of industries, but the utility industry has lagged behind.

Better Customer Engagement Technology. Our platform gives utilities the ability to deploy state-of-the-art technology for their customer communications, allowing them to reach and engage their customers across multiple channels with minimal effort. Much as next generation customer relationship management (“CRM”) software and digital marketing software have delivered significant value to enterprises globally, our solutions help utilities strengthen their relationships with their customers.

Network Effects. We have six years of experience working with industry leading utilities. Our large and growing energy dataset combined with our significant industry experience has caused many utilities to view us as a source of third-party benchmarking and industry knowledge.

Our Differentiated Approach

The key components of our differentiated approach are:

Highly Scalable Data Analytics Engine. We have built what we believe to be the most sophisticated data engine serving utilities. As of December 31, 2013, we have collected energy data from 52 million households and businesses aggregated from our utility customers. Our data analytics engine can process and analyze our vast data set and provide personalized insights to the households and businesses that our utility customers serve.

Cloud-Based Architecture. Our solutions are built on a cloud-based architecture and delivered through web and mobile applications, text message, email, phone and mail. We maintain a single version of our code base, which means that all of our customers receive new features and updates simultaneously. In an industry that is accustomed to long-term investments, the fact that our software is regularly updated at no added cost is a significant benefit.

Intuitive User Experience Informed by Behavioral Science. An intuitive user experience and behavioral science are at the core of all of our solutions. We seek to change the habits of consumers by presenting realistic goals, encouragement and rewards. We use more than 40 behavioral science techniques such as loss language, normative comparisons and reciprocity to encourage utility customers to optimize their energy consumption.

Track Record of Measurable Results. We design our products to deliver measurable outcomes, which are necessary for utilities to meet their energy efficiency and demand response targets. We have 189 client years of results, and we believe this track record gives us a significant advantage over our competitors. Our approach to savings has been approved by regulators in 30 states, and that track record has strengthened our brand.

4

Our Growth Strategy

The key elements of our growth strategy include:

Expand With Existing Customers. We see a significant opportunity to grow our revenue simply by expanding our presence within our existing customer base. Currently, our energy efficiency reports are deployed to approximately 10% of households that our utility customers serve. Most of our utility customers initially purchase only one of our four solutions, and deploy that initial solution to only a portion of their customers. Because all of our easily integrated products help utilities improve their engagement with energy consumers, we believe that utilities will derive even greater benefits as they deploy additional solutions. Moreover, once a utility begins to send us its data, we can more easily roll out programs to additional households and businesses.

Win New Customers Globally. As of December 31, 2013, we had 93 utility customers in eight countries, yet we believe that there are approximately 1,300 utilities that could benefit from our solutions. To reach more of these potential customers, we are expanding our sales, marketing and regulatory efforts, in particular internationally.

Develop New Offerings on Our Industry Data Platform. Since we are a trusted partner, our customers often ask us to develop new offerings to meet their growing needs. These requests are increasingly central to our plans for growth. We have made, and will continue to make, significant investments to augment our platform to capture adjacent opportunities.

Focus on Gas and Electric Consumer Outcomes. From the outset, we have designed products that can deliver measurable changes in consumer behavior, which has been core to our success. We believe we can achieve more both with our existing solutions and through new products. We have focused and will continue to focus our research and development efforts to continue to improve outcomes for gas and electric consumers.

Risks Affecting Us

Our business, financial condition, results of operations and prospects are subject to numerous risks. These risks include:

| • | We have a history of losses and we may not achieve or sustain profitability on a quarterly or annual basis. |

| • | Sales and implementation cycles to our customers can be lengthy and unpredictable. |

| • | We operate in a highly regulated business environment. |

| • | We are dependent on the utility industry, which has experienced increased and changing regulations. |

| • | A limited number of our utility customers are responsible for a significant portion of our bookings, revenue and cash flow. |

| • | We have experienced rapid growth and organizational change in recent periods. |

| • | The market for our products and solutions is still developing. |

| • | Utilities in critical markets may fail to collect data or may be unable to collect current data that we require to provide our products and solutions. |

| • | Our quarterly results are inherently unpredictable and subject to substantial fluctuations. |

| • | We operate in a competitive industry. |

5

Corporate Information

We were incorporated in Delaware in 2007. Our principal executive offices are located at 1515 North Courthouse Road, 8th Floor, Arlington, Virginia 22201, and our telephone number is (703) 778-4544. Our website address is www.opower.com. Information contained on or that can be accessed through our website does not constitute part of this prospectus and inclusions of our website address in this prospectus are inactive textual references only.

“Opower” is our registered trademark in the United States, Australia, Canada, the European Community, Japan and New Zealand. Other trademarks and trade names referred to in this prospectus are the property of their respective owners.

6

| Common stock offered by us |

shares | |

| Common stock to be outstanding after this offering |

shares | |

| Option to purchase additional shares from us |

We have granted the underwriters an option, exercisable for 30 days after the date of this prospectus, to purchase up to an additional shares from us. | |

| Use of proceeds |

We estimate that the net proceeds from the sale of shares of our common stock that we are selling in this offering will be approximately $ million (or approximately $ million if the underwriters’ option to purchase additional shares in this offering is exercised in full), based upon an assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions and estimated offering expenses payable by us. | |

| We currently intend to use the net proceeds of this offering for working capital and other general corporate purposes, including investing further in our sales and marketing and research and development efforts. We intend to use proceeds from this offering to further grow our business and to fund our growth strategies discussed in this prospectus. We may also use a portion of the net proceeds to acquire or invest in complementary businesses, products, services, technologies or other assets. See “Use of Proceeds” for additional information. | ||

| Concentration of ownership |

Upon completion of this offering, our executive officers and directors, and their affiliates, will beneficially own, in the aggregate, approximately % of our outstanding shares of common stock. | |

| Risk factors |

See “Risk Factors” for a discussion of factors you should carefully consider before deciding to invest in our common stock. | |

| New York Stock Exchange trading symbol |

“OPWR” | |

The number of shares of common stock that will be outstanding after this offering is based on 41,359,839 shares outstanding as of December 31, 2013, and excludes:

| • | 7,789,720 shares of common stock issuable upon the exercise of options to purchase common stock that were outstanding as of December 31, 2013, with a weighted-average exercise price of $3.83 per share; |

7

| • | 1,093,326 shares of common stock issuable upon the vesting of restricted stock units that were outstanding as of December 31, 2013; |

| • | 283,950 shares of common stock issuable upon the vesting of restricted stock units that were granted after December 31, 2013; |

| • | shares of common stock issuable upon the conversion of the subordinated convertible promissory note with a utility partner dated March 8, 2013, based on an assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus; and |

| • | 6,529,852 shares of common stock reserved for future issuance under our stock-based compensation plans, consisting of 1,529,852 shares of common stock reserved for future issuance under our 2007 Stock Plan as of December 31, 2013, which shares will be added to the shares to be reserved under our 2014 Stock Incentive Plan, and 5,000,000 shares of common stock reserved for future issuance under our 2014 Stock Incentive Plan, which will become effective in connection with this offering, and shares that become available pursuant to provisions thereof that automatically increase the share reserves under the 2014 Stock Incentive Plan each year. |

Except as otherwise indicated, all information in this prospectus assumes:

| • | the automatic conversion of all outstanding shares of our convertible preferred stock into an aggregate of 19,246,714 shares of common stock, the conversion of which will occur immediately prior to the completion of this offering; |

| • | the filing and effectiveness of our amended and restated certificate of incorporation in Delaware and the adoption of our amended and restated bylaws, each of which will occur immediately prior to the completion of this offering; and |

| • | no exercise by the underwriters of their option to purchase up to an additional shares of common stock from us in this offering. |

8

The following tables summarize our historical financial data. We have derived the summary statement of operations data for the years ended December 31, 2011, 2012 and 2013 and the balance sheet data as of December 31, 2013 from our audited financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future. The following summary financial and other data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes included elsewhere in this prospectus.

| Year Ended December 31, | ||||||||||||

| 2011 | 2012 | 2013 | ||||||||||

| (In thousands, except per share amounts) |

||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||

| Revenue |

$ | 28,746 | $ | 51,756 | $ | 88,703 | ||||||

| Cost of revenue(1) |

13,306 | 18,913 | 31,304 | |||||||||

|

|

|

|

|

|

|

|||||||

| Gross profit |

15,440 | 32,843 | 57,399 | |||||||||

| Operating expenses(1): |

||||||||||||

| Sales and marketing |

13,648 | 21,338 | 30,551 | |||||||||

| Research and development |

14,372 | 16,134 | 27,087 | |||||||||

| General and administrative |

8,716 | 7,730 | 13,578 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total operating expenses |

36,736 | 45,202 | 71,216 | |||||||||

|

|

|

|

|

|

|

|||||||

| Operating loss |

(21,296 | ) | (12,359 | ) | (13,817 | ) | ||||||

| Other income (expense), net |

(1 | ) | 54 | (321 | ) | |||||||

|

|

|

|

|

|

|

|||||||

| Loss before income taxes |

(21,297 | ) | (12,305 | ) | (14,138 | ) | ||||||

| Provision for income taxes |

— | 27 | 23 | |||||||||

|

|

|

|

|

|

|

|||||||

| Net loss |

$ | (21,297 | ) | $ | (12,332 | ) | $ | (14,161 | ) | |||

|

|

|

|

|

|

|

|||||||

| Weighted-average common stock outstanding(2): |

||||||||||||

| Basic and diluted |

17,836 | 19,442 | 21,121 | |||||||||

| Net income (loss) per share(2): |

||||||||||||

| Basic and diluted |

$ | (1.19 | ) | $ | (0.63 | ) | $ | (0.67 | ) | |||

| Pro forma weighted-average common stock outstanding(2): |

||||||||||||

| Basic and diluted |

||||||||||||

| Pro forma net loss per share (unaudited)(2): |

||||||||||||

| Basic and diluted |

$ | |||||||||||

| (1) | Stock-based compensation was allocated as follows: |

| Year Ended December 31, | ||||||||||||

| 2011 | 2012 | 2013 | ||||||||||

| (In thousands) | ||||||||||||

| Cost of revenue |

$ | 87 | $ | 137 | $ | 197 | ||||||

| Sales and marketing |

340 | 484 | 1,348 | |||||||||

| Research and development |

382 | 447 | 939 | |||||||||

| General and administrative |

151 | 119 | 1,141 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total stock-based compensation |

$ | 960 | $ | 1,187 | $ | 3,625 | ||||||

|

|

|

|

|

|

|

|||||||

| (2) | See Note 10 to our audited financial statements for an explanation of the method used to calculate basic and diluted net loss per share attributable to common stockholders, pro forma basic and diluted net loss per share attributable to common stockholders and the weighted-average number of shares used in the computation of the per share amounts. |

9

| December 31, 2013 | ||||||||||||

| Actual | Pro Forma(1) | Pro Forma

As Adjusted(2)(3) |

||||||||||

| (In thousands) | ||||||||||||

| Balance Sheet Data: |

||||||||||||

| Cash and cash equivalents |

$ | 28,819 | $ | $ | ||||||||

| Working capital (deficit) |

(11,851 | ) | ||||||||||

| Property and equipment, net |

10,813 | |||||||||||

| Total assets |

63,135 | |||||||||||

| Deferred revenue |

52,390 | |||||||||||

| Total indebtedness |

3,673 | |||||||||||

| Total stockholders’ equity (deficit) |

(6,263 | ) | ||||||||||

| (1) | The pro forma column in the balance sheet data table above gives effect to (i) the filing of our amended and restated certificate of incorporation, (ii) the automatic conversion of all outstanding shares of our convertible preferred stock into an aggregate of 19,246,714 shares of common stock and (iii) the automatic conversion of all outstanding debt under a subordinated convertible promissory note with a utility partner dated March 8, 2013 into shares of common stock, based on an assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, which conversion will occur prior to the completion of this offering, as if such conversion had occurred on December 31, 2013. |

| (2) | The pro forma as adjusted column in the balance sheet data table above gives effect to the pro forma adjustments set forth in footnote 1 above and the sale and issuance by us of shares of common stock in this offering at an assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. |

| (3) | Each $1.00 increase or decrease in the assumed initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, would increase or decrease, as applicable, the cash and cash equivalents, working capital (deficit), total assets and total stockholders’ equity (deficit) by $ million, assuming that the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same, and after deducting estimated underwriting discounts and commissions payable by us. An increase or decrease of 1.0 million shares in the number of shares offered by us would increase or decrease, as applicable, the cash and cash equivalents, working capital (deficit), total assets and total stockholders’ equity (deficit) by $ million assuming an initial public offering price of $ per share, which is the midpoint of the estimated offering price range set forth on the cover page of this prospectus, and after deducting estimated underwriting discounts and commissions payable by us. |

| Year Ended December 31, | ||||||||||||

| 2011 | 2012 | 2013 | ||||||||||

| (In thousands) | ||||||||||||

| Other Financial Metrics: | ||||||||||||

| Adjusted EBITDA |

$ | (19,710 | ) | $ | (9,573 | ) | $ | (6,426 | ) | |||

To provide investors with additional information regarding our financial results, we have disclosed in the table above and within this prospectus adjusted EBITDA, a non-GAAP financial measure. We have provided a reconciliation below between adjusted EBITDA and net loss, the most directly comparable financial measure as measured in accordance with U.S. generally accepted accounting principles (“GAAP”).

We have included adjusted EBITDA in this prospectus because it is a key measure used by our management to evaluate our operating performance, generate future operating plans and make strategic decisions. Accordingly, we believe that adjusted EBITDA provides useful information to investors and others in understanding and evaluating our results of operations in the same manner as our management and board of directors.

10

While we believe that this non-GAAP financial measure is useful in evaluating our business, this information should be considered as supplemental in nature and is not meant as a substitute for the related financial information prepared in accordance with GAAP. Some of these limitations are:

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized may have to be replaced in the future and adjusted EBITDA does not reflect cash capital expenditure requirements for such replacements or for new capital expenditure requirements; |

| • | adjusted EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | adjusted EBITDA does not include the impact of stock-based compensation; |

| • | adjusted EBITDA does not reflect income tax payments that may represent a reduction in cash available to us; and |

| • | other companies, including companies in our industry, may calculate adjusted EBITDA differently or not at all, which reduces its usefulness as a comparative measure. |

We believe it is useful to exclude non-cash charges, such as depreciation and amortization and stock-based compensation, from our adjusted EBITDA because the amount of such expenses in any specific period may not directly correlate to the underlying performance of our business operations.

Because of the aforementioned limitations, you should consider adjusted EBITDA alongside other financial performance measures, including net loss, cash flow metrics and our financial results presented in accordance with GAAP. The following table presents a reconciliation of net loss to adjusted EBITDA for each of the periods indicated:

| Year Ended December 31, | ||||||||||||

| 2011 | 2012 | 2013 | ||||||||||

| (In thousands) | ||||||||||||

| Reconciliation of Net Loss to Adjusted EBITDA: |

||||||||||||

| Net loss |

$ | (21,297 | ) | $ | (12,332 | ) | $ | (14,161 | ) | |||

| Provision for income taxes |

— | 27 | 23 | |||||||||

| Other (income) expense, including interest |

1 | (54 | ) | 321 | ||||||||

| Depreciation and amortization |

626 | 1,599 | 3,766 | |||||||||

| Stock-based compensation |

960 | 1,187 | 3,625 | |||||||||

|

|

|

|

|

|

|

|||||||

| Adjusted EBITDA |

$ | (19,710 | ) | $ | (9,573 | ) | $ | (6,426 | ) | |||

|

|

|

|

|

|

|

|||||||

11

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information in this prospectus, before making a decision to invest in our common stock. If any of the risks actually occur, our business, financial condition, results of operations and prospects could be harmed. In that event, the trading price of our common stock could decline, and you could lose part or all of your investment.

Risks Related to Our Business

We have a history of losses and anticipate continued losses and negative operating cash flow for the foreseeable future, and we may not achieve or sustain profitability on a quarterly or annual basis.

We have incurred significant losses to date, with an accumulated deficit of $83.2 million as of December 31, 2013. For the years ended December 31, 2011, 2012 and 2013, we incurred net losses of $21.3 million, $12.3 million and $14.2 million, respectively. We expect these losses to continue. We also anticipate negative operating cash flow for the foreseeable future, as we expect to incur significant operating expenses in connection with the continued development and expansion of our business. Many of these expenses relate to prospective customers that may never contract with us, as well as products that may not be introduced, that we may choose to discontinue, that may fail to achieve desired results or that may not generate revenue until later periods, if at all. We may not achieve or sustain profitability on a quarterly or annual basis.

Sales cycles and implementation times can be lengthy and unpredictable and require significant employee time and financial resources.

Sales cycles for our products tend to be long and unpredictable. Even after we have convinced prospective customers of the need for, and value of, our products and solutions, our customers are large organizations that frequently have extensive budgeting, procurement, competitive bidding, technical and performance reviews and regulatory approval processes that can slow down the sales process by months or even years. Utilities may choose, and many historically have chosen, to follow industry trends rather than be early adopters of new products or solutions, which can extend the lead time for or prevent acceptance of more recently introduced products or solutions such as ours. In many instances, a utility may require one or more pilot programs to test our products and solutions before committing to a larger deployment. These pilot programs may be quite lengthy and provide no assurance that they will lead to a larger deployment or future sales. The implementation and deployment of our solutions can be unpredictable due to contract negotiations and challenges with implementation, or critical dependencies, such as the installation of other products, including smart meters. Furthermore, the implementation and deployment of new products and solutions may require troubleshooting, which requires additional time and resources from us and our customers. These delays may lengthen our sales cycles.

Our sales cycle is typically 6 months to 24 months. This extended sales, implementation and deployment process requires our senior management and our sales and marketing and customer services personnel to dedicate significant time to sales, and to use significant financial resources without any assurance of success or recovery of our related expenses.

The lengthy sales cycle also makes it difficult to forecast new customer implementations and deployments, as well as the volume and timing of future agreements, which, in turn, makes forecasting our future results of operations challenging. In the event that we publicly disclose any forecasts of our future results of operations or other forward-looking metrics, and those forecasts ultimately turn out to be inaccurate, the value of our common stock could significantly decline.

12

We provide services to utilities that operate in a highly regulated business environment, and regulatory requirements or need for regulatory approval could delay or reduce demand for our products, impose costs on us or make our products less attractive to our customers.

Our customers, products and solutions are subject to many federal, state, local and foreign laws and regulations. In many cases, our customers are subject to direct oversight from Public Utility Commissions, Public Service Commissions, Independent System Operators, the Federal Energy Regulatory Commission or other regulatory entities primarily focused on the energy utility sector. Applicable laws and regulations govern, among other things, utility demand for energy efficiency and demand response solutions, the data that we are able to handle and collect, utility structuring and incentives, the utility’s ability to spend money on our products and solutions and the methods and manners that we can use to contact utility customers. Depending on the solutions sought, prospective customers may be required to gain approval from any of these organizations prior to implementing our solutions, which could delay our ability to collect cash and recognize revenue.

We are dependent in part on regulations on the utility industry, and the changing regulatory landscape could alter our customers’ buying patterns.

The utility industry has been subject to increasing and changing regulations in recent years. We derive substantially all of our revenue from sales of products and solutions directly and indirectly to utilities, and this complex and difficult landscape poses a risk to us. We have experienced, and may in the future experience, variability in our results of operations on an annual and a quarterly basis as a result of these factors. Going forward, these factors could harm our financial condition and cash flows.

Changes in the regulatory conditions could reduce a customer’s interest in or ability to implement our products and solutions. Examples of market dynamics driven by regulation include:

| • | energy efficiency goals; |

| • | interpretations of the energy savings credit attributed to our products; |

| • | regulated compensation associated with energy efficiency; |

| • | demand response goals; |

| • | rules concerning the peak reductions attributed to our products; |

| • | regulated compensation associated with demand response; |

| • | smart metering or advanced meter infrastructure deployments; and |

| • | data privacy. |

Many regulatory jurisdictions have implemented rules that provide financial incentives for the implementation of energy efficiency and demand response technologies, either by providing rebates or through the restructuring of utility rates. In the past, we have seen demand for our solutions altered by changes in regulation. We have also had to limit or alter our offerings to comply with regulatory requirements, and these changes have affected our revenue. In addition, deregulation may change the incentives for our customers or prospective customers to use our solutions. If changes in regulation reduce or negatively alter the demand for our solutions, our business and results of operations could be harmed. In order to counteract this risk, we have invested significant time and effort in understanding and attempting to impact government decisions that we believe will affect our market. These efforts, however, have not always been successful and may not succeed in the future.

13

If we fail to respond to evolving technological changes, our products and solutions could become obsolete or less competitive.

Our industry is highly competitive and characterized by new and rapidly evolving technologies, techniques, standards, regulations, customer requirements and frequent product introductions. Accordingly, our results of operations depend upon, among other things, our ability to develop and introduce new products and solutions, as well as our ability to improve existing products. The process of developing new technologies and products is complex. If we are unable to develop enhancements to, and new features for, our existing products or if we are unable to develop new products that keep pace with technological developments or industry standards, our business could be harmed.

We continue to invest in new product offerings and the success of those offerings is uncertain. A few examples of such product development challenges are:

| • | Over the last three years, we have invested significant resources in developing a thermostat offering. We have yet to see a significant return from that investment, as our development and sales growth has been slowed by market challenges. These challenges may continue, and our investment in this area may not yield returns. |

| • | We are developing an offering tailored specially for small and medium-sized businesses. The market for this offering is unproven, and our ability to successfully deliver the results our customers seek is uncertain. |

| • | We have invested considerable resources in developing a demand response offering. While the early results have been promising, it is possible that the market could be smaller than we have expected or that our product will not function as intended. |

| • | We also have other products in development; it is possible that none of those products will prove to be successful. |

All of our research and development efforts are dependent upon our ability to deliver products and functionality in a timely and efficient manner. In the past, we have experienced delays delivering products, and while we have taken steps to improve the predictability of our research and development efforts, those efforts may not be successful. If we continue to experience delays in our ability to deliver new products and functionality, our business and growth rates would suffer.

Our success depends in part on our ability to deliver measurable outcomes, and our business may be harmed if our products became less effective or our results are questioned.

Our products deliver valuable measurable outcomes for our customers and receive favorable treatment from their regulators, both of which are important to our customers. Our ability to deliver expected results is dependent on numerous factors, including but not limited to the effectiveness of our approach and products, the cost of alternate sources of energy savings, the availability of data and our ability to effectively reach energy consumers. We may not be able to continue to deliver valuable measurable outcomes or we may find that our programs yield diminishing returns over time. In addition, it is possible that regulators will change their view of our results in a way that might harm our business overall. For example, if regulators were to treat our energy savings as less significant or less reliable than other efficiency programs, or if regulators were to alter how utilities are compensated for working with us, our business and results of operations may be harmed. If our ability to deliver results were to change, or if regulators were to view our results less favorably, our brand, business and results of operations may be harmed.

Because we recognize subscription revenue over the term of the contract, downturns or upturns in new sales will not be immediately reflected in our results of operations and may be difficult to discern.

We generally recognize subscription revenue from customers ratably over the terms of their contracts, which typically range from one to five years. As a result, most of the subscription revenue we report in each

14

quarter is derived from the recognition of deferred revenue relating to subscriptions entered into during previous periods. Consequently, a decline in new or renewed subscriptions in any single quarter will likely have only a small impact on our revenue results for that quarter, but will negatively affect our revenue in future quarters. Accordingly, the effect of significant downturns in sales and market acceptance of our solutions, and potential changes in our pricing policies or rates of renewals, may not be fully reflected in our results of operations until future periods. We may be unable to adjust our cost structure to reflect the changes in revenue. In addition, a significant majority of our costs are expensed as incurred. As a result, increased growth in the number of our customers could result in our recognition of more costs than revenue in the earlier periods of the terms of our agreements. Our subscription model also makes it difficult for us to rapidly increase our revenue through additional sales in any period, as revenue from new customers must be recognized over the applicable subscription term.

A limited number of our utility customers are responsible for a significant portion of our revenue and cash flow. A decrease in sales to these utility customers or delays in customer implementation and deployments could harm our results of operations and financial condition.

We operate in a large and concentrated market. A substantial portion of our revenue, profitability and cash flow depends on a limited number of utility customers, and we cannot easily replace a lost customer. As a result, there may be significant variability in our quarterly results if we were to lose one or more of our large customers.

For the year ended December 31, 2012, our ten largest customers by revenue represented 61% of our total revenue, with two clients, National Grid and Pacific Gas and Electric Company (“PG&E”), representing more than 10% of our total revenue at 15% and 14%, respectively. For the year ended December 31, 2013 our ten largest customers by revenue represented 62% of our total revenue, with three clients, National Grid, PG&E, and Exelon each representing more than 10% of our total revenue at 14%, 13% and 11%, respectively. Many of our fees are not due until we have actually begun to deliver our solutions and, as a result, are subject to delay. We have contracted to provide multiple services to National Grid, PG&E and Exelon, including processing and analyzing data and displaying results to their customers. We entered into an implementation and licensing agreement with National Grid in June 2009, which was renewed and now expires in December 2015, and a renewed application services agreement with PG&E in December 2012 with a term of 3 years. We have also entered into multiple agreements with Exelon subsidiaries, including Baltimore Gas & Electric (“BGE”), PECO and Commonwealth Edison. We entered into an agreement with BGE in March 2011 with an initial term expiring in February 2015 and a renewed agreement with Commonwealth Edison in February 2011 with a term expiring in May 2014, subject to certain additional limitations on the initial term. National Grid, PG&E, BGE and Commonwealth Edison may generally terminate their respective agreements in each case for cause upon written notice of certain uncured material breaches of contract by us, upon the bankruptcy or insolvency of the other party or under certain other circumstances. In addition, National Grid, PG&E, BGE and Commonwealth Edison may generally terminate their respective agreements for convenience upon prior written notice.

We expect that a limited number of utility customers will continue to account for a substantial portion of our revenue in future periods. Changes in the business requirements, vendor selection or purchasing behavior of our utility customers could significantly decrease our sales.

Many of our customer agreements provide our customers with the ability to terminate the agreement for convenience, which may limit our ability to forecast our revenue accurately or could harm our results of operations and financial condition.

Many of our customer agreements, including National Grid and PG&E, are subject to customer termination for any reason, including for the customer’s convenience following a specified notice period. In limited circumstances, we may be required to provide refunds or sales credits in addition to the loss of future revenue from these customers. If customers terminate their agreements with us for convenience, our results of operations may be harmed and our revenue forecasts may be incorrect.

15

We have experienced rapid growth and organizational change in recent periods. If we fail to manage our growth effectively, our financial performance may suffer.

We have substantially expanded our overall business, customer base, employee headcount and operations in recent periods both domestically and internationally. We increased our total number of full-time employees from 162 employees as of December 31, 2010 to 465 employees as of December 31, 2013. Our expansion has placed, and our expected future growth will continue to place, a significant strain on our managerial, customer operations, research and development, sales and marketing, manufacturing, administrative, financial and other resources. We anticipate further growth in headcount will be required to address increases in our solution offerings and continued expansion. Our success will depend in part upon the ability of our management team to manage this growth effectively. To do so, we must continue to recruit, hire, train, manage and integrate a significant number of qualified managers and employees in specialized roles within our company, including in technology, sales and marketing. If our new employees perform poorly, or if we are unsuccessful in recruiting, hiring, training, managing and integrating these new employees, or retaining these or our existing employees, our business and results of operations may suffer.

In addition, to manage the expected growth of our headcount and operations, we will need to continue to improve our operational, financial, management and information technology infrastructure. Our anticipated additional headcount and capital investments will increase our costs, which will make it more difficult for us to address any future revenue shortfalls by reducing expenses in the short term. If we are unable to manage our growth successfully, our business and results of operations will be harmed.

The market for our products and solutions is still developing. If the market does not develop as quickly or as much as we expect, our business and growth rates could be harmed.

The market for our products and solutions is still developing, and it is uncertain whether our products and solutions will achieve and sustain high levels of demand and market acceptance, both domestically and internationally. Our near-term and long-term success will depend to a substantial extent on the willingness and ability of utilities, both domestically and internationally, to pursue energy efficiency, demand response and customer engagement programs. Utilities’ activities are governed by regulatory agencies, including public utility commissions, which may not create a regulatory environment that is conducive to the implementation of energy efficiency or demand response in a particular jurisdiction. Indeed, currently many utilities lack the economic motivation, regulatory requirements or financial incentives to deploy our technology. If utilities do not pursue energy efficiency, demand response or customer engagement or do so in fewer numbers or more slowly than we expect, our business and results of operations would be harmed.

Utilities in critical markets may fail to collect data or may be unable to collect current data that we require to provide our products and solutions.

Our cloud-based platform is dependent upon receiving specific data inputs from our customers such as current energy usage data. Without those inputs, our platform may be less reliable or effective or may not work and we may not be able to provide effective solutions. In markets where energy usage data is infrequently collected or where access to that data is restricted, including in international markets, we may prove unable to provide our products and solutions, or we may be forced to alter our products and solutions in a manner that reduces our ability to derive revenue from them. For example, the processes for data collection in Europe are still developing, and as a result, data may be more difficult to obtain or more expensive to access. If we are unable to access current data from our customers, our business and results of operations may be harmed.

Our quarterly results are inherently unpredictable and subject to substantial fluctuations and, as a result, we may fail to meet the expectations of securities analysts and investors, which could harm the trading price of our common stock.

Our results of operations, including our revenue, profitability and cash flows, may vary significantly from quarter to quarter due to a number of factors, many of which are outside of our control. While our revenue has increased in recent periods, our revenue may not continue to increase or may decrease on a quarterly or annual basis.

16

Factors that may affect the unpredictability of our quarterly results and cause our stock price to fluctuate include, but are not limited to:

| • | long, and sometimes unpredictable, sales and customer implementation and deployment cycles; |

| • | changes in the mix of products and solutions sold; |

| • | our dependence on a limited number of customers; |

| • | the timing of deployment of our products and solutions by our customers, which can have a material effect on when we recognize related revenue under our revenue recognition policies; |

| • | changing market and competitive conditions; |

| • | failures of our solutions that may harm our reputation or result in contractual penalties or terminations; |

| • | product or project failures by our customers that result in the cancellation, slowing down or deferring of projects; |

| • | changes to our cost structure, including changes to our cost of postage, data acquisition, data storage and management, data security and labor; |

| • | delays in adopting our solutions associated with data privacy concerns; |

| • | changes in laws or regulations, directly affecting either our operations, those of our customers or utility consumers; |

| • | delays in regulatory approvals for our utility customers and utility customer implementations and deployments; |

| • | political and consumer sentiment and the related impact on the scope and timing of deployment of our products and solutions; |

| • | economic, regulatory and political conditions in the markets where we operate or anticipate operating; |

| • | the addition of new employees; and |

| • | extraordinary expenses such as litigation or other dispute-related settlement payments. |

As a result, we believe that quarter-to-quarter comparisons of our results of operations are not necessarily a good indication of what our future performance will be. It is likely that in some future quarters our results of operations may be below the expectations of securities analysts or investors, in which case the price of our common stock would likely decline.

We operate in a competitive industry and our market share and results of operations may be harmed if we are unable to respond to our competitors effectively.

Competition in our market involves rapidly changing technologies, evolving regulatory requirements and industry expectations, frequent new product introductions and changes in customer requirements. To maintain and improve our competitive position, we must keep pace with the evolving needs of our utility customers and continue to develop and introduce new products, features and solutions in a timely and efficient manner. We compete with software suppliers to utilities. Our key competitors currently include Aclara, C3 Energy, Nest Labs (which was acquired by Google), Oracle, SAP and Tendril, as well as many other smaller providers. Certain of these companies have, and future competitors may have, substantially greater financial, marketing, technological and other resources than we do.

Additionally, we compete with energy efficiency providers that provide utilities with other efficiency programs and demand response companies that offer programs specifically focused on reduction in peak capacity. If these programs become more cost effective, it would harm our business. For example, if the cost of alternative efficiency approaches, such as light bulb replacement subsidies or home retrofits, decreased or if utilities could more easily deploy those measures on a large scale, our business could be harmed.

17

We have also seen many companies imitate our products, solutions and tactics, and we expect that trend to continue. As we look to expand into new markets, we expect to face additional competitors that may be more established in specific geographies. We anticipate that in the future, additional competitors will emerge that offer a broad range of competing products and solutions.

Our business and financial performance could be harmed by changes in tax laws or regulations.

New income, sales, use or other tax laws, statutes, rules, regulations or ordinances could be enacted at any time. Those enactments could harm our domestic and international business operations, and our business and financial performance. Further, existing tax laws, statutes, rules, regulations or ordinances could be interpreted, changed, modified or applied adversely to us. These events could require us or our utility customers to pay additional tax amounts on a prospective or retroactive basis, as well as require us or our utility customers to pay fines and/or penalties and interest for past amounts deemed to be due. If we raise our prices to offset the costs of these changes, existing and potential future utility customers may elect not to purchase our products and solutions in the future. Additionally, new, changed, modified or newly interpreted or applied tax laws could increase our utility customers’ and our compliance, operating and other costs, as well as the costs of our products. Further, these events could decrease the capital we have available to operate our business. The occurrence of any or all of these events could harm our business and results of operations.

In addition, we may be subject to sales, use and income tax audits by many tax jurisdictions throughout the world, many of which have not established clear guidance on the tax treatment of software-as-a-service based companies. Although we believe our income tax liabilities are reasonably estimated and accounted for in accordance with applicable laws and principles, an adverse resolution of one or more uncertain tax positions in any period could have a material impact on the results of operations for that period.

Our results of operations may be harmed if we are required to collect sales taxes for our products and solutions in jurisdictions where we have not historically done so.

Historically, we have not collected sales tax from our customers nor have we remitted such taxes in many states where we sell our products and solutions. Although we believe we are not obligated to collect sales taxes from our customers in those jurisdictions, states or one or more countries may seek to impose sales or other tax collection obligations on us, including for past sales by us or our utilities. A successful assertion that we should be collecting additional sales or other taxes on our products or solutions could discourage customers from purchasing our solutions or otherwise harm our business and results of operations.

We rely on our management team and need additional key personnel to grow our business, and the loss of key employees or inability to hire key personnel could harm our business.

Our success and future growth depend on the skills, working relationships and continued services of our management team and other key personnel. The loss of any member of our senior management team, and in particular our Chief Executive Officer, President or other key executives, could harm our business. All of our officers are at-will employees, which means they may terminate their employment relationship with us at any time, and their knowledge of our business and industry would be extremely difficult to replace.

Volatility or lack of performance in our stock price may affect our ability to retain our senior management and key personnel. Many of our longest-tenured employees, including members of our senior management and other key personnel with deep institutional knowledge, hold significant vested stock options and shares of our common stock. Employees may be more likely to leave us if the shares they own or the shares underlying their vested stock options have significantly appreciated in value relative to the original purchase prices of the shares or the exercise prices of the options, or if the exercise prices of the options that they hold are significantly above the market price of our common stock. As a result of these factors, we may be unable to attract or retain qualified personnel. Our inability to retain the necessary personnel to run and grow our business could harm our business and results of operations.

18

In addition, our future success will depend on our ability to attract, retain and motivate highly skilled management, product development, operations, sales, engineering and other personnel in the United States and abroad. Competition for these types of personnel is intense and we have experienced periods where we had difficulty hiring for critical roles. In particular, we have struggled at times to attract and hire sales executives and software developers who meet our standards. Even if we are able to hire qualified individuals, we may be unable to retain such individuals. Furthermore, if we hire from competitors or other companies, their former employers may attempt to assert that these employees or we have breached legal obligations, resulting in a diversion of our time and resources.

Postal charges are one of our most significant costs. If postal rates or mailing costs increase, our cost of delivering our solutions could increase.

In each country where we deliver mailed paper reports, we are dependent upon the government mail carrier to deliver our products. We have very little ability to control postal expenses and a change in postal expenses could have a significant impact on our business. For example, the United States Postal Service (“USPS”) delivers all of our U.S. mail correspondence, and we are bound to accept any postage rate increases enacted by the USPS. In the past, we have seen the specific postage rate applied to our products change due to a change in how the USPS interpreted its classification rules. In January 2013, the USPS determined that these reports should be charged first class postage rates rather than standard mail rates, thereby increasing our postage cost significantly. These increased charges continued through June 2013 when we were able to modify our product to comply with classification rules for postage at the standard rate. During the six months ended June 30, 2013, our payments to the USPS increased by $2.9 million as a result of these first class postage rates. We have encountered similar concerns from other carriers to a lesser extent as well. Such increased charges harmed our business and our results of operations during this period. If the USPS or other mail carriers change their position as to our mailed reports or we change our product offerings again, our future results of operations could be harmed.

If we cannot maintain our environmental focus as we grow, we could lose the innovation, teamwork, passion and focus on execution that we believe contributes to our success.

We believe that a critical contributor to our success has been our focus on the environmental impact of our products and solutions. We believe that focus has driven innovation, increased attention to results and has allowed us to attract and retain highly talented individuals who are motivated by our mission driven culture. As we grow and change, we may find it difficult to maintain this critical aspect of our corporate culture. Any failure to preserve our culture could harm our ability to retain and recruit quality personnel, thereby harming our future success.

We have a limited operating history in an evolving industry, which makes it difficult to predict our future prospects and may increase the risk that we will not be successful.

We have a limited operating history in an evolving market that may not develop as expected. This limited operating history makes it difficult to effectively assess or forecast our future prospects. We have encountered and will continue to encounter risks and uncertainties frequently experienced by growing companies in the technology industry, such as the risks and uncertainties described in this prospectus. If our assumptions regarding these risks and uncertainties are incorrect or change due to changes in our markets, or if we do not address these risks successfully, our financial results and results of operations may differ materially from our expectations and our business may suffer.

Our marketing efforts depend significantly on our ability to receive positive references from our existing utility customers.

We operate in an industry with a limited number of buyers and reputation is particularly important as a result. Our customers often serve as references for each other, and they have been known to discuss the performance of our products and solutions with each other. Consequently, our marketing efforts depend significantly on our ability to call on our current utility customers to provide positive references. Given our

19

limited number of utility customers, the loss or dissatisfaction of any customer could substantially harm our brand and reputation, inhibit the market acceptance of our products and solutions and impair our ability to attract new utility customers and maintain existing utility customers. Any of these consequences could harm our business, financial condition and results of operations.

Our business depends substantially on customers renewing, upgrading and expanding their solutions with us. Any decline in our customer renewals, upgrades and expansions may harm our future results of operations.

Our ability to grow depends substantially on our ability to expand our business with existing customers. To date, a significant portion of our growth has resulted from our ability to sell new products and solutions and expand existing products and solutions sold to current customers. We have limited historical data with respect to rates of customer renewals, upgrades and expansions so we may not accurately predict future trends in these areas. Our customers’ renewal rates may decline or fluctuate because of several factors, including their satisfaction or dissatisfaction with our solutions, the prices of our solutions, the prices of solutions offered by our competitors or reductions in our customers’ spending levels due to the macroeconomic environment or other factors. If our customers believe that our service offerings are not sufficiently scalable or effective and do not provide adequate security for the dissemination of information over the Internet, they will not expand their solutions with us, and our profitability and gross margin may be harmed. If our customers do not renew their subscriptions for our solutions, renew on less favorable terms or do not purchase additional functionality or subscriptions, our revenue may grow more slowly than expected or decline.

If the market for our cloud-based delivery model develops more slowly than we expect, our growth may slow or stall, and our results of operations would be harmed.