FORM 6-K

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Report of Foreign Issuer

Pursuant to Rule 13a-16 or 15d-16

of the Securities Exchange Act of 1934

For the month of February, 2022

Commission File Number: 001-12518

Banco Santander, S.A.

(Exact name of registrant as specified in its charter)

Ciudad Grupo Santander

28660 Boadilla del Monte (Madrid) Spain

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes ☐ No ☒

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes ☐ No ☒

Banco Santander, S.A.

TABLE OF CONTENTS

Pillar 3 - Disclosure Report

2021 - strengthening our capital strategy

| | | | | | | | | | | | | | | | | |

Introduction (Ch. 1) | | Capital (Ch. 2) |

| | | | | |

| Santander | | | Capital |

| Santander Pillar 3 Report overview | | | Capital function |

| Regulatory framework | | | Capital management and adequacy. Solvency ratios |

| Scope of consolidation | | | Pillar 1 - Regulatory Capital |

| | | | Pillar 2 - Economic Capital |

| | | | Capital planning and stress tests |

| | | | TLAC & MREL |

| | | | Lines of defence |

| | | | Corporate Special Situations and Resolution Framework |

| | | | | |

| | | | | |

Risks (Ch. 3, 4, 5, 6, 7, 8, 9 and 10) | | Santander (Ch. 11 and 12) |

| | | | |

| Global risk vision | | | Remuneration policies |

| Credit Risk | | | Appendices |

| Counterparty Credit Risk | | | | |

| Credit Risk - Securitisations | | Other appendices available on the Santander website. |

| Market Risk | |

| Operational Risk | | | Access 2021 Pillar 3 Disclosures Report available on the Santander Group website |

| ESG Risk | |

| Other Risks | |

| | | | | |

| | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Introduction |

|

| |

| 1.1. Santander | |

| 1.2. Santander Pillar 3 report overview | |

| 1.2.1. Background information on Santander | |

| 1.2.2. Governance: approval and publication | |

| 1.2.3. Transparency enhancements | |

| 1.2.4. Disclosure criteria used in this report | |

| 1.3. Regulatory framework | |

| 1.3.1. Prudential framework 2021: Capital Adequacy and Resolution key points | |

| 1.3.2. Regulatory response to impacts of covid-19 | |

| 1.3.3. Other regulations: Sustainability | |

| 1.3.4. Other regulations: Digital | |

| 1.3.5. Other regulations: AML/FT | |

| 1.4. Scope of consolidation | |

| 1.4.1. Differences between the consolidation method for accounting purposes and the consolidation method for regulatory capital calculation purposes | |

| 1.4.2. Substantial amendments due to a change in perimeter and corporate transactions | |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

1.Introduction

1.1. Santander

Everything we do must be Simple, Personal & Fair

Santander is one of the largest banks in the eurozone. As of December 2021, we had EUR 1,595,835 million in assets and EUR 1,153,656 million in total funds. Our market capitalization reached EUR 50,990 million.

Santander has a very clear aim to be the best open financial service platform, by acting responsibly and earning the lasting loyalty of our people, customers, shareholders and communities. Our purpose is to help people and businesses prosper.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| CUSTOMER FOCUS | | | | OUR SCALE | | | | DIVERSIFICATION |

Customers worldwide

153 mn +5 mn in 2021 | | | | Top 3 in 10 of our markets  1 1 | | | |

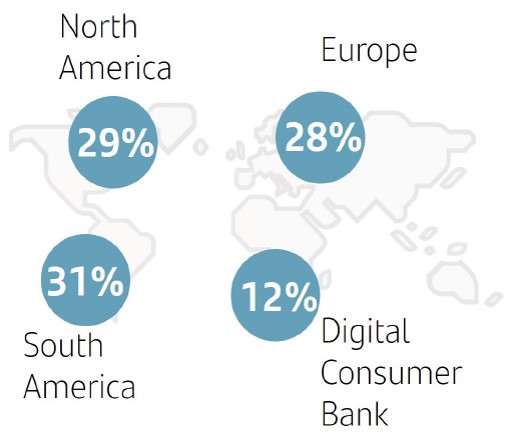

Geographic and business A |

A. 2021 underlying attributable profit by region. Operating areas excluding Corporate Centre.

We have laid the foundations to deliver great value and service for our customers, while increasing profits, improving profitability, and strengthening our capital base

| | | | | | | | | | | | | | | | | |

| Customer focus | | | | |

| | | | | |

| Deepening the relationships with our customers through a simpler value proposition, superior customer experience and our digital proposition | | → We have increased our number of customers over the last seven years, and notably in 2021, with balanced growth by region and business. → Our aim is to further enhance our customers' experience and satisfaction. → We also help a new generation of customers with new ways to interact with their finances, which is reflected in an increase digitalization (54% digital sales / total sales in 2021). |

|

|

| | | | | |

| Our scale | | | | |

| | | | | |

| Local scale and global reach | | → Regional and global scale based on three geographic regions, where we maintain a leadership position in our core markets. → Worldwide reach through our global businesses and PagoNxt, enabling greater collaboration across the Group to generate higher revenue and efficiencies. |

|

|

| | | | | |

| Diversification | | | | |

| | | | | |

| Our geographic and business diversification make us more resilient under adverse circumstances | | → We have a diversified geographical footprint which is well balanced between emerging and developed markets. → Business diversification between customers segments (individuals, SMEs, mid-market companies and large corporates). → This diversification remains a source of great strength and earnings stability. |

|

|

1 Market share in lending as of Sep-21 including only privately-owned banks. UK benchmark only covers the mortgage market (source: central banks). Digital Consumer Bank (DCB) refers to auto financing market shares in the majority of our Europe footprint (source: information from local auto associations and market intelligence reported by SCF units).

| | | | | | | | | | | |

9 | | 2021 Pillar 3 Disclosures Report | |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

Strong operating performance in 2021: EUR 8.7 bn of underlying profit

| | | | | | | | | | | | | | |

2021 (vs. 2020) |

GROWTH | | PROFITABILITY | | STRENGTH |

| Total customers | | RoTE B | | FL CET1 C |

153 mn (+5mn) | | 12.7% (+529bps) | | 12.0% (+7bps) |

Total revenue A | | Efficiency ratio | | Cost of credit D |

EUR 46.4 bn (+7%) | | 46.2% (-86bps) | | 0.8% (-51bps) |

| | | | |

2021 Shareholder value creation: +11%E |

A. Changes in constant euros. In euros: +4%.

B. Underlying RoTE. Statutory RoTE: 12%.

C. Including acquisition of SC USA minority interest which closed on 31 January 2022 and the announced acquisition of Amherst Pierpont which is subject to completion, regulatory approval and other conditions.

D. Provisions to cover losses due to impairment of loans in the last 12 months / average customer loans and advances of the last 12 months.

E. TNAV per share + cash DPS of EUR 7.6 cents paid in calendar year 2021.

We are creating value for our shareholders by focusing on delivering profitable growth in a responsible way

In 2021, we continued to deliver on our ESG commitments, supporting our customers´ green transition and financially empowering more people

| | | | | | | | | | | | | | |

Supporting the green transition | | Building a more inclusive society | | With a talented and diverse team |

| EUR 61 bn | | 7.5 mn | | 6 |

Green finance since 2019 A | | People financially empowered since 2019 | | Geographies where we are Top 10 company to work for |

| >200% | | >EUR 500 mn | | 26% |

YoY green finance in retail B | | Credit allocated to microfinance in 2021 | | Women in senior leadership positions |

| EUR 27 bn | | 1.4 mn | | ESG |

AuM in Sustainable funds C | | Microentrepreneurs supported since 2019 | | Metrics included in executives´incentives |

| #1 | | 8 | | #1 |

Financial advisor in Project Finance renewables D | | Countries with microfinance initiatives underway | | Bank in Bloomberg Gender Equality Index |

Note: non-audited data.

A. Only Santander Corporate Investment Bank (SCIB) global business.

B. All segments excluding SCIB and WM&I (Well Management and Investment).

C. AuMs classified as Article 8 and 9 funds (SFDR) from SAM, plus third-party funds and other ESG products according to EU taxonomy from Private Banking. We apply equivalent ESG criteria to SAM´s funds in Latin America.

D. Banco Santander, SA emerged as the top financial advisor for renewable energy project financing in 2021, with a total deal credit of USD 10.3 billion and a market share of 28%, according to Bloomberg NEF´s H2 2021 Clean Energy League Tables.

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

Santander operated in 2021 amid an environment characterised by:

| | | | | | | | | | | | | | |

| 1 | Fiscal and monetary policies implemented to counter the adverse effects of the covid-19 pandemic. |

|

|

| | | | |

| 2 | The ongoing recovery from the pandemic, which has been inconsistent across countries and sectors. |

|

|

| | | | |

| 3 | New covid-19 variants and significant outbreaks. |

|

|

| | | | |

| 4 | An upturn in inflation in the second half of the year, which reached a three-decade high in mature markets. |

|

|

Inflationary pressures have intensified as a result of a number of factors, including the renewed demand for consumer goods; labour shortages; tensions in the supply chains of microchips and other key items; transportation issues; and increases in energy, certain raw materials and food prices.

Under these circumstances, withdrawal of the expansionary fiscal and monetary policies implemented in response to the covid-19 pandemic began, especially in the last quarter of 2021, particularly in countries that experienced the heaviest pressure on prices.

| | |

| Capital management and solvency ratios |

Grupo Santander’s capital management aims to guarantee solvency and maximize profitability, while complying with internal objectives and regulatory requirements.

It is a key strategic tool for local and corporate decision making, enabling us to set a common framework of actions, criteria, policies, functions, metrics and processes.

Our active capital management applies strategies on efficient capital allocation to business lines, and considers securitizations, asset sales and issuances of capital instruments (capital hybrids and subordinated debt).

Our economic capital model aims to ensure our capital allocation is right for the risks inherent in our operations and risk appetite to optimize economic value added for our group and business units.

To optimize economic value added, we measure the real economic capital an activity requires and its return, and select those activities that maximize returns. We do this under both expected as well as unlikely but plausible economic scenarios, and with the solvency level decided by the Group.

| | | | | | | | | | | |

11 | | 2021 Pillar 3 Disclosures Report | |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

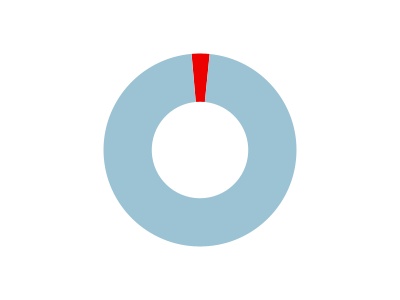

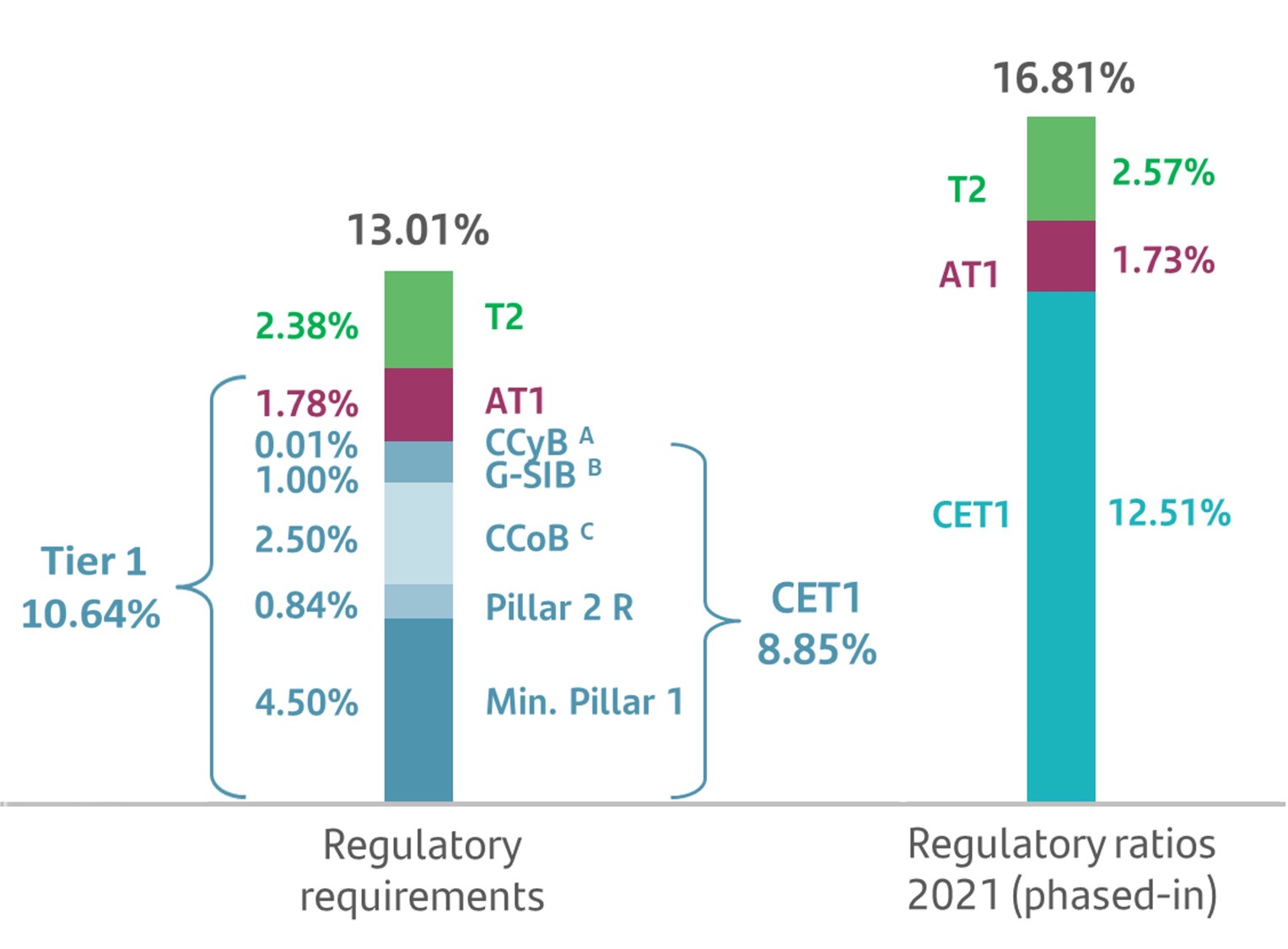

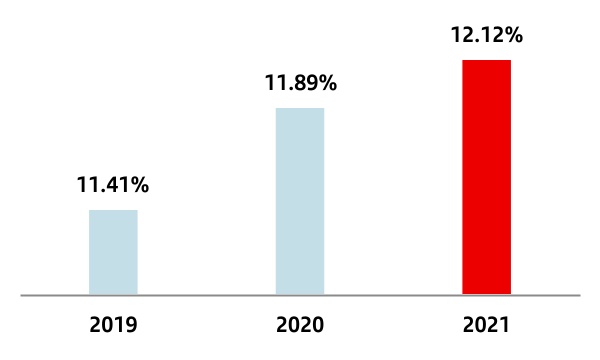

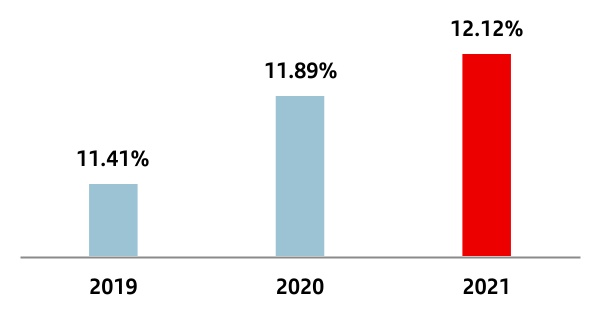

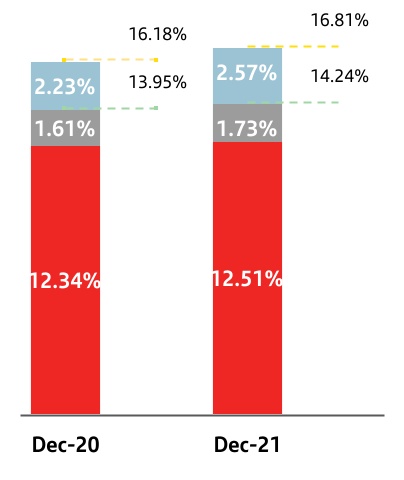

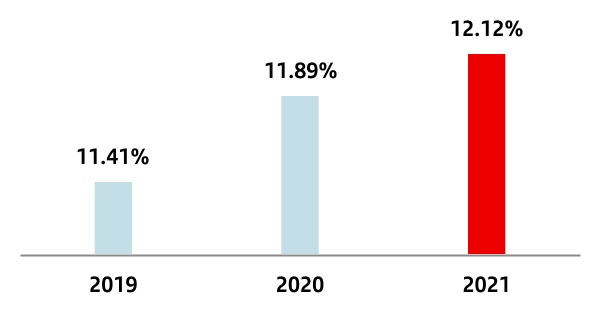

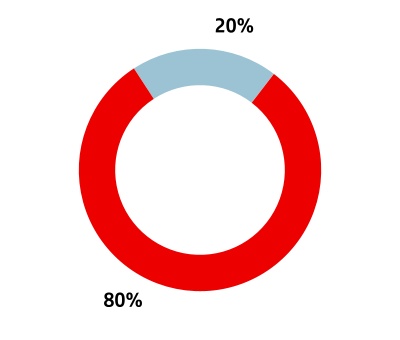

The fully-loaded CET1 ratio stood at 12.12%,

keeping our target between 11% and 12%

| | | | | | | | | | | | | | |

| Regulatory CET1 ratio (Phased-in)2 | |

| | | | |

| 11.65 | % | 12.34 | % | 12.51 | % | |

| | | | | | | | | | | | | | |

| Main capital figures and capital adequacy ratios. |

| EUR million |

| Fully-loaded | Phased-in2 |

| 2021 | 2020 | 2021 | 2020 |

| Common Equity (CET1) | 70,208 | 69,399 | 72,402 | 69,399 |

| Tier 1 | 79,939 | 75,510 | 82,452 | 78,501 |

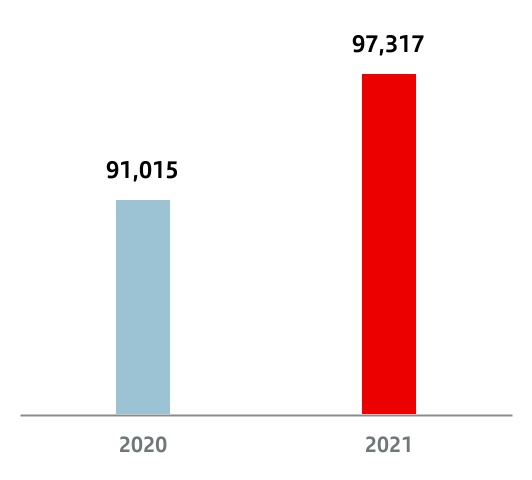

| Total capital | 95,078 | 88,368 | 97,317 | 91,015 |

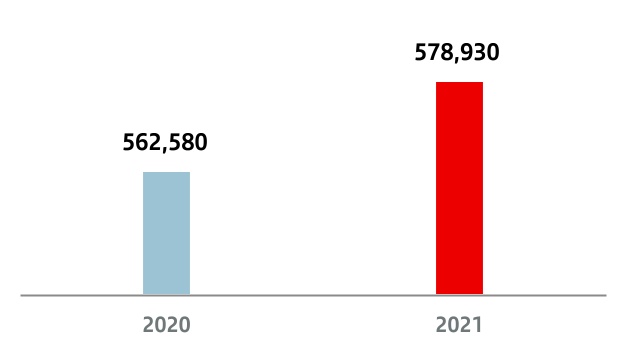

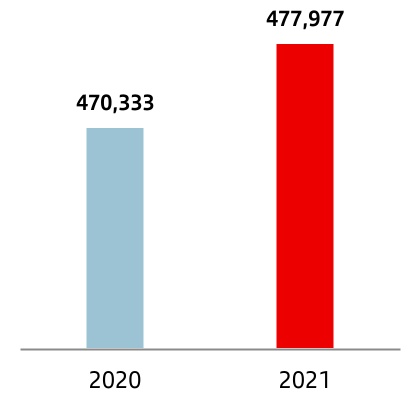

| Risk weighted assets | 579,478 | 561,850 | 578,930 | 562,580 |

| CET1 Ratio | 12.12 | % | 11.89 | % | 12.51 | % | 12.34 | % |

| Tier 1 Ratio | 13.79 | % | 13.44 | % | 14.24 | % | 13.95 | % |

| Total capital ratio | 16.41 | % | 15.73 | % | 16.81 | % | 16.18 | % |

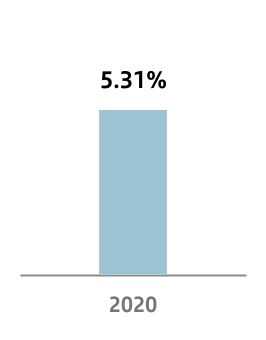

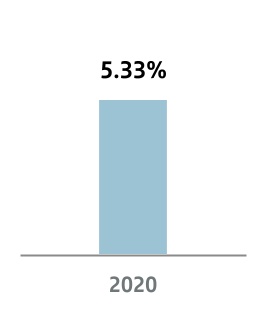

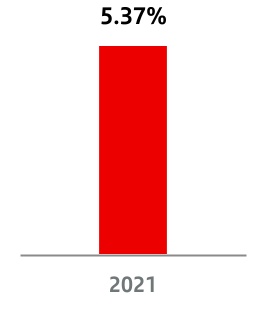

| Leverage Ratio | 5.21 | % | 5.31 | % | 5.37 | % | 5.33 | % |

Strong organic generation driven by profit and RWA management

in fully-loaded CET1 ratio

*Includes Accrued shareholders remuneration

If we do not apply the transitory IFRS 9 provisions, nor the subsequent amendments introduced by Regulation 2020/873 of the European Union, which has a 39 basis point impact, the fully-loaded CET1 ratio was 12.12%.

Of note in the year was organic generation of 118 basis points, supported by the results obtained in the year and management of risk-weighted assets. This figure includes a negative impact of 45 basis points related to shareholder remuneration. This strong generation was partially offset by regulatory and model impacts, the negative market impacts on available for sale (HTC&S) portfolios and non-recurring impacts (acquisition of minority interest in Mexico and restructuring costs).

If we include the acquisition of SC USA minority interests, which closed on 31 January 2022, and the announced acquisition of Amherst Pierpont, which is pending to completion, the CET1 ratio would be an estimated 16 basis points lower, bringing it to 11.96%.

The fully-loaded leverage ratio stood at 5.21%.

2 The phased-in ratios include the transitory treatment of IFRS 9, calculated in accordance with article 473 bis of the Regulation on Capital Requirements (CRR) and subsequent amendments introduced by Regulation 2020/873 of the European Union. Additionally, the Tier 1 and total phased-in capital ratios include the transitory treatment according to chapter 2, title 1, part 10 of the aforementioned CRR.

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

| | |

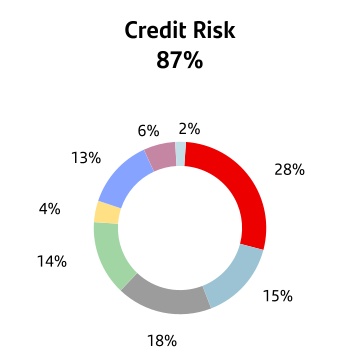

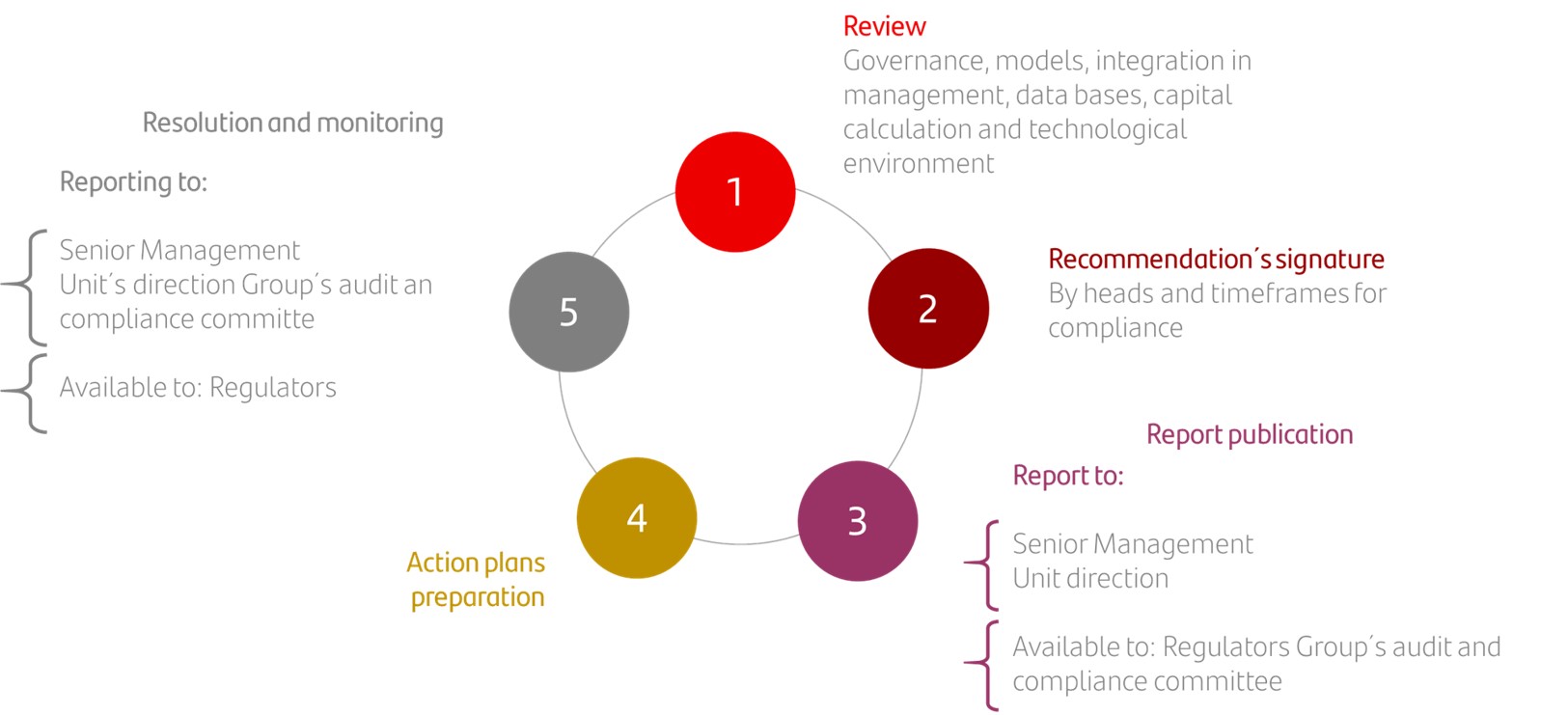

| Main risks capital requirements |

Solid risk culture, robust governance and advanced

risk management processes

| | | | | | | | | | | | | | |

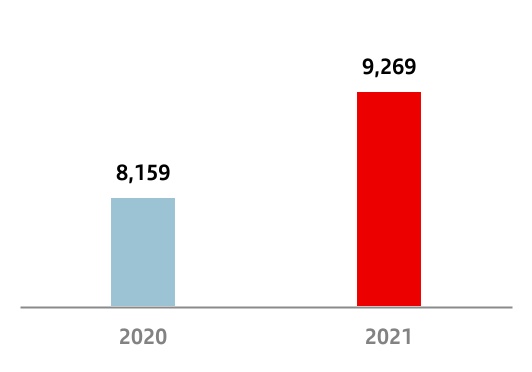

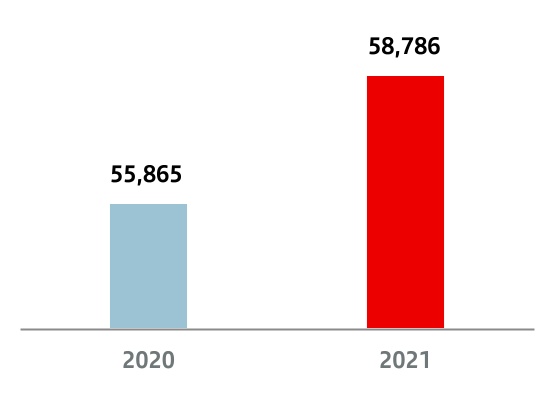

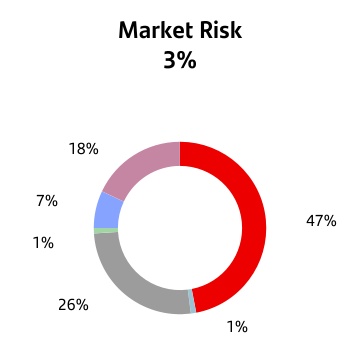

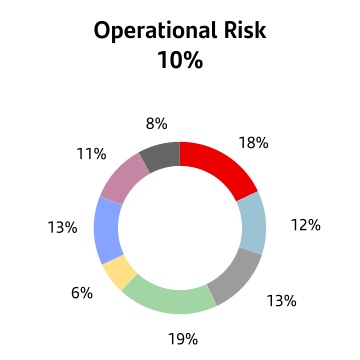

| Credit risk3 | | Market risk | | Operational risk |

| 40,233 | | 1,378 | | 4,703 |

Million euros | | Million euros | | Million euros |

The credit risk management process involves identification, assessment, control and decision-making in relation to the credit risk incurred in the group's operations. It incorporates operational, customer and portfolio factors, together with a comprehensive view of the credit risk cycle. The Business and Risk areas are involved in the process, along with senior management. Santander's profile is mainly retail, with an adequate diversification of credit risk between mature and emerging markets. The Group includes counterparty credit risk in its credit risk framework. Additionally, for management purposes, it also has a specific counterparty credit risk model, policy and procedures. | | The measurement, control and monitoring perimeter of the Market Risk area includes all transactions where risk arises due to changes in market factors. This risk arises from changes in risk factors (interest rate, exchange rate, equities, credit spreads, commodity prices and the volatility of each of these) which may impact earnings or capital, and from the liquidity risk of the products and markets in which Santander operates.

At the end of December 2021, Santander had authorisation to use the internal market risk model for calculating regulatory capital in the trading books of the Spain, Chile and Mexico units. From October 2021, the market risk capital of the internal model for Spain and Santander London Branch (SLB) will be reported in a single entity, following regulatory approval of the diversification between the two units. The Group aims to gradually extend this approval to the rest of the units with significant market positions. | | The Group controls and manages operational risk by focusing on identifying, assessing, mitigating and reporting sources of operational risk, whether or not they have materialised, ensuring that risk management priorities are properly established. Santander expressly recognises that while a certain volume of operational losses can be expected, severe unexpected losses resulting from failures in business controls are unacceptable.

The group applied new developments and enhancements to the operational risk management model in 2021 in the risk assessment and control tools, operational risk appetite, business continuity plans and the analysis and integration of new risks (such as transformation risk or climate risk) into the non-financial risk monitoring and control model. |

3 It includes counterparty credit risk and securitisations without 1250% deduction.

| | | | | | | | | | | |

13 | | 2021 Pillar 3 Disclosures Report | |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

1.2. Santander Pillar 3 report overview

1.2.1. Background information on Santander

Banco Santander, S.A. is a private-law entity subject to the rules and regulations applicable to banks operating in Spain. In addition to its direct operations, Banco Santander is the head of a group of subsidiaries engaged in a range of business activities that comprise Santander. The Capital Requirements Regulation (CRR) and its modifications (hereinafter referred to as CRR), Capital Requirements Directive (CRD) and its modifications, and its transposition through Banco de España Circular 2/2016, on supervision and capital adequacy, are applicable at a consolidated level to the whole of the Group.

Santander is one of the banks that have not required state aid in any of the countries in which they operate.

See Appendix II, CRR Mapping, for all aspects for which disclosure is required under Part Eight of the CRR, as amended but that are not applicable to Santander. These are reported as “N/A” (not applicable).

At 31 December 2021, none of the financial institutions consolidated in the Group had less than the minimum capital required under applicable regulations.

Under Article 7 and 9 of the CRR, the subsidiaries Santander Leasing S.A. EFC and Santander Factoring y Confirming S.A. EFC are exempt from the minimum capital requirements, the limit on large exposures and the internal corporate governance obligations at 31 December 2021. None of the exemptions under applicable regulations have been used for any other Santander subsidiaries.

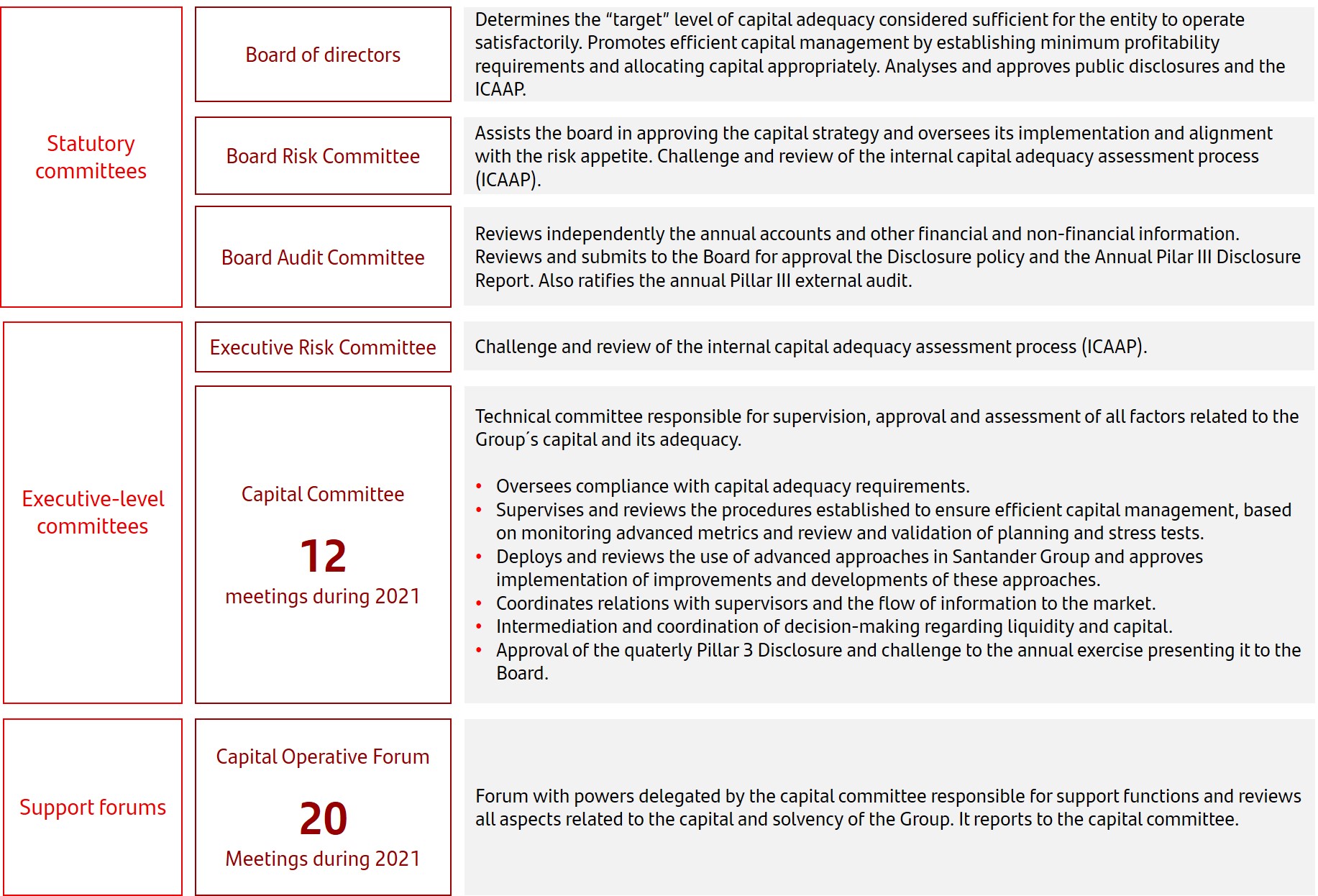

1.2.2. Governance: approval and publication

Santander Group has a formal policy on the disclosure of information of prudential relevance with the aim of defining the criteria for regulating the preparation process, minimum requirements to be included, frequency and associated governance in accordance with the provisions set forth in Directive 2013/36/EU, Regulation (EU) no. 2019/876 of 20 May 2019 (the EU Regulation or CRR2) amending Regulation (EU) no. 575/2013, as well as the law on supervision and capital requirements (10/2014) of the Bank of Spain.

This policy has been prepared in compliance with the criteria established in the European Banking Authority: Guidelines on Materiality, Proprietary, Confidentiality and Frequency of the Information in accordance with Article 432, sections 1 and 2 and Article 433 of Regulation (EU) 575/2013.

Pursuant to this policy, the Prudential Relevance Report corresponding to the financial year 2021 is published after its approval by the Board of Directors. Prior to its approval by the Board of Directors held on 24 February 2022, the report was reviewed by the Capital Committee held on 18 February 2022 and the Audit Committee during its session on the 21 February 2022.

Furthermore, since March 2015, a quarterly report is published which includes a set of information complying with the internal policy and criteria established in the European Banking Authority guidelines.

The information contained in this report has been subject to review by the External Auditor (PwC) which has not declared any incident in its report in relation to the reasonableness of the information detailed and the compliance with the information requirements established in the European Capital Directive and Regulation.

Certification by governing bodies

The board of directors of Santander certifies that the publication of the Pillar 3 disclosures report is compliant with the guidelines in Part Eight of Regulation (EU) 575/2013 and consistent with the “Pillar 3 Disclosures Policy” adopted by the board of directors.

No exceptions have been applied for the publication of information considered proprietary or confidential.

The Pillar 3 disclosures report relies on a range of processes relating to the internal control framework, with duties and responsibilities having been defined for review and certification of the information in the report at several levels of the organisation.

Further information on Santander´s internal control model (ICM) can be found in section VIII of the chapter on Corporate governance of the 2021 Annual report.

| | | | | |

| Access 2021 Annual Report available on the Santander Group website |

In addition, an ex-ante review is performed by external audit, the conclusions of which are presented to the audit committee and form part of the work plans of the recurring internal audit reviews.

The Pillar 3 disclosures report is available in the Shareholders and Investors section of the Santander website (www.santander.com), under "Financial and economic information".

| | | | | |

| Access 2021 Pillar 3 Disclosures Report available on the Santander Group website |

Disclosures by Santander subsidiaries

In addition to the information contained in this report, Santander subsidiaries that are considered to have significant

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

importance for their local market (under article 13 of the CRR, Application of disclosure requirements on a consolidated basis) publish information at the individual level on their websites, in relation to own funds, capital requirements, capital buffers, credit risk adjustments, remuneration policy and the application of credit risk mitigation techniques.

Santander subsidiaries in Argentina, Mexico, the United States, Santander Consumer Nordics, Santander Consumer Germany, Portugal, Chile, Poland, the United Kingdom and Uruguay publish their Pillar 3 reports in accordance with local regulations.

1.2.3. Transparency enhancements

The Group has noted the recommendation issued by international bodies with the aim of improving the transparency of the information published each year in the Pillar 3 disclosures report.

Santander takes into account all reporting requirements regarding market transparency published by the EBA, the BCBS and the Commission. Appendices I and II contain details on the various relevant documents.

Appendix I shows compliance with the different ITS in force in relation to disclosure, and Appendix II lists the location of the information disclosed in accordance with the relevant articles of Part Eight of the Regulation.

Some of the main transparency enhancements include the following:

Some of the main transparency enhancements include the following:

•In June 2021, phased to December 2021, the implementing technical standard (ITS) for the disclosure of Part VIII of Regulation No 575/2013 (CRR) came into force to standardise Pillar 3 disclosures. This disclosure increases our semi-annual disclosure by 30% and our annual disclosure by 10% and provides a uniform definition of the relationship between reporting and disclosure (mapping tool) for 60% of it.

•The implementing technical standard on the disclosure and reporting of the minimum requirement for own funds and eligible liabilities (MREL) and the total loss absorbing capacity (TLAC) also came into force in June 2021.

| | | | | |

| ¤ | For more information, see section 2.7. |

•As a result of the global health crisis, the EBA published a guide to the impact of covid-19 entitled "EBA GLs on reporting and disclosure of exposures subject to measures applied in response to the covid-19 crisis", which specifies that three quantitative templates with information on the scope of the moratoria must be published every six months. Given the ongoing covid-19 pandemic and the uncertainty over its future development, the EBA confirmed in January 2022 the continued application of this reporting and disclosure requirements until further notice.

| | | | | |

| ¤ | For more information, see section 4.10. |

•The EBA also published another ITS on Pillar 3 disclosure on interest rate risk arising from the non-trading book activities (IRRBB).

| | | | | |

| ¤ | For more information, see section 7.4.1. |

See Appendix I Transparency Enhancements and Appendix II CRR Mapping for further information on improvements in transparency.

| | | | | |

| ¤ | For more information, see Appendix I. |

| | | | | |

| ¤ | For more information, see Appendix II. |

In the Financial and economic information / Pillar 3 section of the Group's website, we also publish all the tables shown in this document in editable format for easier processing, as well as the appendices.

| | | | | |

| Access 2021 Pillar 3 Disclosures Report available on the Santander Group website |

Best practise aspiration

Grupo Santander strives to be a best practise example of disclosure, having already excelled in the last EBA assessments in the areas of liquidity, prudent valuation, improvements to general sections, presentation of information and other aspects of navigability.

1.2.4. Disclosure criteria used in this report

This report has been prepared in accordance with current European regulations on capital requirements (CRR).

The ratios presented in this report have been calculated using the transitional CRR and IFRS 9 implementation schedules.

Details of the types of information where there are differences between the regulatory information shown in this report and the information in the annual report and accounting information are as follows.

•The credit risk exposure measurements used for calculating regulatory capital requirements include:

◦Not only current exposures but also potential future risk exposures arising from future commitments (contingent liabilities and commitments) and changes in market risk factors (derivative instruments).

◦The mitigating factors for these exposures (netting agreements and collateral agreements for derivative exposures, and collateral and personal guarantees for on-balance-sheet exposures).

•The criteria used in classifying non-performing exposures in portfolios subject to advanced models for calculating regulatory capital are more conservative than those used

| | | | | | | | | | | |

15 | | 2021 Pillar 3 Disclosures Report | |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

for preparing the disaggregated information provided in the annual report.

1.3. Regulatory framework

1.3.1. Prudential framework 2021: Capital Adequacy and Resolution key points

Credit institutions must meet a number of minimum capital and liquidity requirements. These minimum requirements are governed by the European Capital Requirements Regulation, better known as CRR, and the Capital Requirements Directive, CRD. In June 2019, these regulations were significantly amended.

The applicable regulations are now CRRII and CRDV.

As the Directives need to be transposed into the legal systems of the different Member States in order to be applicable, in the case of Spain, Royal Legislative Decree 7/2021 and Royal Decree 970/2021 were published for this purpose in 2021.

In June 2019, CRRII introduced the minimum TLAC (Total Loss Absorbing Capacity) requirement, which only applies to global systemically important banks (G-SIBs). This requirement introduces two metrics: i) a minimum requirement for own funds and eligible liabilities as a percentage of the Total Risk Exposure Amount (TREA) set at 16% during the transition period and 18% from 1 January 2022 after the end of the transition period; and ii) a metric to set a minimum requirement for own funds and eligible liabilities in terms of a percentage of the Basel III tier 1 leverage ratio exposure measure of 6% during the transition period and 6.75% from 1 January 2022 after the end of the transition period.

This year saw the implementation of the EBA Guidelines on the New Definition of Default, which were prepared in accordance with CRR II, on 1 January 2021. The changes to CRRII that are applicable from June 2021 include the introduction of a minimum leverage ratio of 3%, the new standardised EAD calculation for counterparty risk, known as SA-CCR, the long-term liquidity ratio (NSFR), the new limits for large exposures and the requirement to report under the standardised approach for market risk.

CRDV introduces important modifications such as Pillar 2G regulation (guidance, Pillar 2 requirements orientation).

On 27 October 2021, the European Commission published the draft review of European banking legislation: CRR III and CRD VI.

This review completes the implementation of the Basel III reform, which was agreed at the end of 2017 and aims to reduce the variability of risk-weighted assets and improve comparability between banks.

The banking package consists of the following elements: 1) Implementation of the final Basel III reforms, 2) Contribution to sustainability and green transition and 3) Stronger supervision: ensuring sound management of EU banks and better protection of financial stability.

The first part is reflected in the Commission's proposal to amend the text of the CRR. This proposal contains changes concerning, among other things, key risk factors, standardised credit risk, internal models, the output floor and operational risk.

The second part, relating to the contribution to sustainability and green transition, is reflected in the fact that the legislative proposals continue to incorporate ESG (environmental, social and governance) factors into the various areas of prudential regulation: governance, supervision, risk management, reporting obligations to competent authorities and disclosure requirements, among other topics.

Finally, the third part, which refers to stronger supervision and protection of financial stability, is expressed in a series of provisions concerning: fit-and-proper requirements, the extension of the scope by revising certain definitions that would cover groups managed by fintechs, and the establishment of third-country branches in the EU in order to achieve greater harmonisation of rules and better supervision of this type of entity.

In general, the Commission proposes to start applying the new rules from 1.1.2025, but the amendments to the regulation that concern resolution issues could come into force in the first months of 2022.

With regard to the resolution rules, institutions must have an adequate funding structure to ensure that, in the event of financial distress, the institution has sufficient liabilities to absorb losses in order to recover its position or be resolved, while ensuring the protection of depositors and financial stability.

The directive that governs the resolution framework mentioned above is the Bank Recovery and Resolution Directive (BRRD). Like the CRR and the CRD, the BRRD was amended in June 2019, so BRRDII refers to all of these amendments. The transposition of this directive into the Spanish legal system took place in 2021 through a Royal Decree.

BRRDII has introduced important changes to the Minimum Requirement for Own Funds and Eligible Liabilities (MREL). For example, the TLAC requirement is now considered a Pillar 1 resolution requirement for G-SIBs. For large banks (defined as banks with total assets of more than €100 billion) or banks deemed systemically important by the resolution authority, BRRDII sets a minimum subordination requirement of 13.5% of risk-weighted assets or 5% of the leverage ratio, whichever is higher. For all other institutions, the subordination requirement is set by the resolution authority on a case-by-case basis.

Finally, Deposit Guarantee Schemes (DGS) are regulated by Directive 2014/49 or DSGD, which has not undergone any significant changes since its publication in 2014. It aims to harmonise the deposit guarantee schemes of the Member States, thus ensuring stability and balance in the different countries. It creates an appropriate framework for depositors to have better access to DGSs than was the case before the publication of this Directive through clear coverage, shorter repayment periods, better information and robust funding requirements. This Directive is transposed into Spanish law by Law 11/2015, Royal Decree 1012/2015 and Royal Decree 1041/2021.

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

1.3.2. Regulatory response to impacts of covid-19

The severe economic disruption caused by the covid-19 pandemic during 2020, which continued throughout 2021, has brought home the importance of the financing role banks will play in contributing to the recovery. Competent authorities (national, European and international) have acted by relaxing liquidity, capital and operational requirements so that banks could continue to provide funding to the economy, while ensuring they continue to act prudently.

As part of the European Central Bank's actions, several recommendations have been issued asking European banks to refrain from paying dividends and buying back shares to compensate shareholders.

The first recommendation to refrain from paying dividends was issued in March 2020 and was successively extended until 30 September 2021, when the ECB decided to lift it.

Throughout 2020, national governments took measures to counter the economic and social impact of the pandemic, particularly through legislative repayment moratoria to contain non-performing loans and help people cope with their liquidity needs. For its part, the European Banking Authority (EBA) has adopted a number of guidelines during 2020, including the guidelines on legislative and non-legislative moratoria implemented to respond to the covid-19 crisis on 2 April 2020. These guidelines clarify how the requirements of the public and private moratoria granted are to be met in order to avoid unjustified mass categorisation of these exposures as restructured or doubtful. While these guidelines were originally intended to apply to moratoria granted before 30 June 2020, the EBA decided on 2 December 2020 to reactivate the application of these guidelines for moratoria requested before 31 March 2021 and for a period not exceeding 9 months.

Another measure adopted in 2020 to provide flexibility in meeting the requirements was the approval and entry into force of the CRR "Quick Fix" amending CRR II (urgent and extraordinary amendments to bring about a more flexible regulatory framework in response to covid-19). The Quick Fix introduces a number of new features, including the extension of the transitional period granted before the pandemic for the entry into force of IFRS 9, due to the sudden and significant increase in expected credit loss provisions to be recognised. The implementation of certain provisions of CRR II has also been delayed, such as those relating to the leverage ratio buffer (postponed until 1 January 2023); the possibility of excluding exposures to central banks from the calculation of the leverage ratio, which should have been applied from June 2021 on, has been brought forward. Other provisions beneficial to institutions have also been brought forward. These include the support factors for SMEs and infrastructure, and the new treatment for software (applicable from the day following the publication date of the Delegated Regulation that implements it).

1.3.3. Other regulations: Sustainability

Since the publication of the European Commission's Action Plan underpinning the EU's 2030 climate and sustainable development goals and agenda, steady progress has been made in the development of sustainable finance.

2021 saw further implementation of the Taxonomy Regulation (2020/852), which sets harmonised criteria for classifying an economic activity as environmentally

sustainable. As part of its task to develop the six environmental objectives, the European Commission published the final selection criteria for identifying sustainable activities that contribute to the climate change mitigation and adaptation objectives, which were finally adopted in December 2021. The remaining four objectives – sustainability and protection of water and marine resources, transition to a circular economy, pollution prevention and control, and protection and restoration of biodiversity and ecosystems – will be further implemented during 2022. In addition, the Commission has begun to work on a possible extension of the taxonomy to also classify activities in transition that do not yet meet the criteria of the taxonomy, as well as those with harmful environmental impacts and those with social objectives. This work will continue in 2022.

The final version of the Delegated Act on Article 8 of the Taxonomy Regulation on disclosure requirements for financial and non-financial undertakings was published in July. It sets out a series of indicators that companies subject to the Non-Financial Reporting Directive (NFDR) must publish in relation to the taxonomy.

The most relevant indicator for banks is the Green Asset Ratio. The Green Asset Ratio is the percentage of its exposures that are consistent with the environmentally sustainable activities identified and specified in the relevant Delegated Regulations underlying the Taxonomy Regulation. The final text was adopted in December 2021.

The European Central Bank published its guide on supervisory expectations for climate and environmental risks in November 2020, which was integrated into the supervisory dialogue during the 2021 financial year. The European Central Bank also announced that it will conduct a climate stress test in the first half of 2022, the methodology for which was published at the end of October this year.

Finally, in July, the EBA published its report on the management and monitoring of ESG risks for banks and investment firms. This report will form the basis for the development of guidelines for the ESG risk management of institutions and the supervision of ESG risks by competent authorities in the EU. The EBA guidelines are expected to be published in June 2022.

In 2022, the EBA is expected to publish the technical implementation details for the integration of ESG risks in the Pillar 3 report. Institutions must implement these developments from 2023, for the 2022 financial year.

1.3.4. Other regulations: Digital

Due to the digitalisation of the financial industry and the resulting transformation of the sector, regulators and supervisors need to update both the regulatory framework and their approach to reflect the new realities and business models that are emerging as a result of this new digital world.

In their efforts to maintain financial stability, financial regulators and Supervisors proceed in three main ways:

•by adapting or creating new rules that take into account new realities and new uses of already identified technologies or new relationships that emerge between participants in the financial system and technology companies;

| | | | | | | | | | | |

17 | | 2021 Pillar 3 Disclosures Report | |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

•by broadening the scope of the already existing regulatory framework to ensure regulation that applies consistently to all those engaged in the same activity (in line with the principle of "same activity, same risks, same rules");

•and finally, by adapting the supervisory approach to the new risks that emerge in a constantly evolving digital environment.

In 2021, there have been other regulatory initiatives at both international and European levels that address new realities or the use of technology in the financial industry. These include in particular in Europe (currently under discussion):

•The proposed Digital Operational Resilience Act (DORA), which aims to manage the risks generated by IT-related service providers in their interactions with financial sector participants. An important part of this proposal is that providers deemed to be critical will be subject to direct supervision by banking supervisors.

•The proposed Digital Markets Act (DMA) regulation aims to regulate competition in digital markets and proposes to impose certain "ex ante" obligations on those digital platforms that can be considered "gatekeepers".

•The proposal for a European regulation on Artificial Intelligence, which regulates the use of this technology for both public and private entities. The proposal focuses on applications that are considered high-risk, including the customers' creditworthiness assessment and human resources management.

•The proposed Regulation on Markets in Crypto-Assets (MiCA), which regulates and establishes a regulatory framework for service providers (e.g. issuers, exchanges, wallets, etc.) of crypto-assets, which are not considered financial instruments. Among other things, the proposal regulates crypto-assets used for payments and establishes a stricter framework for crypto-assets that are "significant" in terms of their degree of proliferation.

•The proposed revision of the EIDAs (Regulation on Electronic Identification, Authentication and Trust Services), which proposes a new framework for a European digital identity available to citizens and businesses through digital wallets. The new framework will enable the electronic exchange of documents and proof of identity across Europe, as well as access to public services, applications requiring a high level of security, such as banking services, and digital platforms.

In the area of payment services, the authorities are focusing on further development so that the benefits of innovation and the opportunities created by digitalisation can be exploited. The aim is to create a payment system that is more accessible, faster, offers cross-border solutions and preserves consumer protection at all times.

There is still a debate on whether and under what conditions it makes sense to issue a Digital Euro (there has been a lot of discussion about possible design options this year). The same sorts of debates are also taking place in many other jurisdictions across the world.

1.3.5. Other regulations: Anti-money laundering and countering the financing of terrorism (AML/FT)

In July 2021, the European Commission published a proposal for an Anti-Money Laundering and Countering the Financing of Terrorism (AML/FT) regulatory package that aims to strengthen existing EU rules, improve the detection of suspicious transactions and activities, and close loopholes in the current regulatory framework. It consists of four legislative proposals:

1.Regulation establishing a new European AML/FT Authority that will coordinate national AML/FT authorities and directly supervise certain financial sector institutions. The Authority is expected to become operational in 2024 and to start its supervisory activities in 2026.

2.AML/FT Regulation. Parts of the current Directive will be transferred to this Regulation, which will be directly applicable in all Member States without the need for local transposition. This will harmonise EU requirements in areas such as customer due diligence, among others. Expected to be implemented by the end of 2025.

3.Sixth AML/FT Directive, which will repeal the current Directive. It contains provisions that must be transposed into national law, in particular on national supervisory authorities and Financial Intelligence Units (FIUs).

4.Recast of the Regulation on Transfers of Funds, with a particular focus on the tracking of transfers of crypto-assets. This revision introduces new requirements in relation to Virtual Asset Service Providers (VASPs) by requiring these actors to collect and make available data on the originators and beneficiaries of the transfers of virtual or crypto assets they operate.

The European Parliament and the Council are now debating this package, and the legislative procedure is estimated to take about two years.

1.4. Scope of consolidation

This section covers the qualitative requirements LIA - Explanations of differences between accounting and regulatory exposure amounts and LIB - Other qualitative information on the scope of application.

The Group companies included in the scope of consolidation for calculating the capital adequacy ratio under the CRR are the same as those included in the scope of consolidation for accounting purposes under Banco de España Circular 2/2018.

1.4.1. Differences between the accounting consolidation method and the consolidation method for calculating regulatory capital

In application of Part I (General Provisions) of the CRR, some Santander companies are consolidated using a different methods for accounting consolidation.

For the purposes of calculating the capital adequacy ratio based on the nature of their business activities, the Group companies included in the prudential scope of consolidation are consolidated using the full consolidation method, with the exception of jointly controlled entities, which use proportionate consolidation. All companies that cannot be

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

consolidated based on their business activities are accounted for using the equity method and so are treated as equity exposures.

The basis of the information used for accounting purposes differs from that used for calculating regulatory capital requirements. Risk exposure measurements may differ depending on the purpose for which they are calculated, such as financial reporting, regulatory capital reporting and management information. The exposure data included in the quantitative disclosures in this document are used for calculating regulatory capital or leverage ratio.

The companies for which different consolidation methods are used, depending on the regulations applied (table LI3), are listed in Appendix V of the 2021 Pillar 3 Report file available on the Santander website.

| | | | | |

| Access 2021 Pillar 3 Disclosures Report available on the Santander Group website |

| | | | | | | | | | | |

19 | | 2021 Pillar 3 Disclosures Report | |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

The following table shows the relationship between the categories in the financial statements and the risk categories in accordance with prudential requirements.

| | | | | | | | | | | | | | | | | | | | | | | |

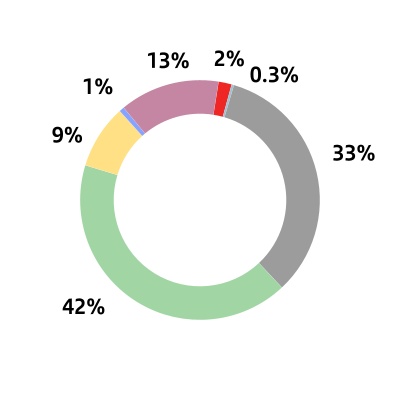

| Table 1.LI1 - Differences between accounting and regulatory scopes of consolidation and mapping of financial statement categories with regulatory risk categories |

|

| EUR million | | | | | | | |

| | | | | | 2021 |

| Carrying values as reported in published financial statements | Carrying values under scope of regulatory consolidation | Carrying values of items: |

| Subject to credit risk framework | Subject to the CCR framework | Subject to securitisation framework | Subject to market risk framework | Not subject to capital requirements or subject to deduction from capital |

| Assets | | | | | | | |

| Cash and cash balances at central banks | 210,689 | 211,095 | 211,095 | — | — | — | — |

| Financial assets held for trading | 116,953 | 116,923 | — | 71,264 | 73 | 116,850 | — |

| Non-trading financial assets mandatorily measured at fair value through profit or loss | 5,536 | 3,483 | 752 | — | 760 | 1,971 | — |

| Financial assets not held for trading valued mandatorily at fair value through profit or loss | 15,957 | 13,790 | — | 5,489 | — | 13,790 | — |

| Financial assets designated at fair value through profit or loss | 108,038 | 95,246 | 80,803 | — | 14,443 | — | — |

| Financial assets at amortised cost | 1,037,898 | 1,042,227 | 1,005,832 | 32,637 | 3,677 | — | 82 |

| Derivatives - Hedge accounting | 4,761 | 4,770 | — | 4,770 | — | — | — |

| Fair value changes of the hedged items in portfolio hedge of interest rate risk | 410 | 410 | — | — | — | — | 410 |

| Investments in subsidiaries, joint ventures and associates | 7,525 | 8,492 | — | — | — | — | 8,492 |

| Reinsurance assets | 283 | — | — | — | — | — | — |

| Tangible assets | 33,321 | 31,073 | 31,073 | — | — | — | — |

| Intangible assets | 16,584 | 16,819 | 1,766 | — | — | — | 15,052 |

| Tax assets | 25,196 | 25,210 | 23,954 | — | — | — | 1,256 |

| Other assets | 8,597 | 8,842 | 6,870 | — | — | — | 1,972 |

| Non-current assets and disposal groups classified as held for sale | 4,089 | 4,305 | 4,305 | — | — | — | — |

| Total assets | 1,595,837 | 1,582,685 | 1,366,450 | 114,161 | 18,953 | 132,610 | 27,264 |

| Liabilities | | | | | | | |

| Financial liabilities held for trading | (79,469) | (79,508) | — | (67,272) | — | (79,508) | — |

| Financial liabilities designated at fair value through profit or loss | (32,733) | (15,305) | — | (390) | — | (15,305) | — |

| Financial liabilities measured at amortised cost | (1,349,169) | (1,354,296) | — | — | — | — | (1,354,296) |

| Derivatives - Hedge accounting | (5,463) | (5,457) | — | (5,457) | — | — | — |

| Fair value changes of the hedged items in portfolio hedge of interest rate risk | (248) | (248) | — | — | — | — | — |

| Liabilities under insurance contracts | (770) | — | — | — | — | — | — |

| Provisions | (9,583) | (9,595) | (733) | — | — | — | (8,862) |

| Tax liabilities | (8,649) | (8,576) | — | — | — | — | (8,576) |

| Other liabilities | (12,700) | (12,669) | — | — | — | — | (12,669) |

| Total liabilities | (1,498,784) | (1,485,654) | (733) | (73,119) | — | (94,813) | (1,384,403) |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

The difference in total assets between the public and the reserved scopes is not material and corresponds to the exclusion of financial institutions and the inclusion of jointly controlled and intra group entities.

In addition, the sum of the carrying amounts of certain items is greater than the carrying amounts under the scope of prudential consolidation, as the financial assets held for trading and the financial assets at fair value through profit or loss are subject to the capital requirements of more than one risk category under the regulatory scope.

The main differences between the carrying amounts in the financial statements and the exposures for prudential purposes are shown below:

| | | | | | | | | | | | | | | | | |

| Table 2.LI2 - Main sources of differences between regulatory exposure amounts and carrying values in financial statements |

|

| EUR million | | | | | |

| | | | 2021 |

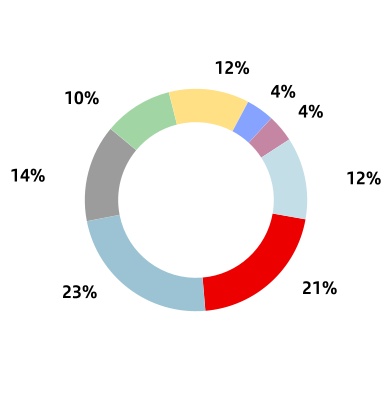

| Total | Items subject to: |

| Credit risk framework | CCR framework | Securitisation framework | Market risk framework |

| Asset carrying value amount under scope of regulatory consolidation (as per template EU LI1) | 1,632,174 | 1,366,450 | 114,161 | 18,953 | 132,610 |

| Liabilities carrying value amount under regulatory scope of consolidation (as per template EU LI1) | (168,665) | (733) | (73,119) | — | (94,813) |

| Total net amount under regulatory scope of consolidation | 1,463,509 | 1,365,717 | 41,042 | 18,953 | 37,797 |

| Off-balance sheet amounts | 331,030 | 331,030 | — | — | — |

| Regulatory Add-on | 31,975 | — | 31,975 | — | — |

| Differences in valuations | — | — | — | — | — |

| Differences due to different netting rules, other than those already included in row 2 | (42,626) | — | (4,828) | — | (37,797) |

| Non-eligibility of the balances corresponding to accounting hedges (derivatives) | (4,770) | — | (4,770) | — | — |

| Securitisations with risk transfer | 28,321 | 32,874 | — | (4,553) | — |

| Other | (17,006) | (50,745) | — | 33,739 | — |

| Differences due to consideration of provisions | (14,601) | (14,389) | — | (212) | — |

| Differences due to CRMs | (32,629) | (16,442) | (15,592) | (595) | — |

| Differences due to CCFs | (235,233) | (235,233) | — | — | — |

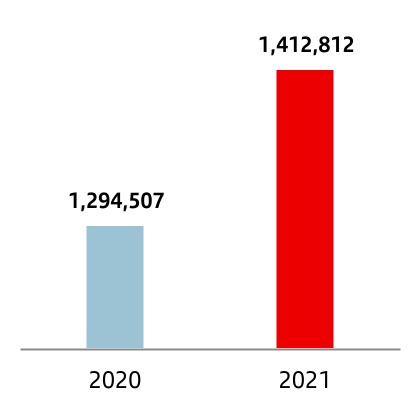

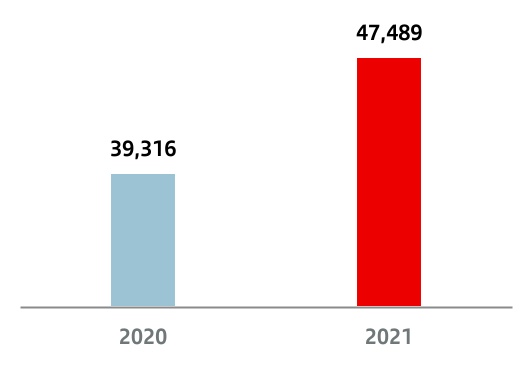

| Exposure amounts considered for regulatory purposes (EAD) | 1,508,128 | 1,412,812 | 47,827 | 47,489 | — |

This table shows a breakdown of the differences between the amounts of exposures for prudential purposes and the carrying amounts according to various parameters

The main causes in this case, result from the amount of off-balance sheet items +EUR 331.030 billion) and the application of CCFs (-EUR 235.233 billion). The regulatory add-on (+EUR 31.975 billion and the differences resulting from the various offsetting rules (-EUR 42.626 billion).

The reconciliation of the public and non-public balance sheets (table CC2) is shown in Appendix VI, which is available on the Santander website.

| | | | | |

| Access 2021 Pillar 3 Disclosures Report available on the Santander Group website |

1.4.2. Substantial amendments due to a change in the perimeter and corporate transactions

For more information on the main acquisitions and disposals of holdings in other companies and other major corporate transactions by Santander last year, refer to section 3 of the Notes to the consolidated financial statements in the Audit Report section of the 2021 Annual Report.

| | | | | |

| Access 2021 Annual Report available on the Santander Group website |

| | | | | | | | | | | |

21 | | 2021 Pillar 3 Disclosures Report | |

| | |

INTRODUCTION 2021 Pillar 3 Disclosures Report |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | |

| Capital |

|

|

| |

| 2.1. Capital | |

| 2.2. Capital function | |

| 2.2.1. Organisation | |

| 2.2.2. Capital governance | |

| 2.3. Capital management and adequacy. Solvency ratios | |

| 2.3.1. Profitability | |

| 2.3.2. Pricing | |

| 2.3.3. Other activities in capital management | |

| 2.4. Pillar 1 - Regulatory capital | |

| 2.4.1. Eligible capital | |

| 2.4.2. Capital requirements | |

| 2.4.2.1. Plan to deploy advanced internal models and supervisory approval | |

| 2.4.3. Capital buffers and capital requirements | |

| 2.4.4. Leverage ratio | |

| 2.5. Economic capital and RoRAC - Pillar II | |

| 2.6. Capital planning and stress tests | |

| 2.7. Total Loss-Absorbing Capacity (TLAC) and Minimum Requirement for own funds and Eligible Liabilities (MREL) | |

| 2.8. Lines of defence | |

| 2.8.1. Second line of defense | |

| 2.8.2. Internal Audit | |

| 2.9. Corporate Special Situations and Resolution Framework, crisis management, Recovery and Resolution Planningk | |

| |

| |

| |

| | |

CAPITAL 2021 Pillar 3 Disclosures Report |

2. Capital

| | | | | | | | | | | | | | |

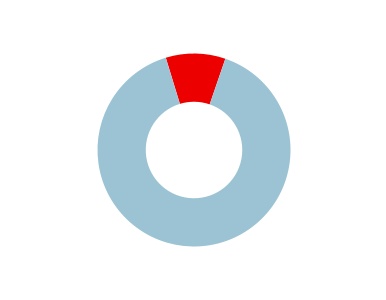

| Regulatory CET1 ratio (Phased-in)4 | |

| | | | |

| 11.65 | % | 12.34 | % | 12.51 | % | |

Focus ahead will remain on disciplined capital allocation and shareholder

remuneration while we maintain our fully-loaded CET1 target

between 11% and 12%.

At December 31, 2021, the fully-loaded CET1 ratio (without applying the IFRS 9 or CRR transitional arrangements) stood at 12.12% and the phased-in CET1 ratio was 12.51%. Only applying the IFRS 9 transitional arrangements (CRR fully-loaded), the ratio remains at 12.51%. The following table shows shows the impact of the CRR transitional arrangements under a IFRS 9 phased-in scenario:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Table 3.Main capital figures and capital adequacy ratios (Phased-in IFRS 9). | | |

| EUR million | | |

| Fully-loaded CRR | | Phased-in CRR |

| Dec'21 | Sep'21 | Jun'21 | Mar'21 | Dec'20 | | Dec'21 | Sep'21 | Jun'21 | Mar'21 | Dec'20 |

| Common Equity (CET1) | 72,402 | 70,787 | 70,864 | 69,627 | 69,399 | | 72,402 | 70,787 | 70,864 | 69,627 | 69,399 |

| Tier 1 | 82,133 | 80,585 | 79,661 | 78,417 | 78,126 | | 82,452 | 80,897 | 79,973 | 78,731 | 78,501 |

| Total capital | 97,013 | 93,240 | 92,270 | 91,466 | 90,933 | | 97,317 | 93,537 | 92,539 | 91,550 | 91,015 |

| Risk weighted assets | 578,930 | 577,209 | 584,999 | 567,797 | 562,580 | | 578,930 | 577,209 | 584,999 | 567,797 | 562,580 |

| CET1 Ratio | 12.51 | % | 12.26 | % | 12.11 | % | 12.26 | % | 12.34 | % | | 12.51 | % | 12.26 | % | 12.11 | % | 12.26 | % | 12.34 | % |

| Tier 1 Ratio | 14.19 | % | 13.96 | % | 13.62 | % | 13.81 | % | 13.89 | % | | 14.24 | % | 14.02 | % | 13.67 | % | 13.87 | % | 13.95 | % |

| Total capital ratio | 16.76 | % | 16.15 | % | 15.77 | % | 16.11 | % | 16.16 | % | | 16.81 | % | 16.20 | % | 15.82 | % | 16.12 | % | 16.18 | % |

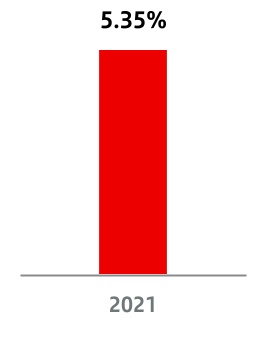

| Leverage Ratio | 5.35 | % | 5.29 | % | 5.25 | % | 5.06 | % | 5.31 | % | | 5.37 | % | 5.31 | % | 5.27 | % | 5.08 | % | 5.33 | % |

| | | | | | | | | | | |

| 2020 and 2021 figures are calculated applying the transitional arrangements of IFRS 9 unless specified otherwise (Phased-in IFRS 9). | | |

| In March and June 2021 a pay-out of 50% was applied, from September onwards 20% cash was applied depending on the dividend in cash and the first authorized repurchase. | | |

2.1. Capital

Capital management and control at the Group is a fully transversal process that seeks to guarantee the bank's capital adequacy, while complying with regulatory requirements and maximising profitability.

It is determined by the strategic objectives and risk appetite set by the board of directors. To achieve this, the following

policies have been established that shape the approach that the Group applies to capital management:

•Establish adequate capital planning, so as to meet current needs and provide the necessary resources to meet the needs of the business plans, regulatory requirements and the associated risks in the short and medium term, while maintaining the risk profile approved by the board.

4 The phased-in ratios include the transitory treatment of IFRS 9, calculated in accordance with article 473 bis of the Regulation on Capital Requirements (CRR) and subsequent amendments introduced by Regulation 2020/873 of the European Union. Additionally, the Tier 1 and total phased-in capital ratios include the transitory treatment according to chapter 2, title 1, part 10 of the aforementioned CRR.

| | | | | | | | | | | |

25 | | 2021 Pillar 3 Disclosures Report | |

| | |

CAPITAL 2021 Pillar 3 Disclosures Report |

•Ensure that Santander and its companies have adequate capital to cover needs resulting from increased risks due to deteriorating macroeconomic conditions under stress scenarios.

•Optimise capital use through its appropriate allocation among the businesses, based on the relative return on regulatory and economic capital and taking risk appetite, growth and strategic objectives into account.

Santander maintains a very comfortable capital adequacy position, well above the levels required by applicable regulations and by the European Central Bank.

IFRS 9 became effective on 1 January 2018, implying changes in accounting that affect capital ratios. Santander decided to apply the transitional arrangements, which means a seven-year transitional period.

Had the IFRS9 or CRR transitional arrangements not been applied, the total impact on the fully-loaded CET1 ratio at December would have been -39bps.

Phased-in CET1 stood at 12.51% in December, increasing by 17 bps during the year.

For further detail see the comparison of institutions’ own funds and capital and leverage ratios with and without the application of transitional arrangements for IFRS 9 or analogous ECLs (IFRS 9-FL), Appendix VIII (NIIF9).

| | | | | |

| Access 2021 Pillar 3 Disclosures Report available on the Santander Group website |

For further information on capital key metrics see Appendix VII (KM1 requirement).

| | | | | |

| Access 2021 Pillar 3 Disclosures Report available on the Santander Group website |

| | | | | | | | |

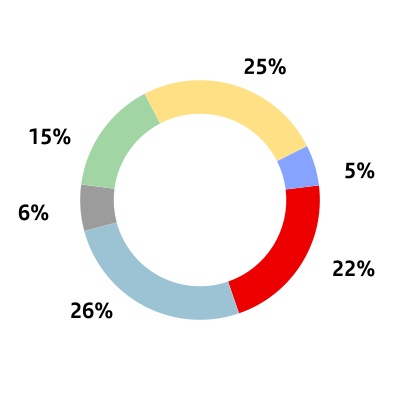

| Changes in main Capital ratios (Phased-in IFRS9) | |

| |

| | | | | |

|

| n | T2 |

| n | AT1 |

| n | CET1 |

| n | Tier 1 |

| n | Total capital ratio |

| |

| |

| |

| |

| | |

| 2021 CET1 evolution (Phased-in IFRS9) |

% |

*Includes Accrued shareholders remuneration

| | | | | | | | | | | |

26 | | 2021 Pillar 3 Disclosures Report | |

| | |

CAPITAL 2021 Pillar 3 Disclosures Report |

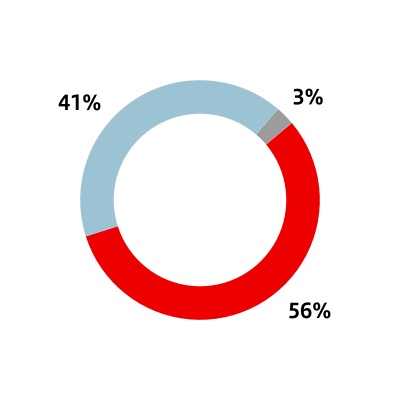

There was 120 basis points of organic capital growth in the year (including the negative impact from shareholder remuneration), supported by the results obtained in the year and the management of risk weighted assets. This figure includes a negative impact of 45 basis points related to shareholder remuneration. This strong generation was partially offset by regulatory and model impacts, the negative market impacts on available for sale portfolios and non-recurring impacts (acquisition of minority interest in Mexico and restructuring costs).

If we include the acquisition of SC USA minority interests, which closed on 31 January 2022, and the announced acquisition of Amherst Pierpont, which is pending to completion, the CET1 ratio would be 12.35% (instead of 12.51%).

The phased-in leverage ratio was 5.37%.

| | | | | |

| ¤ | For more information, see section 2.4.3. |

2.2. Capital function

The core principles establish the basic guidelines governing the actions of Santander entities in capital management, monitoring and control processes.

2.2.1. Organisation

The organisational structure has been defined with the aim of guaranteeing compliance with the core principles in relation to capital and ensuring that the relationship between the subsidiaries and the corporate centre is maintained. This function allows twin objectives to be met: comply with the subsidiary’s financial autonomy while at the same time retaining coordinated monitoring at group level.

2.2.2. Capital governance

Santander has developed a structure of agile and efficient governing bodies, ensuring the Capital function operates properly when it comes to both decision-making and supervision and control. This ensures the involvement of all the areas concerned and the necessary involvement of senior management.

The Group's characteristic subsidiary-based structure has a strong capital governance where there are various committees that have responsibilities at regional level and also for coordination at group level. The local committees must report to the corporate committees in due time and proper form on any relevant aspects of their activity that may affect capital, to ensure proper coordination between the subsidiaries and the corporate centre.

| | | | | | | | | | | |

27 | | 2021 Pillar 3 Disclosures Report | |

| | |

CAPITAL 2021 Pillar 3 Disclosures Report |

2.2.3. Capital targets

Focus ahead will remain on disciplined capital allocation and shareholder remuneration while we maintain our fully-loaded CET1 target between 11%-12%.

| | | | | | | | | | | | | | |

| Regulatory CET1 ratio (Phased-in) | |

| | | | |

| 11.65 | % | 12.34 | % | 12.51 | % | |

The continuous improvement in the capital ratios reflects our profitable growth strategy and a culture of active capital management at all levels of the organization.

In order to have a more global vision and simplify our structure, we created a new team, ‘Capital and Profitability Management’, in charge of our capital analysis, adequacy and management, coordination with subsidiaries in all matters related to capital and monitoring and measuring returns.

All the countries and business units have drawn up individual capital plans focused on achieving a business that maximizes the return on equity.

Santander gives a significant weight to capital and incentives. Certain aspects relating to capital management and returns are taken into account when setting the variable remuneration payable to members of senior management:

•The relevant metrics include our CET1 ratio, the county units' capital contributions to the Group ratio, the return on tangible equity (RoTE) and profit after tax.

•The qualitative aspects considered include the proper management of regulatory changes affecting capital, effective management of capital relating to business decisions, sustainable capital generation over time and effective capital allocation.

Action plans

In addition, we have developed a three-year action plan for the continuous improvement of infrastructures, processes and methodologies that support all aspects related to capital,

with the aim of further enhancing active capital management, responding more quickly to the numerous and increasing regulatory requirements and efficiently carrying out all associated activities.

We continue to improve our processes and controls associated with capital data quality. Additionally, we continuously develop risk management initiatives at both the consolidated and local levels to strengthen and fine-tune different activities.

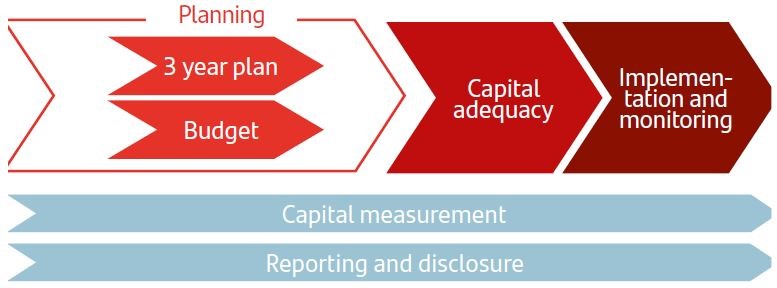

2.3. Capital management and adequacy. Solvency ratios

The aim of capital management and adequacy at the Group is to guarantee solvency and maximise its profitability, while complying with internal capital targets and regulatory requirements.

Capital management is a key strategic tool for decision-making at both the local and corporate levels.

At the Group there is a common framework of action, criteria, policies, functions, metrics and processes for capital management.

The Group's most notable capital management activities are:

•Establishing capital adequacy and capital contribution targets aligned with minimum regulatory requirements and internal policies, to guarantee robust capital levels consistent with our risk profile and efficient use of capital to maximise shareholder value.

•Developing a capital plan to meet those objectives consistently with the strategic plan. Capital planning is an essential part of executing the three-year strategic plan.

•Assessing capital adequacy to ensure that the capital plan is also consistent with our risk profile and risk appetite framework in stress scenarios.

•Developing the annual capital budget as part of the group's budgeting process.

•Monitoring and controlling the group's and countries' budget execution and drawing up action plans to correct any deviations from the budget.

•Integrating capital metrics into business management to ensure consistency with group objectives.

•Preparing internal capital reports, and reports for the supervisory authorities and the market.

•Planning and managing other loss absorbing instruments (MREL and TLAC).

The Group's capital function is carried out on three levels:

| | | | | | | | | | | |

28 | | 2021 Pillar 3 Disclosures Report | |

| | |

CAPITAL 2021 Pillar 3 Disclosures Report |

| | | | | | | | | | | | | | |

| → | Regulatory capital |

| The first step in managing regulatory capital is to analyse the capital base, the capital adequacy ratios under the current regulatory criteria and the scenarios used in capital planning in order to make the capital structure as efficient as possible, both in terms of cost and compliance with regulatory requirements. Active capital management includes strategies for capital allocation and its efficient usage, together with securitisations, asset sales and issuances of equity instruments (hybrid equity instruments and subordinated debt). |

|

| | | | |

| → | Economic capital |

| The objective of the economic capital model is to ensure that we adequately allocate our capital to cover all the risks to which we are exposed as a result of our activity and risk appetite. It also aims to optimise value creation in the Group and all of the business units. |

|

|

| | | | |

| → | Profitability and pricing |

| Creating value and maximizing profitability is one of Santander's main objectives, carefully selecting the most appropriate markets and portfolios based on profitability, taking into account risk. Profitability and pricing are therefore integral parts of the key capital model processes. |

|

| | | | |

Disciplined capital allocation, prioritizing organic growth and shareholder remuneration, always present in our capital management.

2.3.1. Profitability

One of the main priorities in the Group is capital management, ensuring a profitable capital adequacy in all our activities.

Our strategy includes allocating capital in those markets and portfolios showing the best capital returns, ensuring a strong value creation for shareholders in a sustainable manner.

Identifying and managing underperforming businesses is part of this process, where we hope to optimize Group's capital, targeting customers, portfolios and markets with an interesting capital return, being dynamic, monitoring it actively.

We must encourage the Group's business development within capital and profitability targets through adequate and efficient capital allocation. Our strength is our business model, diversified in businesses and geographically, with solid results, based on risk-adjusted profitability, metrics such as RoTE, RoRWA and RoRAC are part of our admission and monitoring policies.

The combination with a correct pricing adjusted to the risk taken with maintaining a medium-low risk profile is the key to success, having in every moment (including stress scenarios) the needed capital to undertake our corporate strategy.

| | | | | | | | | | | |

29 | | 2021 Pillar 3 Disclosures Report | |

| | |

CAPITAL 2021 Pillar 3 Disclosures Report |

Disciplined capital allocation

A disciplined execution of our capital allocation strategy...

leads to growth, profitability and strength.

| | | | | | | | | | | | | | | | | | | | |

| | | | | | |

| | | | | | |

| — | | — | | — | |

| GROWTH | | PROFITABILITY | | BALANCE SHEET STRENGTH | |

| | | | | | |

| Focused on business that generate high RoTE and high capital generation, along with meaningful potential for growth. | | Focused on maintaining high and sustainable levels through scale in the markets in which we operate, leading to efficiency, and allowing us to provide value to our customers and high returns to our shareholders. | | After years of regulatory capital accumulation, we are focused on maintaining capital levels around 11%-12% on a fully-loaded basis. | |

| | | | | | |

| | | ESG embedded in everything we do | | | |

| | | | | |

Santander's core objectives include creating value and maximising profitability. Therefore, pricing and profitability are among the capital model's key processes.

Pricing is an objective process for determining the right price based on the characteristics of the transaction, product, borrower, segment and market. The process must make sure the price is not below a minimum threshold for, at least, covering funding, operating, credit and capital costs, plus a margin that factors in the sensitivity of demand to price and value generation. Therefore, the pricing process should aim to maximise profitability by creating value on every transaction, customer and/or portfolio and ensuring that minimum return on capital targets are achieved.

The main components and responsibilities of the pricing process are:

| | | | | | | | | | | |

30 | | 2021 Pillar 3 Disclosures Report | |

| | |

CAPITAL 2021 Pillar 3 Disclosures Report |

| | | | | | | | | | | | | | |

| A | | B | | C |

| | | | |

Determining the minimum price | | Integrating pricing into the approval process | | Monitoring of prices and profitability |

| | | | |

The finance function sets the criteria for establishing cost of capital and determining minimum profitability thresholds, ensuring that at least capital, funding, operating and credit costs are covered. The financial management function sets the criteria for establishing cost of funding and the management control function allocates operating costs and passes on financing costs to the businesses. The risk function sets the criteria for measuring expected loss and estimates the parameters used to calculate it. | | The business function is ultimately responsible for the transaction approval process, while the risk function is involved in authorising transactions based on each committee's rules and regulations and the governance of authority, and incorporates profitability metrics and minimum thresholds into the approval process. | | The financial and risk functions are the main functions charged with monitoring trends in profitability using appropriate risk-adjusted profitability metrics and presenting them to the relevant governing bodies. Together with the financial function, the risk function is also responsible for duly recording, controlling and monitoring transactions approved under the defined minimum threshold. The management control function monitors the degree of compliance with the budgeted profitability of each portfolio. |

The capital committee tracks return on capital metrics, the ALCO monitors the status of origination, and the executive risk committee (ERC) ensures that all transactions and customers/portfolios have the appropriate risk profile and create value in line with the agreed-upon return on capital targets. The ERC must also approve the internal models plan and approve the Group's main models, while the model approval forum (MAF) reviews and authorises the models used in the Group's capital management.

To execute this process correctly, Santander has a granular approval process for the SCIB and corporates segments with tools for calculating regulatory and economic return on capital (RoRWA and RoRAC) and determining the appropriate price. For retail segments, granular approval processes using risk-adjusted approval tools are already in place in many cases or are currently being developed. The approval and pricing processes consider the unit's minimum profitability threshold for creating value above cost of capital. Cost of capital is reviewed at least annually and approved by the capital committee. Implementation of a common granular tool for monitoring return on capital among units is now in the advanced stage. Once implemented, it will make it easier to assess profitability, determine whether pricing is commensurate with the level of risk considering the main related costs, and help recommend possible action plans.

Approval tools are used to identify and justify any new loans granted at a price below the minimum threshold. Monitoring tools are used to identify transactions whose profitability is below cost of capital and destroys value, and those for which it must apply measures to raise profitability and deliver on targets. The approval and profitability monitoring processes both have robust approval and review governance for ensuring that the minimum threshold is integrated correctly. An appropriate escalation process is in place for authorising transactions and those approved below the minimum threshold are monitored closely.

In 2022-2023, we will continue with our three-year strategy on resources allocation efficiently, competing where we can achieve the best returns.

With all this, Santander is in an optimal position to ensure appropriate pricing and maximise profitability. It also complies with regulatory requirements, especially the EBA guidelines on loan origination and monitoring published in May 2020 and effective from June 2021, which set out

supervisory expectations regarding the need for risk-based pricing of loans, covering the main costs and ensuring that institutions apply an overall framework in their pricing. These EBA guidelines state that, in pricing, institutions should consider the relevant costs (mainly cost of capital, credit risk costs, cost of funding, and operating and administrative costs), that risk-adjusted indicators should be used as performance measures (e.g. EVA, RoRWA, RoRAC, RoTA), that ex ante transaction tools and regular ex post monitoring should be implemented, and that all material transactions below costs should be reported and properly justified.

The guidelines note that pricing frameworks should be well documented and supported by appropriate governance structures that are responsible for the maintenance of the overall pricing framework and for individual pricing decisions when relevant. In December 2020, the capital committee approved a corporate pricing policy, which sets out the general criteria and describes the main stages for pricing. It also outlines the core components, focusing on the minimum threshold, the need to integrate pricing in approval using ex ante tools and the relevance of defining robust governance and monitoring of recurring profitability. All Group units transposed this corporate policy in 2021, after validation by the corporate teams, to ensure uniformity in interpretation and local implementation. Meanwhile, the risk function drew up and approved three pricing procedures in 2021

•SCIB

•Corporates

•Pooled or personalised treatment

These procedures implement the processes described in the corporate pricing policy, further specifying and allocating the required roles and responsibilities, and governance. These pricing procedures are now being transposed by the units and will also be subject to prior validation by the corporate teams.

2.3.3. Other activities in capital management

Details of the most significant actions undertaken over the year are set out below: