Filed Pursuant to Rule 433

Registration Statement 333-259205

Registration Statement 333-259205

| • |

CUSIP: 78016HDN7

|

| • |

Trade Date: December 23, 2022

|

| • |

Issue Date: December 29, 2022

|

| • |

Valuation Date: January 23, 2024

|

| • |

Maturity Date: January 26, 2024

|

| • |

Term: 13 months

|

| • |

Reference Assets: the S&P 500® Index (SPX) and the Russell 2000® Index (RTY)

|

| • |

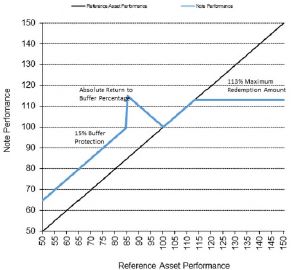

Maximum Redemption Amount: 113% of the principal amount

|

| • |

Buffer Level: 85% of each Initial Level

|

| • |

Buffer Percentage: 15%

|

| • |

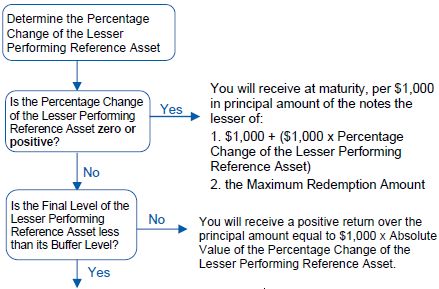

Lesser Performing Reference Asset: the Reference Asset with the lowest Percentage Change

|

| • |

Percentage Change of each Reference Asset:

|

| • |

Absolute Value of Percentage Change: -1 x Percentage Change

|

| • |

Payment at maturity linked to the Reference Asset with the lowest Percentage Change.

|

| • |

Receive a return equal to the Percentage Change if the level of the Lesser Performing Reference Asset increases from its Initial Level to the Final Level, subject to the Maximum Redemption Amount.

|

| • |

Positive return equal to the Absolute Value of the Percentage Change of the Lesser Performing Reference Asset, if that Reference Asset decreases by not more than 15%.

|

| • |

Subject to 1% loss of the principal amount for each 1% that the Lesser Performing Reference Asset decreases beyond its Buffer Level if its Final Level is less than its Buffer Level.

|

| • |

The notes are subject to Royal Bank of Canada’s credit risk.

|

| • |

The return on the Notes is capped.

|

| • |

The notes are not principal protected.

|

| • |

Your notes are likely to have limited liquidity.

|

| • |

Please see the following page for important risk factor information.

|

| • |

Each investor will agree to treat the notes as a pre-paid cash-settled derivative contract for U.S. federal income tax purposes, as described in more detail in the product prospectus supplement.

|

DETERMINING PAYMENT AT MATURITY

If the Final Level of the Lesser Performing Reference Asset is less than its Buffer Level, you will lose 1% of the principal amount for each 1% decline in the level of that

Reference Asset beyond its Buffer Level. The payment at maturity per $1,000 in principal amount of the notes will be calculated as follows:

$1,000 + [$1,000 x (Percentage Change of the Lesser Performing Reference Asset + 15%)]

Additional Key Information:

This document is a summary of the preliminary terms of an equity linked note that Royal Bank of Canada will issue. It does not contain all of the material terms of, or risks related to, these

notes. You should read the preliminary terms supplement for the notes and the documents described above before investing. In addition, you should consult your accounting, legal and tax advisors before investing. The preliminary terms

supplement for this offering will be provided to you prior to your investment decision, and it may also be accessed here:

The notes are not bail-inable notes under the Canada Deposit Insurance Corporation Act.

You should review the preliminary terms supplement carefully prior to investing in the notes. In particular, you should carefully review the relevant risk factors set forth therein, including,

but not limited to, the following:

| • |

You May Lose a Significant Portion of Your Principal Amount, Depending Upon the Performance of the Lesser Performing Reference Asset.

|

| • |

The Return on the Notes Is Subject to the Maximum Redemption Amount.

|

| • |

The Notes Do Not Pay Interest and Your Return May Be Lower than the Return on a Conventional Debt Security of Comparable Maturity.

|

| • |

Payments on the Notes Are Subject to Our Credit Risk, and Changes in Our Credit Ratings Are Expected to Affect the Market Value of the Notes.

|

| • |

The Payment on the Notes Are Linked to the Lesser Performing Reference Asset, Regardless of the Performance of the Other Reference Asset.

|

| • |

There May Not Be an Active Trading Market for the Notes—Sales in the Secondary Market May Result in Significant Losses.

|

| • |

You Will Not Have Any Rights to the Securities Included in the Reference Assets.

|

| • |

An Investment in the Notes Is Subject to Risks Relating to Small Capitalization Stocks

|

| • |

The Initial Estimated Value of the Notes Will Be Less than the Price to the Public.

|

| • |

The Initial Estimated Value of the Notes that We Will Provide in the Final Pricing Supplement Will Be an Estimate Only, Calculated as of the Time the Terms of the Notes Are Set.

|

| • |

Our Business Activities May Create Conflicts of Interest.

|

| • |

The Payment at Maturity and the Valuation Date Are Subject to Postponement if a Market Disruption Event Occurs.

|

The SPX is a product of S&P Dow Jones Indices LLC, a division of S&P Global, or its affiliates (“SPDJI”), and has been licensed for use by Royal Bank of Canada. Standard & Poor’s®

and S&P® are registered trademarks of Standard & Poor’s Financial Services LLC, a division of S&P Global (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (“Dow Jones”). The

Notes are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P or their respective affiliates, and none of such parties make any representation regarding the advisability of investing in the Notes nor do they have any

liability for any errors, omissions, or interruptions of the SPX.

The Notes are not sponsored, endorsed, sold or promoted by FTSE Russell. FTSE Russell makes no representation or warranty, express or implied, to the owners of the Notes or any member of the

public regarding the advisability of investing in securities generally or in the Notes particularly or the ability of the RTY to track general stock market performance or a segment of the same. FTSE Russell’s publication of the RTY in no way

suggests or implies an opinion by FTSE Russell as to the advisability of investment in any or all of the stocks upon which the RTY is based. FTSE Russell's only relationship to Royal Bank is the licensing of certain trademarks and trade names

of FTSE Russell and of the RTY, which is determined, composed and calculated by FTSE Russell without regard to Royal Bank or the Notes. FTSE Russell is not responsible for and has not reviewed the Notes nor any associated literature or

publications and FTSE Russell makes no representation or warranty express or implied as to their accuracy or completeness, or otherwise. FTSE Russell reserves the right, at any time and without notice, to alter, amend, terminate or in any way

change the RTY. FTSE Russell has no obligation or liability in connection with the administration, marketing or trading of the Notes.

Royal Bank of Canada has filed a registration statement (including a product prospectus supplement, a prospectus supplement, and a prospectus) with the SEC for the offering to which this document relates. Before you

invest, you should read those documents and the other documents relating to this offering that we have filed with the SEC for more complete information about us and this offering. You may obtain these documents without cost by visiting EDGAR on

the SEC website at www.sec.gov. Alternatively, Royal Bank of Canada, any agent or any dealer participating in this offering will arrange to send you the product prospectus supplement, the prospectus supplement and the prospectus if you so

request by calling toll-free at 1-877-688-2301.