![]()

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Dividend Growth Fund

Growth Opportunities Fund

Small Cap Value Fund

For the fiscal year ended November 30, 2022

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-06650

LORD ABBETT RESEARCH FUND, INC.

(Exact name of Registrant as specified in charter)

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Address of principal executive offices) (Zip code)

Lawrence B. Stoller, Esq.

Vice President, Secretary, and Chief Legal Officer

90 Hudson Street, Jersey City, New Jersey 07302-3973

(Name and address of agent for service)

Registrant’s telephone number, including area code: (888) 522-2388

Date of fiscal year end: 11/30

Date of reporting period: 11/30/2022

| Item 1: | Report(s) to Shareholders. |

![]()

LORD ABBETT

ANNUAL REPORT

Lord Abbett

Dividend Growth Fund

Growth Opportunities Fund

Small Cap Value Fund

For the fiscal year ended November 30, 2022

Table of Contents

Lord Abbett Dividend Growth Fund,

Lord Abbett Growth Opportunities Fund, and

Lord Abbett Small Cap Value Fund

Annual Report

For the fiscal year ended November 30, 2022

From left to right: James L.L. Tullis, Independent Chair of the Lord Abbett Funds and Douglas B. Sieg Director, President and Chief Executive Officer of the Lord Abbett Funds.

Dear Shareholders: We are pleased to provide you with this overview of the performance of the Funds for the fiscal year ended November 30, 2022. On this page and the following pages, we discuss the major factors that influenced fiscal year performance. For detailed and timely information about the Funds, please visit our website at www.lordabbett.com, where you can also access the quarterly commentaries that provide updates on each Fund’s performance and other portfolio related updates.

Thank you for investing in Lord Abbett mutual funds. We value the trust that you place in us and look forward to serving your investment needs in the years to come.

Best regards,

Douglas B. Sieg

Director, President and Chief Executive Officer

Lord Abbett Dividend Growth Fund

For the fiscal year ended November 30, 2022, the Fund returned -5.30%, reflecting performance at the net asset value (“NAV”) of Class A shares with all distributions reinvested, compared to its benchmark, the S&P 500® Index1, which returned -9.21% over the same period.

U.S. markets faced many challenges throughout the twelve-month period

ending November 30, 2022, including the spread of the Omicron variant of COVID-19, supply chain dislocations, labor shortages, inflationary pressures, tighter fiscal and monetary policy, and Russia’s invasion of Ukraine. The Dow Jones Industrial Average was up 2.48% and the S&P 500® Index1 fell -9.21%, while the tech-heavy Nasdaq Composite lost -25.59%. Value stocks2 significantly outperformed growth stocks3 (1.95%

1

vs -21.59%), while large cap stocks4 outperformed small cap stocks5 (-10.66% vs -13.01%).

In November 2021, just prior to the start of the period, the World Health Organization designated the newly discovered Omicron variant as a “variant of concern”, leading to one of the largest selloffs of U.S. risk assets since the start of the pandemic, amid fears that the world would succumb to a new wave of infections. U.S. cases hit the highest levels of the pandemic in December, rising above 580,000 new cases in the last week of the month, more than doubling the previous record high. Yet, negative sentiment quickly reversed as cases proved to be generally less severe than prior strains. Market sentiment also increased after the Center for Disease Control shortened its suggested isolation policy for those infected from 10 days to five.

Inflationary concerns began to take focus towards the end of 2021 and became a dominant story throughout the period. Headline consumer price index (CPI) readings had hovered a little above 5% year-over-year for most of 2021, which led investors to question whether this period of rising prices would be more persistent than originally thought. This debate was intensified by November’s headline consumer price index rising 6.8% year-over-year, the fastest pace since 1982. The sharp increase in prices was generally due to supply and demand imbalances across multiple industries, led initially by energy, food, and used cars.

Inflation readings continued to climb throughout the first half of 2022, peaking at 9.1% year-over-year in June.

Energy costs were the primary driver of inflation for the period, rising more than 30% year-over-year by the end of June. The energy sector, which had been subject to rising consumer demand as global economies reopened from lockdowns induced by COVID-19, faced added friction with Russia’s invasion of Ukraine. Investors were concerned about the secondary effects of the war, particularly from a commodity and supply chain standpoint. Russia has been a large exporter of oil and certain minerals, and the various sanctions set on Russia from Western nations led to a surge in commodity prices, with crude oil reaching over $100 per barrel for the first time since 2014.

The surge in prices forced the U.S. Federal Reserve (Fed) into a more aggressive approach to combating inflation. After remaining mostly consistent in its messaging that price pressures would likely be transitory, elevated and more persistent inflation pressures caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee meeting, the first hike in more than three years. Five additional rate hikes of 50 bps, 75 bps, 75 bps, 75 bps, and 75 bps, respectively, followed in the succeeding months as inflation prints continued to come in hotter than expected, resulting in a

2

federal funds rate of 4.00% by November 2, 2022. Bond yields shot up in response to this aggressive policy, leading to a bearish curve flattening and ultimately a yield curve inversion, as shorter-term yields moved higher than longer-term yields.

Separately, global markets faced increased geopolitical tensions due to Russia’s invasion of Ukraine on February 23rd. Tensions remained elevated for the remainder of the twelve-month period, as Russia continued to weaponize energy flows, annexed four Ukrainian regions, and ratcheted up its nuclear warnings. In addition, the rhetoric between the U.S. and China over Taiwan further heated up after U.S. House of Representatives Speaker Nancy Pelosi visited Taiwan in August. China responded to the trip with large-scale military drills, which led to a pledge by U.S. President Joe Biden to defend the democratically governed island.

Key macroeconomic indicators mostly trended lower throughout the period, with the U.S. reporting negative gross domestic product of -1.6% in the first quarter of 2022 and -0.9% in the second quarter before returning to growth in the third quarter. Worries among investors that a recession was pending continued to grow, leading to a decline in consumer sentiment to lower levels than during the height of the COVID-19 pandemic and the global financial crisis of 2008 as measured by the consumer confidence index.

Despite rising recessionary signs, select bright spots in the U.S. economy supported

the idea that a potential recession would be shallow. For example, one positive development was the peak inflation narrative, which included a 99 day stretch of declines in U.S. gasoline prices and October CPI coming in better than expected on both the headline and core numbers. In addition, apartment rents fell for the first time in nearly two years in July, and lumber prices declined by more than 70% from their March peak late in the third quarter, falling back to pre-COVID levels. The second quarter of 2022 earnings season also generated a lot of “better-than-feared” takeaways, including a common theme of relatively stable demand and pricing power protecting margins. Third-quarter earnings were slightly below expectations but provided evidence of healthy consumer spending. Capital return and capital expenditures were also mentioned as relative bright spots as companies flagged easing labor shortages and supply chain constraints. The U.S. labor market also remained strong over the period, with the national unemployment rate at 3.7% as of the end of November.

In terms of the Fund’s key performance drivers, over the 12-month period ending November 30, 2022, security selection within the industrials sector contributed to the Fund’s relative performance. Within the industrials sector, Northrop Grumman Corp., a defense contractor, contributed most to relative performance. The ongoing tensions between Russia and Ukraine built

3

up momentum in the defense sector and the U.S. government is Northrop Grumman’s largest customer. We expect Northrop Grumman to be the fastest growing U.S. defense contractor based on its large and ramping growth platforms that serve critical U.S. needs including Ground Based Strategic Deterrent (GBSD) and satellites. The Fund’s position in AbbVie, Inc., a research-based biopharmaceutical company, also contributed to relative performance. Shares rallied in the first half of the year, up almost 50% at the peak in early April. The stock price move was supported by the company’s strong fourth quarter earnings and fiscal year guidance, which came in above expectations. The Fund’s position in McDonald’s Corporation, a multinational fast-food chain, contributed to relative performance. Shares rallied after the company reported strong third quarter earnings that demonstrated broad-based business momentum as global comparable sales increased nearly 10%. The company also increased the quarterly dividend by more than 10%.

Conversely, one of the largest detractors from relative performance during the 12-month period ending November 30, 2022, was NVIDIA Corp., an American multinational technology company. The company’s gaming segment was adversely impacted by material economic slowdowns in China and Europe, which led to a selloff in shares of NVIDIA. Government restrictions were introduced in September, which

limited the company’s ability to sell certain products into China, which compounded the sell off. Within the health care sector, the Fund’s allocation to West Pharmaceutical, which manufactures and markets pharmaceuticals, biologics, vaccines and consumer healthcare products, was one of the largest detractors from relative performance. The company reported first quarter earnings that were modestly ahead of expectations, coupled with an earnings guidance increase. Despite the better-than-expected quarter, shares sold off as the company continued to face foreign exchange rate headwinds as the U.S. dollar strengthened and investors worried that a faster-than-expected fall-off in COVID-19 related order flow would result in underutilization of new capacity. The Fund’s position in Estée Lauder Companies, Inc., which engages in the manufacturing of skin care, makeup, fragrance, and hair care products, detracted from relative performance. Shares sold off following Russia’s invasion of Ukraine. After suspending The Estée Lauder Companies’ business investments and initiatives in Russia, the company also decided to suspend all commercial activity in Russia, including closing every store it owns and operates, as well as its brand sites and shipments to any of its retailers in Russia.

Lord Abbett Growth Opportunities Fund

For the fiscal year ended November 30, 2022, the Fund returned -27.23%,

4

reflecting performance at the net asset value (“NAV”) of Class A shares with all distributions reinvested, compared to its benchmark, the Russell Midcap® Growth Index,6 which returned -21.77% over the same period.

U.S. markets faced many challenges throughout the twelve-month period ending November 30, 2022, including the spread of the Omicron variant of COVID-19, supply chain dislocations, labor shortages, inflationary pressures, tighter fiscal and monetary policy, and Russia’s invasion of Ukraine. The Dow Jones Industrial Average was up 2.48% and the S&P 500® Index1 fell -9.21%, while the tech-heavy Nasdaq Composite lost -25.59%. Value stocks2 significantly outperformed growth stocks3 (1.95% vs -21.59%), while large cap stocks4 outperformed small cap stocks5 (-10.66% vs -13.01%).

In November 2021, just prior to the start of the period, the World Health Organization designated the newly discovered Omicron variant as a “variant of concern”, leading to one of the largest selloffs of U.S. risk assets since the start of the pandemic, amid fears that the world would succumb to a new wave of infections. U.S. cases hit the highest levels of the pandemic in December, rising above 580,000 new cases in the last week of the month, more than doubling the previous record high. Yet, negative sentiment quickly reversed as cases proved to be generally less severe than prior strains. Market sentiment also increased after the

Center for Disease Control shortened its suggested isolation policy for those infected from 10 days to five.

Inflationary concerns began to take focus towards the end of 2021 and became a dominant story throughout the period. Headline consumer price index (CPI) readings had hovered a little above 5% year-over-year for most of 2021, which led investors to question whether this period of rising prices would be more persistent than originally thought. This debate was intensified by November’s headline consumer price index rising 6.8% year-over-year, the fastest pace since 1982. The sharp increase in prices was generally due to supply and demand imbalances across multiple industries, led initially by energy, food, and used cars. Inflation readings continued to climb throughout the first half of 2022, peaking at 9.1% year-over-year in June.

Energy costs were the primary driver of inflation for the period, rising more than 30% year-over-year by the end of June. The energy sector, which had been subject to rising consumer demand as global economies reopened from lockdowns induced by COVID-19, faced added friction with Russia’s invasion of Ukraine. Investors were concerned about the secondary effects of the war, particularly from a commodity and supply chain standpoint. Russia has been a large exporter of oil and certain minerals, and the various sanctions set on Russia from Western nations led to a surge in commodity prices, with crude oil reaching over $100 per barrel for the first time since 2014.

5

The surge in prices forced the U.S. Federal Reserve (Fed) into a more aggressive approach to combating inflation. After remaining mostly consistent in its messaging that price pressures would likely be transitory, elevated and more persistent inflation pressures caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee meeting, the first hike in more than three years. Five additional rate hikes of 50 bps, 75 bps, 75 bps, 75 bps, and 75 bps, respectively, followed in the succeeding months as inflation prints continued to come in hotter than expected, resulting in a federal funds rate of 4.00% by November 2, 2022. Bond yields shot up in response to this aggressive policy, leading to a bearish curve flattening and ultimately a yield curve inversion, as shorter-term yields moved higher than longer-term yields.

Separately, global markets faced increased geopolitical tensions due to Russia’s invasion of Ukraine on February 23rd. Tensions remained elevated for the remainder of the twelve-month period, as Russia continued to weaponize energy flows, annexed four Ukrainian regions, and ratcheted up its nuclear warnings. In addition, the rhetoric between the U.S. and China over Taiwan further heated up after U.S. House of Representatives Speaker Nancy Pelosi visited Taiwan in August. China

responded to the trip with large-scale military drills, which led to a pledge by U.S. President Joe Biden to defend the democratically governed island.

Key macroeconomic indicators mostly trended lower throughout the period, with the U.S. reporting negative gross domestic product of -1.6% in the first quarter of 2022 and -0.9% in the second quarter before returning to growth in the third quarter. Worries among investors that a recession was pending continued to grow, leading to a decline in consumer sentiment to lower levels than during the height of the COVID-19 pandemic and the global financial crisis of 2008 as measured by the consumer confidence index.

Despite rising recessionary signs, select bright spots in the U.S. economy supported the idea that a potential recession would be shallow. For example, one positive development was the peak inflation narrative, which included a 99 day stretch of declines in U.S. gasoline prices and October CPI coming in better than expected on both the headline and core numbers. In addition, apartment rents fell for the first time in nearly two years in July, and lumber prices declined by more than 70% from their March peak late in the third quarter, falling back to pre-COVID levels. The second quarter of 2022 earnings season also generated a lot of “better-than-feared” takeaways, including a common theme of relatively stable demand and pricing power protecting margins. Third-quarter earnings were

6

slightly below expectations but provided evidence of healthy consumer spending. Capital return and capital expenditures were also mentioned as relative bright spots as companies flagged easing labor shortages and supply chain constraints. The U.S. labor market also remained strong over the period, with the national unemployment rate at 3.7% as of the end of November.

Over the 12-month period ending November 30, 2022, Lord Abbett made the strategic decision to offer a single style of growth investing, led by our Innovation Growth team, which is directed by F. Thomas O’Halloran, J.D., CFA, Partner & Portfolio Manager, and Matthew DeCicco, CFA, Partner & Director of Equities. As a result of this enhanced focus, the investment strategy, philosophy and process of the Growth Opportunities Fund changed to become consistent with the rest of the innovation growth suite of products. As such, the Fund’s portfolio management team seeks to invest in the stocks of companies with strong business models, management, and competitive positions that are targeting markets that appear most likely to benefit from increased innovation.

As a result of supply chain dislocations, labor shortages, inflationary pressures, tighter fiscal and monetary policy, and the war in Ukraine, high innovation small and midcap companies, particularly those aggressively reinvesting in research and development to drive future revenues and

earnings, underperformed lower growth, lower valuation names within the index during the period as the market has largely expressed a technical preference for companies with positive earnings today, compared to larger growth potential in the future. As such, the portfolio’s exposure to small and midcap secular growth companies, such as MongoDB, Inc., a general-purpose database platform, was a primary drag on relative performance.

In addition, having no exposure to stock of companies related to the oil, gas, and consumable fuel industry throughout the first few months of 2022 was also a primary detractor from relative performance, as geopolitical tensions that ultimately culminated in the Russian invasion of Ukraine resulted in oil prices rising above $120 per barrel in March as the market anticipated a supply shortage.

The Fund’s position in Roku, Inc., a manufacturer of digital media players for video streaming, was the largest individual detractor from relative performance. In February, shares of the stock fell after the company reported a revenue miss for the fourth quarter of 2021 and gave first-quarter 2022 guidance that was below analysts’ expectations. Management blamed the slowing revenue growth on continued supply chain disruptions impacting the U.S. television market.

The Fund’s position in Enphase Energy, Inc., an energy technology company that develops and manufactures solar micro-inverters, battery energy storage, and

7

electric vehicle charging stations, was a prominent contributor to relative performance over the period. Enphase has benefited greatly from increased demand for solar solutions in Europe as a result of persistent energy shortages. In the company’s most recent quarterly earnings report, management reported top- and bottom-line earnings results that exceeded consensus expectations. Notably, Enphase’s reported strong revenue growth driven by growth in microinverter and IQ Battery shipments. As of the end of the fiscal year, Enphase is one of the portfolio’s top active overweights.

The Fund’s position in Intra-Cellular Therapies, a developer of innovative treatments for individuals with neuropsychiatric and neurologic disorders, was also a notable contributor to relative performance. Shares soared following the FDA’s approval of CAPLYTA®, the first and only FDA-approved treatment for depressive episodes in adults with bipolar I or II disorders. Positive momentum of the stock continued into 2022 as a result of the drug’s successful initial launch, as well as the company reporting strong first quarter 2022 earnings.

Lord Abbett Small Cap Value Fund

For the fiscal year ended November 30, 2022, the Fund returned -9.18% reflecting performance at the net asset value (“NAV”) of Class A shares with all distributions reinvested, compared to its benchmark, the

Russell 2000 Value® Index7, which returned -4.75% over the same period.

U.S. markets faced many challenges throughout the twelve-month period ending November 30, 2022, including the spread of the Omicron variant of COVID-19, supply chain dislocations, labor shortages, inflationary pressures, tighter fiscal and monetary policy, and Russia’s invasion of Ukraine. The Dow Jones Industrial Average was up 2.48% and the S&P 500® Index1 fell -9.21%, while the tech-heavy Nasdaq Composite lost -25.59%. Value stocks2 significantly outperformed growth stocks3 (1.95% vs -21.59%), while large cap stocks4 outperformed small cap stocks5 (-10.66% vs -13.01%).

In November 2021, just prior to the start of the period, the World Health Organization designated the newly discovered Omicron variant as a “variant of concern”, leading to one of the largest selloffs of U.S. risk assets since the start of the pandemic, amid fears that the world would succumb to a new wave of infections. U.S. cases hit the highest levels of the pandemic in December, rising above 580,000 new cases in the last week of the month, more than doubling the previous record high. Yet, negative sentiment quickly reversed as cases proved to be generally less severe than prior strains. Market sentiment also increased after the Center for Disease Control shortened its suggested isolation policy for those infected from 10 days to five.

8

Inflationary concerns began to take focus towards the end of 2021 and became a dominant story throughout the period. Headline consumer price index (CPI) readings had hovered a little above 5% year-over-year for most of 2021, which led investors to question whether this period of rising prices would be more persistent than originally thought. This debate was intensified by November’s headline consumer price index rising 6.8% year-over-year, the fastest pace since 1982. The sharp increase in prices was generally due to supply and demand imbalances across multiple industries, led initially by energy, food, and used cars. Inflation readings continued to climb throughout the first half of 2022, peaking at 9.1% year-over-year in June.

Energy costs were the primary driver of inflation for the period, rising more than 30% year-over-year by the end of June. The energy sector, which had been subject to rising consumer demand as global economies reopened from lockdowns induced by COVID-19, faced added friction with Russia’s invasion of Ukraine. Investors were concerned about the secondary effects of the war, particularly from a commodity and supply chain standpoint. Russia has been a large exporter of oil and certain minerals, and the various sanctions set on Russia from Western nations led to a surge in commodity prices, with crude oil reaching over $100 per barrel for the first time since 2014.

The surge in prices forced the U.S. Federal Reserve (Fed) into a more

aggressive approach to combating inflation. After remaining mostly consistent in its messaging that price pressures would likely be transitory, elevated and more persistent inflation pressures caused the Fed to move the target federal funds rate into more restrictive territory. This resulted in a 25-basis point (bps) hike in the federal funds rate at the March Federal Open Market Committee meeting, the first hike in more than three years. Five additional rate hikes of 50 bps, 75 bps, 75 bps, 75 bps, and 75 bps, respectively, followed in the succeeding months as inflation prints continued to come in hotter than expected, resulting in a federal funds rate of 4.00% by November 2, 2022. Bond yields shot up in response to this aggressive policy, leading to a bearish curve flattening and ultimately a yield curve inversion, as shorter-term yields moved higher than longer-term yields.

Separately, global markets faced increased geopolitical tensions due to Russia’s invasion of Ukraine on February 23rd. Tensions remained elevated for the remainder of the twelve-month period, as Russia continued to weaponize energy flows, annexed four Ukrainian regions, and ratcheted up its nuclear warnings. In addition, the rhetoric between the U.S. and China over Taiwan further heated up after U.S. House of Representatives Speaker Nancy Pelosi visited Taiwan in August. China responded to the trip with large-scale military drills, which led to a pledge

9

by U.S. President Joe Biden to defend the democratically governed island.

Key macroeconomic indicators mostly trended lower throughout the period, with the U.S. reporting negative gross domestic product of -1.6% in the first quarter of 2022 and -0.9% in the second quarter before returning to growth in the third quarter. Worries among investors that a recession was pending continued to grow, leading to a decline in consumer sentiment to lower levels than during the height of the COVID-19 pandemic and the global financial crisis of 2008 as measured by the consumer confidence index.

Despite rising recessionary signs, select bright spots in the U.S. economy supported the idea that a potential recession would be shallow. For example, one positive development was the peak inflation narrative, which included a 99 day stretch of declines in U.S. gasoline prices and October CPI coming in better than expected on both the headline and core numbers. In addition, apartment rents fell for the first time in nearly two years in July, and lumber prices declined by more than 70% from their March peak late in the third quarter, falling back to pre-COVID levels. The second quarter of 2022 earnings season also generated a lot of “better-than-feared” takeaways, including a common theme of relatively stable demand and pricing power protecting margins. Third-quarter earnings were slightly below expectations but provided evidence of healthy consumer spending.

Capital return and capital expenditures were also mentioned as relative bright spots as companies flagged easing labor shortages and supply chain constraints. The U.S. labor market also remained strong over the period, with the national unemployment rate at 3.7% as of the end of November.

In terms of the Fund’s key performance drivers during the 12-month period ending November 30, 2022, the Fund’s position in Spectrum Brands Holdings, Inc., a consumer products and home essentials company, detracted from relative performance. Shares fell after Assa Abloy, which engages in the provision of intelligent lock and security solutions, issued a statement regarding the U.S. DOJ’s blocking of Assa Abloys’s proposed acquisition of the hardware and home improvement division of Spectrum Brands. The Fund’s position in Customers Bancorp, Inc., a bank holding company, also detracted from relative performance. Amid the flattening of the yield curve and skepticism around global growth prospects, banks have come under pressure. Shares continued to fall following two consecutive quarters of lower-than-expected earnings per share. The Fund’s position in Century Aluminum Co., a producer of aluminum and operator of aluminum reduction facilities, or smelters, in the United States and Iceland, detracted from relative performance. Shares fell as power costs increased early in the year, with the expectation that higher prices

10

would continue through the summer. Electricity prices typically comprise approximately 1/3 of smelter costs. In addition to this, it became evident there was a much smaller global aluminum supply deficit than anticipated, largely due to weaker China demand and excess supply.

Conversely, the largest contributor to relative performance during the 12-month period ending November 30, 2022, was International Money Express, Inc, a leading money remittance services company. Shares rallied after the company reported fourth quarter earnings above expectations, followed by another strong first quarter earnings report. The company subsequently increased second quarter earnings guidance. We believe their valuation remains attractive and they are well positioned for further growth. The Fund’s position in Cars.com, Inc., a leading automotive marketplace platform, contributed to relative performance. Shares rallied after the company reported strong second quarter earnings where revenue and adjusted earnings before interest, taxes, depreciation, and

amortization (EBITDA) beat expectations. Subsequently, the company issued third quarter guidance stating they expect revenue growth to accelerate and projected growth of 6-8% year-over-year in the second half of 2022. The Fund’s position in Silicon Motion Technology, which engages in the development, manufacturing, and supply of semiconductor products for the electronics market, was the largest contributor to relative performance within the sector. Silicon Motion Technology was a significant contributor to relative performance in the first half of the year. Shares rallied following the announcement that MaxLinear, which provides highly integrated radio-frequency analog and mixed-signal semiconductor products for broadband communications applications, would acquire Silicon Motion Technology.

Each Fund’s portfolio is actively managed and, therefore, holdings and the weightings of a particular issuer or particular sector as a percentage of portfolio assets are subject to change. Sectors may include many industries.

1 The S&P 500® Index is widely regarded as the standard for measuring large cap U.S. stock market performance and includes a representative sample of leading companies in leading industries.

2 As represented by the Russell 3000® Value Index as of 11/30/2022.

3 As represented by the Russell 3000® Growth Index as of 11/30/2022.

4 As represented by the Russell 1000® Index as of 11/30/2022.

5 As represented by the Russell 2000® Index as of 11/30/2022.

6 The Russell Midcap® Growth Index measures the performance of those Russell Midcap® companies with higher price-to-book ratios and higher forecasted growth values.

7 The Russell 2000 Value® Index measures the performance of those stocks of the Russell 2000® Index with lower price-to-book ratios and lower relative forecasted growth rates.

Indices are unmanaged, do not reflect the deduction of fees or expenses, and an investor cannot invest directly in an index.

11

Unless otherwise specified, indexes reflect total return, with all dividends reinvested. Indexes are unmanaged, do not reflect the deduction of fees or expenses, and are not available for direct investment.

Important Performance and Other Information Performance data quoted in the following pages reflect past performance and are no guarantee of future results. Current performance may be higher or lower than the performance quoted. The investment return and principal value of an investment in the Funds will fluctuate so that shares, on any given day or when redeemed, may be worth more or less than their original cost. You can obtain performance data current to the most recent month end by calling Lord Abbett at 888-522-2388 or referring to www.lordabbett.com.

Except where noted, comparative Fund performance does not account for the deduction of sales charges and would be different if sales charges were included. Each Fund offers classes of shares with distinct pricing options. For a full description of the differences in pricing alternatives, please see each Fund’s prospectus.

During certain periods shown, expense waivers and reimbursements were in place. Without such waivers and expense reimbursements, the Funds’ returns would have been lower.

The annual commentary above discusses the views of the Funds’ management and various portfolio holdings of the Funds as of November 30, 2022. These views and portfolio holdings may have changed after this date. Information provided in the commentary is not a recommendation to buy or sell securities. Because the Funds’ portfolios are actively managed and may change significantly, the Funds may no longer own the securities described above or may have otherwise changed their positions in the securities. For more recent information about the Funds’ portfolio holdings, please visit www.lordabbett.com.

A Note about Risk: See Notes to Financial Statements for a discussion of investment risks. For a more detailed discussion of the risks associated with each Fund, please see each Fund’s prospectus.

Mutual funds are not insured by the FDIC, are not deposits or other obligations of, or guaranteed by, banks, and are subject to investment risks including possible loss of principal amount invested.

12

Dividend Growth Fund

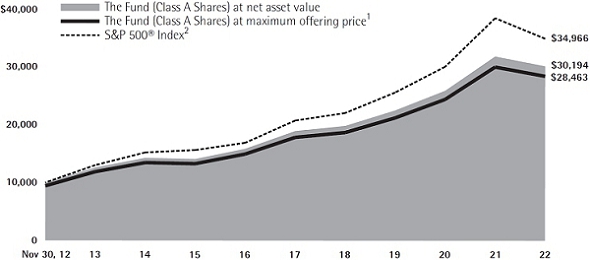

Below is a comparison of a $10,000 investment in Class A shares with the same investment in the S&P 500® Index, assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total

Returns at Maximum Applicable

Sales Charge for the Periods Ended November 30, 2022

| 1 Year | 5 Years | 10 Years | Life of Class | ||||||

| Class A3 | -10.76% | 8.49% | 11.03% | – | |||||

| Class C4 | -6.88% | 8.95% | 10.85% | – | |||||

| Class F5 | -5.05% | 10.05% | 11.92% | – | |||||

| Class F36 | -4.95% | 10.13% | – | 11.34% | |||||

| Class I5 | -5.04% | 10.05% | 11.97% | – | |||||

| Class P5 | -5.46% | 9.55% | 11.46% | – | |||||

| Class R25 | -5.64% | 9.39% | 11.29% | – | |||||

| Class R35 | -5.53% | 9.51% | 11.42% | – | |||||

| Class R47 | -5.30% | 9.78% | – | 10.96% | |||||

| Class R57 | -5.09% | 10.06% | – | 11.23% | |||||

| Class R67 | -5.00% | 10.14% | – | 11.32% |

13

1 Reflects the deduction of the maximum initial sales charge of 5.75%.

2 Performance for the unmanaged index does not reflect any fees or expenses. The performance of each index is not necessarily representative of the Fund’s performance.

3 Total return, which is the percentage change in net asset value, after deduction of the maximum initial sales charge of 5.75% applicable to Class A shares, with all dividends and distributions reinvested for the periods shown ended November 30, 2022, is calculated using the SEC-required uniform method to compute such return.

4 The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Performance is at net asset value.

6 Commenced operations and performance for the Class began on April 4, 2017. Performance is at net asset value.

7 Commenced operations and performance for the Class began on June 30, 2015. Performance is at net asset value.

14

Growth Opportunities Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in both the Russell Midcap® Growth Index and the Russell Midcap® Index, assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total

Returns at Maximum Applicable

Sales Charge for the Periods Ended November 30, 2022

| 1 Year | 5 Years | 10 Years | Life of Class | ||||||

| Class A3 | -31.41% | 6.32% | 9.87% | – | |||||

| Class C4 | -28.27% | 6.79% | 9.73% | – | |||||

| Class F5 | -27.09% | 7.75% | 10.71% | – | |||||

| Class F36 | -26.98% | 7.93% | – | 9.82% | |||||

| Class I5 | -27.03% | 7.86% | 10.82% | – | |||||

| Class P5 | -27.35% | 7.38% | 10.33% | – | |||||

| Class R25 | -27.44% | 7.22% | 10.16% | – | |||||

| Class R35 | -27.39% | 7.32% | 10.27% | – | |||||

| Class R47 | -27.19% | 7.59% | – | 7.34% | |||||

| Class R57 | -27.01% | 7.86% | – | 7.61% | |||||

| Class R67 | -26.96% | 7.93% | – | 7.71% |

1 Reflects the deduction of the maximum initial sales charge of 5.75%.

2 Performance for each unmanaged index does not reflect any fees or expenses. The performance of each index is not necessarily representative of the Fund’s performance.

3 Total return, which is the percentage change in net asset value, after deduction of the maximum initial sales charge of 5.75% applicable to Class A shares, with all dividends and distributions reinvested for the periods shown ended November 30, 2022, is calculated using the SEC–required uniform method to compute such return.

4 The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Performance is at net asset value.

6 Commenced operations and performance for the Class began on April 4, 2017. Performance is at net asset value.

7 Commenced operations and performance for the Class began on June 30, 2015. Performance is at net asset value.

15

Small Cap Value Fund

Investment Comparison

Below is a comparison of a $10,000 investment in Class A shares with the same investment in both the Russell 2000® Value Index, assuming reinvestment of all dividends and distributions. The performance of the other classes will be greater than or less than the performance shown in the graph below due to different sales loads and expenses applicable to such classes. The graph and performance table below do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. During certain periods, expenses of the Fund have been waived or reimbursed by Lord Abbett; without such waiver or reimbursement of expenses, the Fund’s returns would have been lower. Past performance is no guarantee of future results.

Average Annual Total Returns at Maximum

Applicable

Sales Charge for the Periods Ended November 30, 2022

| 1 Year | 5 Years | 10 Years | Life of Class | ||||||

| Class A3 | -14.38% | 1.16% | 6.63% | – | |||||

| Class C4 | -10.55% | 1.57% | 6.46% | – | |||||

| Class F5 | -8.99% | 2.53% | 7.44% | – | |||||

| Class F36 | -8.85% | 2.71% | – | 3.86% | |||||

| Class I5 | -8.95% | 2.63% | 7.54% | – | |||||

| Class P5 | -9.33% | 2.17% | 7.06% | – | |||||

| Class R25 | -9.46% | 2.02% | 6.90% | – | |||||

| Class R35 | -9.41% | 2.13% | 7.02% | – | |||||

| Class R47 | -9.14% | 2.38% | – | 4.44% | |||||

| Class R57 | -8.93% | 2.63% | – | 4.71% | |||||

| Class R67 | -8.81% | 2.72% | – | 4.80% |

1 Reflects the deduction of the maximum initial sales charge of 5.75%.

2 Performance for each unmanaged index does not reflect any fees or expenses. The performance of each index is not necessarily representative of the Fund’s performance.

3 Total return, which is the percentage change in net asset value, after deduction of the maximum initial sales charge of 5.75% applicable to Class A shares, with all dividends and distributions reinvested for the periods shown ended November 30, 2022, is calculated using the SEC-required uniform method to compute such return.

4 The 1% CDSC for Class C shares normally applies before the first anniversary of the purchase date. Performance for other periods is at net asset value.

5 Performance is at net asset value.

6 Commenced operations and performance for the Class began on April 4, 2017. Performance is at net asset value.

7 Commenced operations and performance for the Class began on June 30, 2015. Performance is at net asset value.

16

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments (these charges vary among the share classes); and (2) ongoing costs, including management fees; distribution and service (12b-1) fees (these charges vary among the share classes); and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in each Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (June 1, 2022 through November 30, 2022).

Actual Expenses

For each class of each Fund, the first line of the applicable table on the following pages provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading titled “Expenses Paid During Period 6/1/22 – 11/30/22” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

For each class of each Fund, the second line of the applicable table on the following pages provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

17

Dividend Growth Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value |

Ending Account Value |

Expenses Paid During Period† |

|||||||||||

| 6/1/22 | 11/30/22 | 6/1/22 – 11/30/22 |

|||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,037.90 | $4.70 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.46 | $4.66 | ||||||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,033.90 | $8.51 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,016.70 | $8.44 | ||||||||

| Class F | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,039.50 | $3.43 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,021.71 | $3.40 | ||||||||

| Class F3 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,039.80 | $3.07 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,022.06 | $3.04 | ||||||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,039.40 | $3.43 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,021.71 | $3.40 | ||||||||

| Class P | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,037.00 | $5.72 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.45 | $5.67 | ||||||||

| Class R2 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,035.80 | $6.48 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,018.70 | $6.43 | ||||||||

| Class R3 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,036.80 | $5.97 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.20 | $5.92 | ||||||||

| Class R4 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,038.00 | $4.70 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.46 | $4.66 | ||||||||

| Class R5 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,039.40 | $3.43 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,021.71 | $3.40 | ||||||||

| Class R6 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,039.80 | $3.07 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,022.06 | $3.04 | ||||||||

† For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (0.92% for Class A, 1.67% for Class C, 0.67% for Class F, 0.60% for Class F3, 0.67% for Class I, 1.12% for Class P, 1.27% for Class R2, 1.17% for Class R3, 0.92% for Class R4, 0.67% for Class R5 and 0.60% for Class R6) multiplied by the average account value over the period, multiplied by 183/365 (to reflect one-half year period).

18

Portfolio Holdings Presented by Sector

November 30, 2022

| Sector* | %** | |||

| Consumer Discretionary | 9.22 | % | ||

| Consumer Staples | 7.42 | % | ||

| Energy | 4.86 | % | ||

| Financials | 16.37 | % | ||

| Health Care | 14.55 | % | ||

| Industrials | 11.29 | % | ||

| Information Technology | 22.88 | % | ||

| Materials | 6.22 | % | ||

| Real Estate | 2.49 | % | ||

| Utilities | 3.44 | % | ||

| Repurchase Agreements | 1.26 | % | ||

| Total | 100.00 | % | ||

| * | A sector may comprise several industries. | |

| ** | Represents percent of total investments, which excludes derivatives. |

19

Growth Opportunities Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value |

Ending Account Value |

Expenses Paid During Period† |

|||||||||||

| 6/1/22 | 11/30/22 | 6/1/22 – 11/30/22 |

|||||||||||

| Class A* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,004.20 | $5.12 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.95 | $5.16 | ||||||||

| Class C* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,000.90 | $8.88 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,016.19 | $8.95 | ||||||||

| Class F* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,005.40 | $4.42 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.66 | $4.46 | ||||||||

| Class F3* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,006.00 | $3.47 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,021.61 | $3.50 | ||||||||

| Class I* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,005.60 | $4.02 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,021.06 | $4.05 | ||||||||

| Class P* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,003.90 | $6.13 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,018.95 | $6.17 | ||||||||

| Class R2* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,002.90 | $6.88 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,018.20 | $6.93 | ||||||||

| Class R3* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,003.40 | $6.38 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,018.70 | $6.43 | ||||||||

| Class R4 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,004.80 | $5.13 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.95 | $5.16 | ||||||||

| Class R5* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,005.60 | $3.87 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,021.21 | $3.90 | ||||||||

| Class R6* | |||||||||||||

| Actual | $ | 1,000.00 | $ | 1,006.40 | $3.47 | ||||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,021.61 | $3.50 | ||||||||

† For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (1.02% for Class A, 1.77% for Class C, 0.88% for Class F, 0.69% for Class F3, 0.80% for Class I, 1.22% for Class P, 1.37% for Class R2, 1.27% for Class R3, 1.02% for Class R4, 0.77% for Class R5 and 0.69% for Class R6) multiplied by the average account value over the period, multiplied by 183/365 (to reflect one-half year period).

* The annualized expense ratios have been updated to 0.96% for Class A, 1.71% for Class C, 0.81% for Class F, 0.63% for Class F3, 0.71% for class I, 1.16% for Class P, 1.31% for Class R2, 1.21% for Class R3, 0.96% for Class R4, 0.71% for Class R5, and 0.63% for Class R6. Had these updated expense ratios been in place throughout the most recent fiscal half-year, expenses paid during the period would have been:

20

| Actual | Hypothetical (5% Return Before Expenses) | |||

| Class A | $4.82 | $4.86 | ||

| Class C | $8.58 | $8.64 | ||

| Class F | $4.07 | $4.10 | ||

| Class F3 | $3.17 | $3.19 | ||

| Class I | $3.57 | $3.60 | ||

| Class P | $5.83 | $5.87 | ||

| Class R2 | $6.59 | $6.63 | ||

| Class R3 | $6.08 | $6.12 | ||

| Class R4 | $4.83 | $4.86 | ||

| Class R5 | $3.57 | $3.60 | ||

| Class R6 | $3.17 | $3.19 |

21

Portfolio Holdings Presented by Sector

November 30, 2022

| Sector* | %** | |||

| Communication Services | 1.55 | % | ||

| Consumer Discretionary | 20.81 | % | ||

| Consumer Staples | 1.30 | % | ||

| Energy | 2.84 | % | ||

| Financials | 1.92 | % | ||

| Health Care | 19.63 | % | ||

| Industrials | 13.12 | % | ||

| Information Technology | 35.03 | % | ||

| Materials | 1.20 | % | ||

| Real Estate | 1.11 | % | ||

| Repurchase Agreements | 0.85 | % | ||

| Money Market Funds(a) | 0.58 | % | ||

| Time Deposits(a) | 0.06 | % | ||

| Total | 100.00 | % | ||

| * | A sector may comprise several industries. | |

| ** | Represents percent of total investments, which excludes derivatives. | |

| (a) | Securities were purchased with the cash collateral from loaned securities. |

22

Small Cap Value Fund

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads). Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value |

Ending Account Value |

Expenses Paid During Period† |

|||||||||||

| 6/1/22 | 11/30/22 | 6/1/22 – 11/30/22 |

|||||||||||

| Class A | |||||||||||||

| Actual | $ | 1,000.00 | $ | 986.90 | $ | 6.13 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,018.90 | $ | 6.23 | |||||||

| Class C | |||||||||||||

| Actual | $ | 1,000.00 | $ | 982.10 | $ | 9.84 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,015.14 | $ | 10.00 | |||||||

| Class F | |||||||||||||

| Actual | $ | 1,000.00 | $ | 987.80 | $ | 5.38 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.65 | $ | 5.47 | |||||||

| Class F3 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 988.60 | $ | 4.44 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.61 | $ | 4.51 | |||||||

| Class I | |||||||||||||

| Actual | $ | 1,000.00 | $ | 987.90 | $ | 4.88 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.16 | $ | 4.96 | |||||||

| Class P | |||||||||||||

| Actual | $ | 1,000.00 | $ | 985.60 | $ | 7.12 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,017.90 | $ | 7.23 | |||||||

| Class R2 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 985.30 | $ | 7.86 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,017.15 | $ | 7.99 | |||||||

| Class R3 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 985.70 | $ | 7.37 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,017.65 | $ | 7.49 | |||||||

| Class R4 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 986.90 | $ | 6.08 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,018.95 | $ | 6.17 | |||||||

| Class R5 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 987.90 | $ | 4.88 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.16 | $ | 4.96 | |||||||

| Class R6 | |||||||||||||

| Actual | $ | 1,000.00 | $ | 989.10 | $ | 4.44 | |||||||

| Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.61 | $ | 4.51 | |||||||

† For each class of the Fund, net expenses are equal to the annualized expense ratio for such class (1.23% for Class A, 1.98% for Class C, 1.08% for Class F, 0.89% for Class F3, 0.98% for Class I, 1.43% for Class P, 1.58% for Class R2, 1.48% for Class R3, 1.22% for Class R4, 0.98% for Class R5 and 0.89% for Class R6) multiplied by the average account value over the period, multiplied by 183/365 (to reflect one-half year period).

23

Portfolio Holdings Presented by Sector

November 30, 2022

| Sector* | %** | |||

| Communication Services | 4.90 | % | ||

| Consumer Discretionary | 7.63 | % | ||

| Consumer Staples | 6.31 | % | ||

| Energy | 6.72 | % | ||

| Financials | 23.97 | % | ||

| Health Care | 5.65 | % | ||

| Industrials | 20.09 | % | ||

| Information Technology | 9.02 | % | ||

| Materials | 6.44 | % | ||

| Real Estate | 5.86 | % | ||

| Utilities | 2.31 | % | ||

| Repurchase Agreements | 0.81 | % | ||

| Money Market Funds(a) | 0.26 | % | ||

| Time Deposits(a) | 0.03 | % | ||

| Total | 100.00 | % | ||

| * | A sector may comprise several industries. | |

| ** | Represents percent of total investments, which excludes derivatives. | |

| (a) | Securities were purchased with the cash collateral from loaned securities. |

24

DIVIDEND GROWTH FUND November 30, 2022

| Investments | Shares | Fair Value | ||||||

| LONG-TERM INVESTMENTS 98.55% | ||||||||

| COMMON STOCKS 98.55% | ||||||||

| Aerospace & Defense 4.37% | ||||||||

| Northrop Grumman Corp. | 141,100 | $ | 75,247,219 | |||||

| Raytheon Technologies Corp. | 875,141 | 86,393,920 | ||||||

| Total | 161,641,139 | |||||||

| Banks 3.69% | ||||||||

| Bank of America Corp. 3,601,334 | 136,310,492 | |||||||

| Beverages 2.73% | ||||||||

| Coca-Cola Co. (The) | 1,589,379 | 101,100,398 | ||||||

| Biotechnology 2.42% | ||||||||

| AbbVie, Inc. | 554,807 | 89,423,792 | ||||||

| Capital Markets 7.16% | ||||||||

| Ameriprise Financial, Inc. | 290,600 | 96,464,670 | ||||||

| Morgan Stanley | 1,038,500 | 96,653,195 | ||||||

| S&P Global, Inc. | 203,800 | 71,900,640 | ||||||

| Total | 265,018,505 | |||||||

| Chemicals 2.10% | ||||||||

| Air Products & Chemicals, Inc. | 250,400 | 77,664,064 | ||||||

| Construction Materials 1.98% | ||||||||

| Vulcan Materials Co. | 398,605 | 73,076,255 | ||||||

| Containers & Packaging 1.23% | ||||||||

| Avery Dennison Corp. | 234,452 | 45,326,605 | ||||||

| Electric: Utilities 3.04% | ||||||||

| NextEra Energy, Inc. | 1,326,049 | 112,316,350 | ||||||

| Equity Real Estate Investment Trusts 2.49% | ||||||||

| American Tower Corp. | 319,800 | 70,755,750 | ||||||

| Prologis, Inc. | 180,351 | 21,243,544 | ||||||

| Total | 91,999,294 | |||||||

| Investments | Shares | Fair Value | ||||||

| Food & Staples Retailing 4.17% | ||||||||

| Costco Wholesale Corp. | 140,028 | $ | 75,510,099 | |||||

| Walmart, Inc. | 516,770 | 78,766,083 | ||||||

| Total | 154,276,182 | |||||||

| Health Care Equipment & Supplies 1.77% | ||||||||

| Abbott Laboratories | 610,200 | 65,645,316 | ||||||

| Health Care Providers & Services 4.66% | ||||||||

| Humana, Inc. | 74,756 | 41,108,324 | ||||||

| UnitedHealth Group, Inc. | 239,700 | 131,298,072 | ||||||

| Total | 172,406,396 | |||||||

| Hotels, Restaurants & Leisure 3.01% | ||||||||

| Churchill Downs, Inc. | 131,635 | 29,217,705 | ||||||

| McDonald’s Corp. | 169,726 | 46,299,555 | ||||||

| Starbucks Corp. | 350,848 | 35,856,666 | ||||||

| Total | 111,373,926 | |||||||

| Industrial Conglomerates 2.27% | ||||||||

| Honeywell International, Inc. | 383,100 | 84,109,605 | ||||||

| Information Technology Services 5.79% | ||||||||

| Accenture plc Class A (Ireland)(a) | 158,500 | 47,697,405 | ||||||

| Jack Henry & Associates, Inc. | 260,000 | 49,231,000 | ||||||

| Mastercard, Inc. Class A | 328,659 | 117,134,068 | ||||||

| Total | 214,062,473 | |||||||

| Insurance 5.49% | ||||||||

| Allstate Corp. (The) | 516,967 | 69,221,881 | ||||||

| American Financial Group, Inc./OH | 225,300 | 32,042,166 | ||||||

| Arthur J Gallagher & Co. | 294,753 | 58,688,270 | ||||||

| Chubb Ltd. (Switzerland)(a) | 196,900 | 43,237,271 | ||||||

| Total | 203,189,588 | |||||||

| See Notes to Financial Statements. | 25 |

Schedule of Investments (continued)

DIVIDEND GROWTH FUND November 30, 2022

| Investments | Shares | Fair Value | ||||||

| Life Sciences Tools & Services 2.63% | ||||||||

| Danaher Corp. | 252,400 | $ | 69,008,684 | |||||

| West Pharmaceutical Services, Inc. | 120,200 | 28,206,132 | ||||||

| Total | 97,214,816 | |||||||

| Machinery 2.11% | ||||||||

| Parker-Hannifin Corp. | 260,891 | 77,990,756 | ||||||

| Metals & Mining 0.91% | ||||||||

| Reliance Steel & Aluminum Co. | 158,700 | 33,531,723 | ||||||

| Multi-Utilities 0.39% | ||||||||

| CMS Energy Corp. | 239,100 | 14,601,837 | ||||||

| Oil, Gas & Consumable Fuels 4.85% | ||||||||

| Exxon Mobil Corp. | 1,161,830 | 129,358,152 | ||||||

| Marathon Petroleum Corp. | 411,100 | 50,076,091 | ||||||

| Total | 179,434,243 | |||||||

| Personal Products 0.50% | ||||||||

| Estee Lauder Cos., Inc. (The) Class A | 78,419 | 18,490,416 | ||||||

| Pharmaceuticals 3.04% | ||||||||

| Eli Lilly & Co. | 200,432 | 74,376,307 | ||||||

| Zoetis, Inc. | 247,900 | 38,211,306 | ||||||

| Total | 112,587,613 | |||||||

| Professional Services 0.81% | ||||||||

| Booz Allen Hamilton Holding Corp. | 282,727 | 30,082,153 | ||||||

| Road & Rail 1.70% | ||||||||

| Union Pacific Corp. | 289,600 | 62,967,728 | ||||||

| Semiconductors & Semiconductor Equipment 4.58% | ||||||||

| Analog Devices, Inc. | 293,400 | 50,438,394 | ||||||

| KLA Corp. | 89,700 | 35,265,555 | ||||||

| NVIDIA Corp. | 152,900 | 25,875,267 | ||||||

| Texas Instruments, Inc. | 320,800 | 57,891,568 | ||||||

| Total | 169,470,784 | |||||||

| Investments | Shares | Fair Value | ||||||

| Software 9.51% | ||||||||

| Intuit, Inc. | 91,000 | $ | 37,090,690 | |||||

| Microsoft Corp. | 971,200 | 247,791,968 | ||||||

| Roper Technologies, Inc. | 152,284 | 66,835,925 | ||||||

| Total | 351,718,583 | |||||||

| Specialty Retail 5.42% | ||||||||

| Home Depot, Inc. (The) | 185,600 | 60,132,544 | ||||||

| Lowe’s Cos., Inc. | 369,375 | 78,510,656 | ||||||

| TJX Cos., Inc. (The) | 774,900 | 62,030,745 | ||||||

| Total | 200,673,945 | |||||||

| Technology Hardware, Storage & Peripherals 2.96% | ||||||||

| Apple, Inc. | 740,003 | 109,542,644 | ||||||

| Textiles, Apparel & Luxury Goods 0.77% | ||||||||

| NIKE, Inc. Class B | 259,900 | 28,508,431 | ||||||

| Total Common Stocks (cost $3,003,430,736) | 3,645,756,052 | |||||||

| Principal Amount | ||||||||

| SHORT-TERM INVESTMENTS 1.26% | ||||||||

| Repurchase Agreements 1.26% | ||||||||

| Repurchase Agreement dated 11/30/2022, 1.75% due 12/1/2022 with Fixed Income Clearing Corp. collateralized by $49,320,100, of U.S. Treasury Note at 2.00% due 5/31/2024; value: $47,391,585; proceeds: $46,464,591 (cost $46,462,332) | $ | 46,462,332 | 46,462,332 | |||||

| Total Investments in Securities 99.81% (cost $3,049,893,068) | 3,692,218,384 | |||||||

| Other Assets and Liabilities – Net(b) 0.19% | 7,099,025 | |||||||

| Net Assets 100.00% | $ | 3,699,317,409 | ||||||

| (a) | Foreign security traded in U.S. dollars. | |

| (b) | Other Assets and Liabilities include net unrealized appreciation/depreciation on futures contracts as follows: |

| 26 | See Notes to Financial Statements. |

Schedule of Investments (concluded)

DIVIDEND GROWTH FUND November 30, 2022

Futures Contracts at November 30, 2022:

| Type | Expiration | Contracts | Position | Notional Amount | Notional Value | Unrealized Appreciation | ||||||||||||

| E-Mini S&P 500 Index | December 2022 | 185 | Long | $36,013,386 | $37,751,562 | $1,738,176 | ||||||||||||

The following is a summary of the inputs used as of November 30, 2022 in valuing the Fund’s investments carried at fair value(1):

| Investment Type(2) | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Long-Term Investments | ||||||||||||||||

| Common Stocks | $ | 3,645,756,052 | $ | – | $ | – | $ | 3,645,756,052 | ||||||||

| Short-Term Investments | ||||||||||||||||

| Repurchase Agreements | – | 46,462,332 | – | 46,462,332 | ||||||||||||

| Total | $ | 3,645,756,052 | $ | 46,462,332 | $ | – | $ | 3,692,218,384 | ||||||||

| Other Financial Instruments | ||||||||||||||||

| Futures Contracts | ||||||||||||||||

| Assets | $ | 1,738,176 | $ | – | $ | – | $ | 1,738,176 | ||||||||

| Liabilities | – | – | – | – | ||||||||||||

| Total | $ | 1,738,176 | $ | – | $ | – | $ | 1,738,176 | ||||||||

| (1) | Refer to Note 2(i) for a description of fair value measurements and the three-tier hierarchy of inputs. | |

| (2) | See Schedule of Investments for fair values in each industry and identification of foreign issuers and/or geography. When applicable each Level 3 security is identified on the Schedule of Investments along with the valuation technique utilized. |

A reconciliation of Level 3 investments is presented when the Fund has a material amount of Level 3 investments at the beginning or end of the year in relation to the Fund’s net assets.

| See Notes to Financial Statements. | 27 |

Schedule of Investments

GROWTH OPPORTUNITIES FUND November 30, 2022

| Investments | Shares | Fair Value | ||||||

| LONG-TERM INVESTMENTS 99.08% | ||||||||

| COMMON STOCKS 99.08% | ||||||||

| Aerospace & Defense 4.30% | ||||||||

| Axon Enterprise, Inc.* | 49,850 | $ | 9,173,896 | |||||

| Parsons Corp.* | 77,254 | 3,824,073 | ||||||

| TransDigm Group, Inc. | 11,898 | 7,477,893 | ||||||

| Total | 20,475,862 | |||||||

| Beverages 1.31% | ||||||||

| Brown-Forman Corp. Class B | 33,458 | 2,443,103 | ||||||

| Celsius Holdings, Inc.* | 34,044 | 3,790,459 | ||||||

| Total | 6,233,562 | |||||||

| Biotechnology 9.17% | ||||||||

| Alnylam Pharmaceuticals, Inc.* | 21,264 | 4,690,626 | ||||||

| Argenx SE ADR* | 22,172 | 8,823,791 | ||||||

| Biogen, Inc.* | 12,704 | 3,876,880 | ||||||

| Cytokinetics, Inc.* | 141,144 | 5,998,620 | ||||||

| Genmab A/S ADR* | 105,821 | 4,923,851 | ||||||

| Karuna Therapeutics, Inc.* | 26,827 | 6,312,661 | ||||||

| Krystal Biotech, Inc.* | 46,698 | 3,630,302 | ||||||

| Sarepta Therapeutics, Inc.* | 44,147 | 5,421,693 | ||||||

| Total | 43,678,424 | |||||||

| Capital Markets 1.93% | ||||||||

| MSCI, Inc. | 10,459 | 5,311,394 | ||||||

| Raymond James Financial, Inc. | 33,412 | 3,905,863 | ||||||

| Total | 9,217,257 | |||||||

| Chemicals 1.21% | ||||||||

| Albemarle Corp. | 20,748 | 5,767,737 | ||||||

| Communications Equipment 4.28% | ||||||||

| Arista Networks, Inc.* | 74,850 | 10,426,605 | ||||||

| Calix, Inc.* | 139,486 | 9,945,352 | ||||||

| Total | 20,371,957 | |||||||

| Investments | Shares | Fair Value | ||||||

| Construction & Engineering 2.69% | ||||||||

| Comfort Systems USA, Inc. | 41,303 | $ | 5,235,568 | |||||

| Quanta Services, Inc. | 50,570 | 7,579,432 | ||||||

| Total | 12,815,000 | |||||||

| Electrical Equipment 2.35% | ||||||||

| AMETEK, Inc. | 52,611 | 7,492,859 | ||||||

| Hubbell, Inc. | 14,509 | 3,686,156 | ||||||

| Total | 11,179,015 | |||||||

| Entertainment 0.74% | ||||||||

| World Wrestling Entertainment, Inc. Class A | 43,873 | 3,504,575 | ||||||

| Equity Real Estate Investment Trusts 1.12% | ||||||||

| SBA Communications Corp. | 17,848 | 5,341,906 | ||||||

| Health Care Equipment & Supplies 7.89% | ||||||||

| Axonics, Inc.* | 48,035 | 3,289,437 | ||||||

| DexCom, Inc.* | 91,990 | 10,696,597 | ||||||

| IDEXX Laboratories, Inc.* | 5,862 | 2,496,450 | ||||||

| Inspire Medical Systems, Inc.* | 12,043 | 2,909,227 | ||||||

| Insulet Corp.* | 39,130 | 11,714,348 | ||||||

| Lantheus Holdings, Inc.* | 60,045 | 3,727,594 | ||||||

| Shockwave Medical, Inc.* | 10,852 | 2,752,067 | ||||||

| Total | 37,585,720 | |||||||

| Hotels, Restaurants & Leisure 6.04% | ||||||||

| Chipotle Mexican Grill, Inc.* | 7,783 | 12,662,630 | ||||||

| Hilton Worldwide Holdings, Inc. | 42,174 | 6,014,856 | ||||||

| Planet Fitness, Inc. Class A* | 75,139 | 5,887,892 | ||||||

| Wingstop, Inc. | 25,344 | 4,194,685 | ||||||

| Total | 28,760,063 | |||||||

| 28 | See Notes to Financial Statements. |

Schedule of Investments (continued)

GROWTH OPPORTUNITIES FUND November 30, 2022

| Investments | Shares | Fair Value | ||||||

| Information Technology Services 4.83% | ||||||||

| Block, Inc.* | 65,030 | $ | 4,407,083 | |||||

| Cloudflare, Inc. Class A* | 76,120 | 3,740,537 | ||||||

| Shopify, Inc. Class A (Canada)*(a) | 236,312 | 9,660,435 | ||||||

| Toast, Inc. Class A* | 284,428 | 5,222,098 | ||||||

| Total | 23,030,153 | |||||||

| Internet & Direct Marketing Retail 4.74% | ||||||||

| Coupang, Inc. (South Korea)*(a) | 403,505 | 7,860,278 | ||||||

| Etsy, Inc.* | 46,343 | 6,121,447 | ||||||

| MercadoLibre, Inc. (Uruguay)*(a) | 9,241 | 8,603,232 | ||||||

| Total | 22,584,957 | |||||||

| Life Sciences Tools & Services 1.68% | ||||||||

| Agilent Technologies, Inc. | 37,349 | 5,788,348 | ||||||

| Repligen Corp.* | 12,479 | 2,231,744 | ||||||

| Total | 8,020,092 | |||||||

| Machinery 1.40% | ||||||||

| Fortive Corp. | 60,607 | 4,094,003 | ||||||

| Xylem, Inc. | 22,863 | 2,568,658 | ||||||

| Total | 6,662,661 | |||||||

| Oil, Gas & Consumable Fuels 2.85% | ||||||||

| Antero Resources Corp.* | 64,418 | 2,354,478 | ||||||

| Cheniere Energy, Inc. | 50,415 | 8,840,774 | ||||||

| EQT Corp. | 56,624 | 2,401,424 | ||||||

| Total | 13,596,676 | |||||||

| Pharmaceuticals 1.00% | ||||||||

| Intra-Cellular Therapies, Inc.* | 87,707 | 4,755,474 | ||||||

| Professional Services 1.72% | ||||||||

| Booz Allen Hamilton Holding Corp. | 32,114 | 3,416,930 | ||||||

| CoStar Group, Inc.* | 59,053 | 4,785,655 | ||||||

| Total | 8,202,585 | |||||||

| Investments | Shares | Fair Value | ||||||

| Semiconductors & Semiconductor Equipment 12.14% | ||||||||

| Enphase Energy, Inc.* | 43,924 | $ | 14,081,595 | |||||

| First Solar, Inc.* | 20,726 | 3,575,857 | ||||||

| GLOBALFOUNDRIES, Inc.*(b) | 51,660 | 3,324,321 | ||||||

| KLA Corp. | 12,248 | 4,815,301 | ||||||

| Lattice Semiconductor Corp.* | 108,089 | 7,872,122 | ||||||

| Monolithic Power Systems, Inc. | 17,770 | 6,787,429 | ||||||

| ON Semiconductor Corp.* | 80,953 | 6,087,666 | ||||||

| Rambus, Inc.* | 136,934 | 5,255,527 | ||||||

| SolarEdge Technologies, Inc. (Israel)*(a) | 11,248 | 3,361,577 | ||||||

| Wolfspeed, Inc.* | 29,227 | 2,657,319 | ||||||

| Total | 57,818,714 | |||||||

| Software 13.49% | ||||||||

| Aspen Technology, Inc.* | 23,713 | 5,465,846 | ||||||

| Bentley Systems, Inc. Class B | 88,949 | 3,523,270 | ||||||

| Bill.com Holdings, Inc.* | 28,150 | 3,389,823 | ||||||

| Cadence Design Systems, Inc.* | 15,341 | 2,639,266 | ||||||

| Clear Secure, Inc. Class A | 231,652 | 7,199,744 | ||||||

| Crowdstrike Holdings, Inc. Class A* | 40,701 | 4,788,473 | ||||||

| CyberArk Software Ltd. (Israel)*(a) | 28,425 | 4,237,315 | ||||||

| Datadog, Inc. Class A* | 30,596 | 2,318,565 | ||||||

| DoubleVerify Holdings, Inc.* | 149,813 | 3,925,100 | ||||||

| Gitlab, Inc. Class A* | 55,447 | 2,192,929 | ||||||

| Palo Alto Networks, Inc.* | 15,167 | 2,576,873 | ||||||

| Paycom Software, Inc.* | 17,848 | 6,052,257 | ||||||

| Paylocity Holding Corp.* | 15,847 | 3,451,952 | ||||||

| Roper Technologies, Inc. | 8,925 | 3,917,093 | ||||||

| See Notes to Financial Statements. | 29 |

Schedule of Investments (continued)

GROWTH OPPORTUNITIES FUND November 30, 2022

| Investments | Shares | Fair Value | ||||||

| Software (continued) | ||||||||

| Synopsys, Inc.* | 7,731 | $ | 2,624,984 | |||||

| Trade Desk, Inc. (The) Class A* | 74,862 | 3,903,305 | ||||||

| Zscaler, Inc.* | 15,260 | 2,036,447 | ||||||

| Total | 64,243,242 | |||||||

| Specialty Retail 3.15% | ||||||||

| Dick’s Sporting Goods, Inc. | 33,702 | 4,030,085 | ||||||

| Tractor Supply Co. | 22,145 | 5,011,635 | ||||||

| Ulta Beauty, Inc.* | 12,880 | 5,987,139 | ||||||

| Total | 15,028,859 | |||||||

| Technology Hardware, Storage & Peripherals 1.32% | ||||||||

| Pure Storage, Inc. Class A* | 215,776 | 6,298,501 | ||||||

| Textiles, Apparel & Luxury Goods 6.99% | ||||||||

| Crocs, Inc.* | 112,453 | 11,357,753 | ||||||

| Deckers Outdoor Corp.* | 19,832 | 7,910,588 | ||||||

| Lululemon Athletica, Inc. (Canada)*(a) | 36,923 | 14,042,186 | ||||||

| Total | 33,310,527 | |||||||

| Trading Companies & Distributors 0.74% | ||||||||

| WW Grainger, Inc. | 5,844 | 3,524,283 | ||||||

| Total Common Stocks (cost $392,695,204) | 472,007,802 | |||||||

| Investments | Principal Amount | Fair Value | ||||||

| SHORT-TERM INVESTMENTS 1.49% | ||||||||

| Repurchase Agreements 0.85% | ||||||||

| Repurchase Agreement dated 11/30/2022, 1.75% due 12/1/2022 with Fixed Income Clearing Corp. collateralized by $4,414,700, of U.S. Treasury Note at 0.25% due 6/15/2024; value: $4,129,707; proceeds: $4,048,900 (cost $4,048,703) | $ | 4,048,703 | $ | 4,048,703 | ||||

| Shares | ||||||||

| Money Market Funds 0.58% | ||||||||

| Fidelity Government Portfolio(c) (cost $2,767,050) | 2,767,050 | 2,767,050 | ||||||

| Time Deposits 0.06% | ||||||||

| CitiBank N.A.(c) (cost $307,450) | 307,450 | 307,450 | ||||||

| Total Short-Term Investments (cost $7,123,203) | 7,123,203 | |||||||

| Total Investments in Securities 100.57% (cost $399,818,407) | 479,131,005 | |||||||

| Other Assets and Liabilities – Net (0.57)% | (2,729,998 | ) | ||||||

| Net Assets 100.00% | $ | 476,401,007 | ||||||

| ADR | American Depositary Receipt. | |

| * | Non-income producing security. | |

| (a) | Foreign security traded in U.S. dollars. | |

| (b) | All or a portion of this security is temporarily on loan to unaffiliated broker/dealers. | |

| (c) | Security was purchased with the cash collateral from loaned securities. |

| 30 | See Notes to Financial Statements. |

Schedule of Investments (concluded)

GROWTH OPPORTUNITIES FUND November 30, 2022

The following is a summary of the inputs used as of November 30, 2022 in valuing the Fund’s investments carried at fair value(1):

| Investment Type(2) | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Long-Term Investments | ||||||||||||||||

| Common Stocks | $ | 472,007,802 | $ | – | $ | – | $ | 472,007,802 | ||||||||

| Short-Term Investments | ||||||||||||||||

| Repurchase Agreements | – | 4,048,703 | – | 4,048,703 | ||||||||||||

| Money Market Funds | 2,767,050 | – | – | 2,767,050 | ||||||||||||

| Time Deposits | – | 307,450 | – | 307,450 | ||||||||||||

| Total | $ | 474,774,852 | $ | 4,356,153 | $ | – | $ | 479,131,005 | ||||||||

| (1) | Refer to Note 2(i) for a description of fair value measurements and the three-tier hierarchy of inputs. | |

| (2) | See Schedule of Investments for fair values in each industry and identification of foreign issuers and/or geography. When applicable each Level 3 security is identified on the Schedule of Investments along with the valuation technique utilized. |

A reconciliation of Level 3 investments is presented when the Fund has a material amount of Level 3 investments at the beginning or end of the year in relation to the Fund’s net assets.

| See Notes to Financial Statements. | 31 |

Schedule of Investments

SMALL CAP VALUE FUND November 30, 2022

| Investments | Shares | Fair Value | ||||||

| LONG-TERM INVESTMENTS 99.20% | ||||||||

| COMMON STOCKS 99.20% | ||||||||

| Aerospace & Defense 2.00% | ||||||||

| Curtiss-Wright Corp. | 46,221 | $ | 8,164,940 | |||||

| Auto Components 1.86% | ||||||||

| Dorman Products, Inc.* | 45,505 | 4,079,068 | ||||||

| Gentherm, Inc.* | 49,267 | 3,527,025 | ||||||

| Total | 7,606,093 | |||||||

| Banks 11.91% | ||||||||

| Bancorp, Inc. (The)* | 171,667 | 5,144,860 | ||||||

| Eastern Bankshares, Inc. | 214,867 | 4,213,542 | ||||||

| First BanCorp | 677,245 | 10,416,012 | ||||||

| Heritage Financial Corp. | 243,292 | 8,004,307 | ||||||

| Prosperity Bancshares, Inc. | 85,184 | 6,437,355 | ||||||

| SouthState Corp. | 78,479 | 6,894,380 | ||||||

| Wintrust Financial Corp. | 82,700 | 7,561,261 | ||||||

| Total | 48,671,717 | |||||||

| Building Products 1.67% | ||||||||

| Masonite International Corp.* | 90,803 | 6,834,742 | ||||||

| Capital Markets 4.07% | ||||||||

| Bridge Investment Group Holdings, Inc. Class A | 404,071 | 6,162,083 | ||||||

| CI Financial Corp.(a) | 459,700 | 4,863,049 | ||||||

| Moelis & Co. Class A | 130,106 | 5,623,181 | ||||||

| Total | 16,648,313 | |||||||

| Chemicals 3.97% | ||||||||

| Avient Corp. | 138,289 | 4,786,182 | ||||||

| Element Solutions, Inc. | 212,497 | 4,156,442 | ||||||

| Valvoline, Inc. | 220,452 | 7,270,507 | ||||||

| Total | 16,213,131 | |||||||

| Commercial Banks 1.36% | ||||||||

| WSFS Financial Corp. | 114,710 | 5,564,582 | ||||||

| Investments | Shares | Fair Value | ||||||

| Commercial Services & Supplies 1.45% | ||||||||

| SP Plus Corp.* | 169,675 | $ | 5,919,961 | |||||

| Construction & Engineering 2.08% | ||||||||

| EMCOR Group, Inc. | 54,868 | 8,499,053 | ||||||

| Construction Materials 1.62% | ||||||||

| Eagle Materials, Inc. | 48,677 | 6,636,622 | ||||||

| Containers & Packaging 0.87% | ||||||||

| Pactiv Evergreen, Inc. | 305,990 | 3,561,724 | ||||||