Exhibit 99.2

Fourth Quarter And Full Year 2024 Earnings Supplement March 4, 2025

Important Disclosure This presentation is intended to provide general information

only and is not, and should not be considered, as an offer to purchase or sell the Company’s securities, or a proposal to receive such offers. In addition, this presentation is not an offer to the public of the Company’s securities. By

attending or viewing this presentation, each attendee (“Attendee”) agrees that he or she (i) has read this disclaimer, (ii) is bound by the restrictions set out herein, (iii) is permitted, in accordance with all applicable laws, to receive such

information, (iv) is solely responsible for his or her own assessment of the business and financial position of the Company and (v) will conduct his or her own analysis and be solely responsible for forming the Attendee's view of the potential

future performance of the Company’s business. This presentation includes projections, guidance, forecasts, estimates, assessments and other information pertaining to future events and/or matters, whose materialization is uncertain and is

beyond the Company’s control, and which constitute forward looking statements (within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Israeli

Securities Law, 5728-1968). Many of the forward-looking statements contained in this presentation can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “estimate”

and “potential,” among others. Forward-looking statements include, but are not limited to, expectations and evaluations relating to the Company’s business and financial targets and strategy, the integration of the Company’s technology in

various systems and industries, the advantages of the Company’s existing and future products, timetables regarding completion of the Company’s developments and the Company’s intentions in relation to various industries, the Company’s intentions

in relation to the creation of collaborations and engagements in licensing agreements, production and distribution in various countries, and other statements regarding our intent, belief or current expectations. Forward-looking statements are

based on our management’s beliefs and assumptions and on information currently available to our management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the

forward-looking statements due to of various factors, including, but not limited to: our expectations regarding general market conditions, including as a result of global economic trends; changes in consumer tastes and preferences; fluctuations

in inflation, interest rate and exchange rates in the global economic environment over the world; the availability of qualified personnel and the ability to retain such personnel; changes in commodity costs, labor, distribution and other

operating costs; our ability to implement our growth strategy; changes in government regulation and tax matters; other factors that may affect our financial condition, liquidity and results of operations; general economic, political,

demographic and business conditions in Israel, including ongoing military conflicts in the region; the success of operating initiatives, including advertising and promotional efforts and new product and concept development by us and our

competitors; factors relating to the acquisition of Retail Pro International ("Retail Pro"), including but not limited to the financing for and payment of the acquisition and our ability to effectively and efficiently integrate the acquired

business into our existing business; and other risk factors discussed under “Risk Factors” in our annual report on Form 20-F filed with the SEC on March 4 , 2025 (our “Annual Report"). You should not rely upon forward-looking statements as

predictions of future events. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee that future results, levels of activity, performance and events and circumstances reflected

in the forward-looking statements will be achieved or will occur. Except as required by law, we undertake no obligation to update publicly any forward-looking statements provided in this presentation for any reason, to conform these statements

to actual results or to changes in our expectations. In addition, the presentation includes data published by various bodies, and data provided to the Company in the framework of cooperation engagements, concerning the industry, competitive

position and the markets in which the Company operates, whose content was not independently verified by the Company, such that the Company is not responsible for the accuracy or completeness of such date or whether the data is up-to-date, and

Company takes no responsibility for any reliance on the data. Management estimates contained in this presentation are derived from publicly available information released by independent industry analysts and other third-party sources, as well

as data from the Company's internal research, and are based on assumptions made by the Company upon reviewing such data, and the Company's experience in, and knowledge of, such industry and markets, which the Company believes to be reasonable.

In addition, projections, assumptions and estimates of the future performance of the industry in which the Company operates and the Company's future performance are necessarily subject to uncertainty and risk due to a variety of factors,

including those described above. These and other factors could cause results to differ materially from those expressed in the estimates made by independent parties and by the Company. Industry publications, research, surveys and studies

generally state that the information they contain has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Forecasts and other forward-looking information obtained

from these sources are subject to the same qualifications and uncertainties as the other forward-looking statements in this presentation. In addition to various operational metrics and financial measures in accordance with accounting

principles generally accepted under International Financial Reporting Standards, or IFRS, this presentation contains Adjusted EBITDA, Free Cash Flow and Adjusted OPEX, all non-IFRS financial measures, as measures to evaluate our past results

and future prospects. Please refer to the Appendix for a definition of Adjusted EBITDA, Free Cash Flow and Adjusted OPEX as well as reconciliations of Adjusted EBITDA to net income (loss), Free Cash Flow to operating cash and Adjusted OPEX to

OPEX. Unless noted otherwise, the financial information of the Company included in this presentation for Q4 2023 or any later period includes figures from Retail Pro. Unless noted otherwise, the financial information of the Company included

in this presentation for the Q2 2024 or any later period includes figures from Roseman Engineering LTD, Roseman Holdings (1985) LTD and Vmtecnologia LTDA. The Company does not provide a reconciliation of forward-looking Adjusted EBITDA to IFRS

net income (loss), due to the inherent difficulty in forecasting, and quantifying certain amounts that are necessary for such reconciliation, in particular, because special items such as, finance expenses and Issuance and acquisition costs,

used to calculate projected net income (loss) vary dramatically based on actual events. Therefore, the Company is not able to forecast on an IFRS basis with reasonable certainty all deductions needed in order to provide an IFRS calculation of

projected net income (loss) at this time. The amount of these deductions may be material, and therefore could result in projected IFRS net income (loss) being materially less than projected Adjusted EBITDA (non-IFRS). The Company and its

licensors have proprietary rights to trademarks used in this Presentation. Solely for convenience, trademarks and trade names referred to in this Presentation may appear without the “®” or “™” symbols, but the lack of such references is not

intended to indicate, in any way, that the Company will not assert, to the fullest extent possible under applicable law, its rights or the rights of the applicable licensor to these trademarks and trade names. This Presentation also contains

trademarks, trade names and service marks of other companies, which are the property of their respective owners and are used for reference purposes only. Such use of other parties’ trademarks, trade names or service marks should not be

construed to imply, a relationship with, or an endorsement or sponsorship of the Company by any other party. 2

Today’s Presenters 3 Yair Nechmad CEO & Co-Founder Sagit

Manor CFO Aaron Greenberg CSO

Simplifying commerce and payments for retailers, driving growth while

optimizing operations and enhancing consumer engagement Our Mission Vending Amusement Self-Service Kiosks Laundromats Car Wash & Air Vac Kiddie Rides Food Trucks Restaurants Micro Markets EV Energy Massage Chair Parking 4

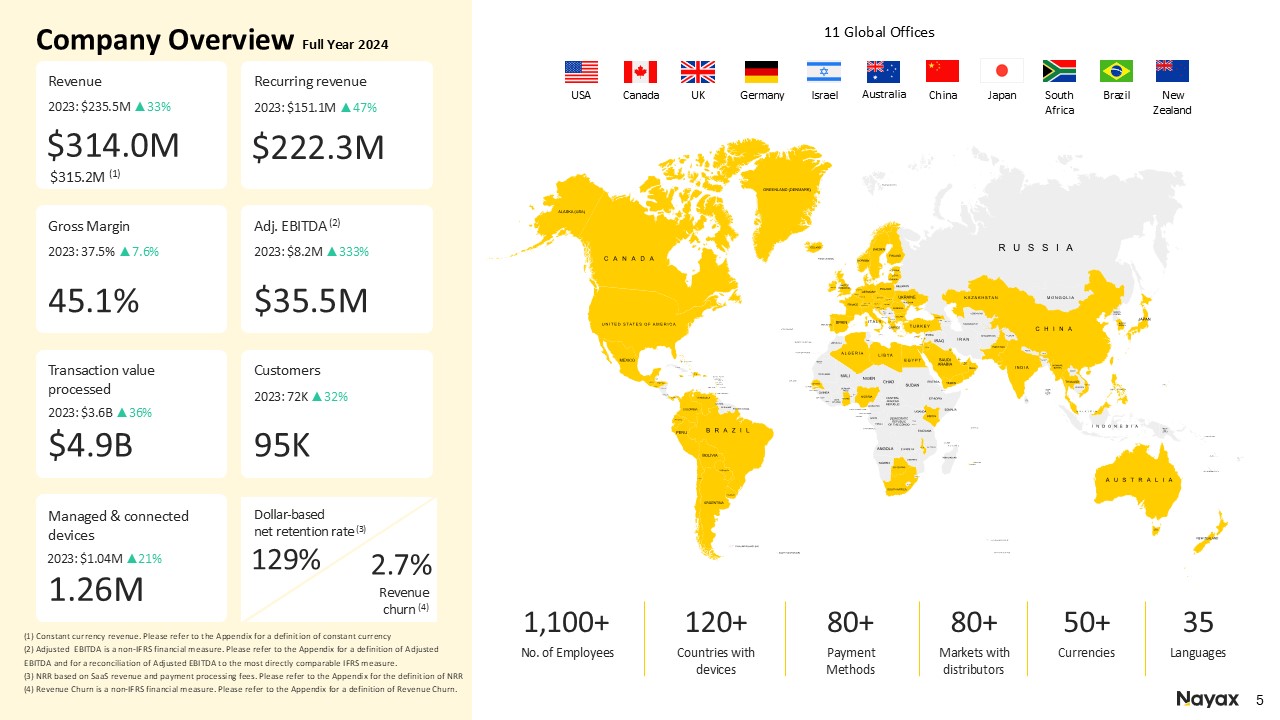

Company Overview Full Year 2024 11 Global Offices Revenue $314.0M $315.2M

(1) 2023: $235.5M ▲33% Recurring revenue $222.3M 2023: $151.1M ▲47% Gross Margin 45.1% 2023: 37.5% ▲7.6% Adj. EBITDA (2) $35.5M 2023: $8.2M ▲333% (1) Constant currency revenue. Please refer to the Appendix for a definition of

constant currency (2) Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. (3) NRR based

on SaaS revenue and payment processing fees. Please refer to the Appendix for the definition of NRR (4) Revenue Churn is a non-IFRS financial measure. Please refer to the Appendix for a definition of Revenue Churn. Transaction value

processed $4.9B Customers 95K No. of Employees 1,100+ Countries with devices 120+ Payment Methods 80+ Markets with distributors 80+ Currencies 50+ Languages 35 Managed & connected devices 1.26M Revenue churn

(4) 2.7% 2023: $3.6B ▲36% 2023: 72K ▲32% Dollar-basednet retention rate (3) 129% 2023: $1.04M ▲21% Canada USA UK Israel Germany Australia China Japan South Africa Brazil New Zealand

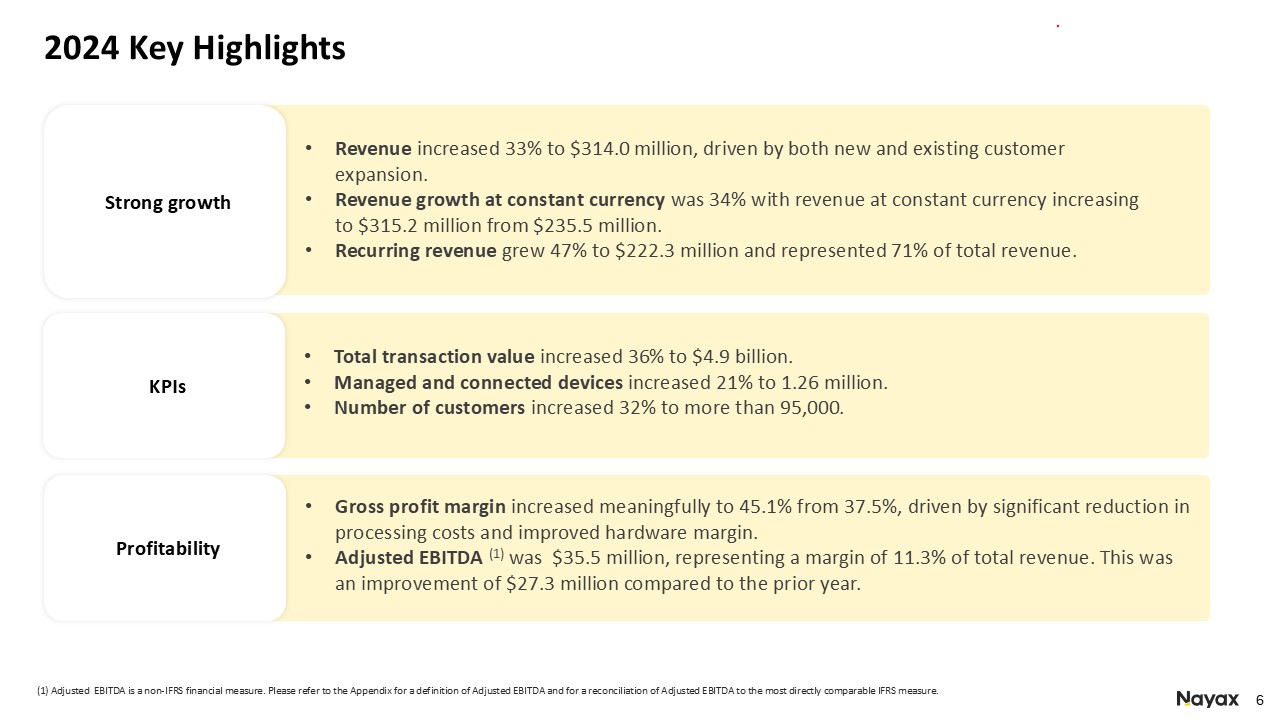

2024 Key Highlights (1) Adjusted EBITDA is a non-IFRS financial measure. Please

refer to the Appendix for a definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. Strong growth Revenue increased 33% to $314.0 million, driven by both new and existing

customer expansion. Revenue growth at constant currency was 34% with revenue at constant currency increasing to $315.2 million from $235.5 million. Recurring revenue grew 47% to $222.3 million and represented 71% of total revenue. Gross

profit margin increased meaningfully to 45.1% from 37.5%, driven by significant reduction in processing costs and improved hardware margin. Adjusted EBITDA (1) was $35.5 million, representing a margin of 11.3% of total revenue. This was an

improvement of $27.3 million compared to the prior year. Profitability Total transaction value increased 36% to $4.9 billion. Managed and connected devices increased 21% to 1.26 million. Number of customers increased 32% to more than

95,000. KPIs

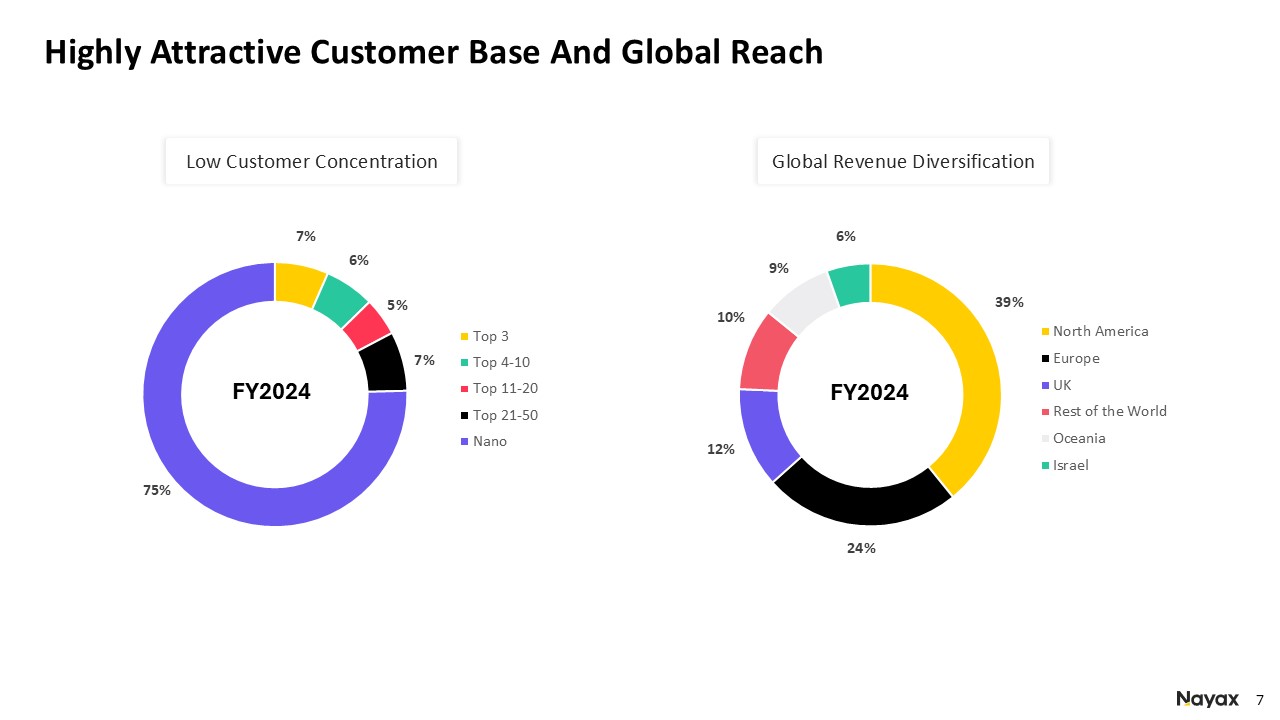

Highly Attractive Customer Base And Global Reach Low Customer

Concentration Global Revenue Diversification FY2024 FY2024

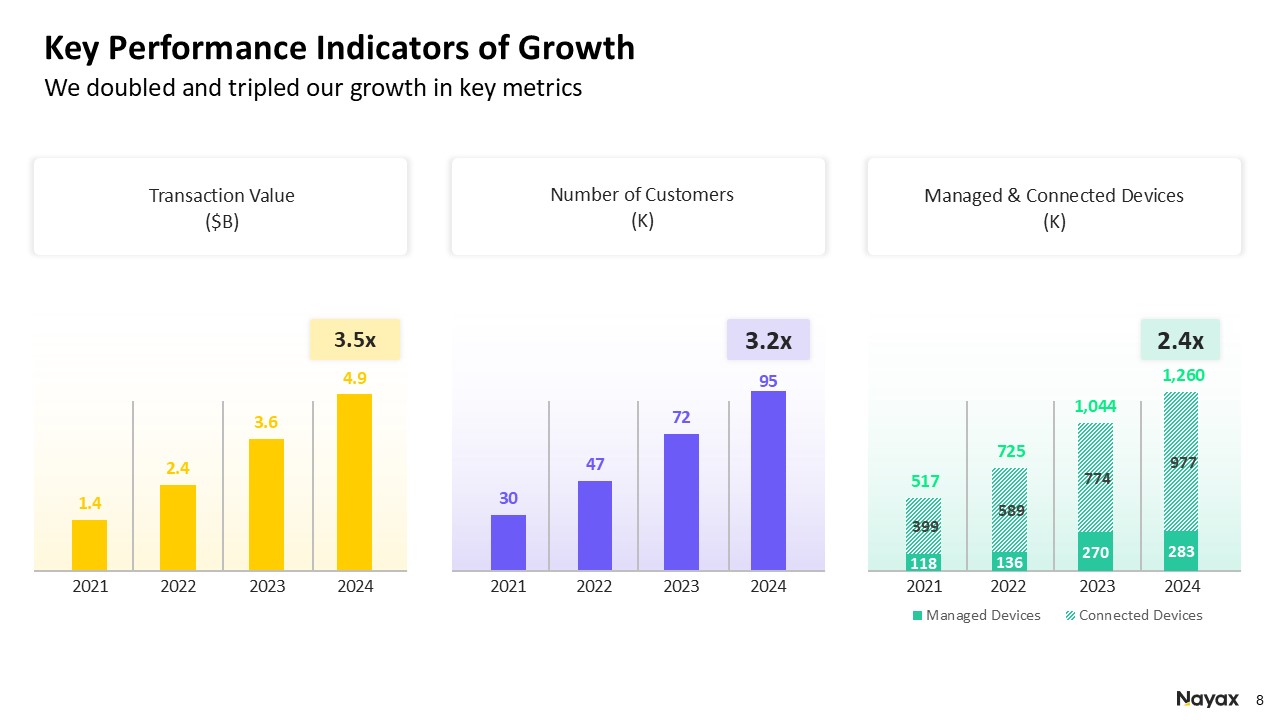

Key Performance Indicators of Growth We doubled and tripled our growth in key

metrics Transaction Value ($B) 2021 2022 2023 2024 3.5x 2021 2022 2023 2024 3.2x 2021 2022 2023 2024 2.4x Number of Customers (K) Managed & Connected Devices (K)

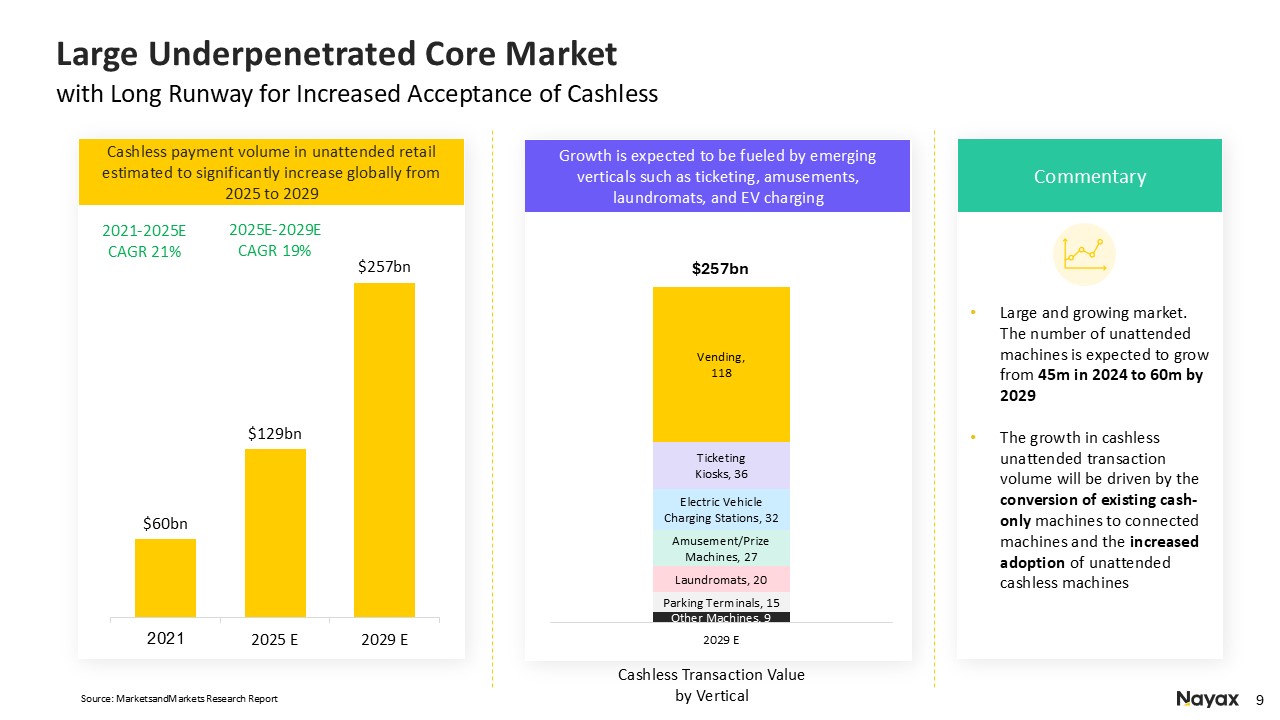

Large Underpenetrated Core Market with Long Runway for Increased Acceptance of

Cashless Source: MarketsandMarkets Research Report Growth is expected to be fueled by emerging verticals such as ticketing, amusements, laundromats, and EV charging Cashless Transaction Value by Vertical $257bn Large and growing market.

The number of unattended machines is expected to grow from 45m in 2024 to 60m by 2029 The growth in cashless unattended transaction volume will be driven by the conversion of existing cash-only machines to connected machines and the increased

adoption of unattended cashless machines Cashless payment volume in unattended retail estimated to significantly increase globally from 2025 to 2029 Commentary 2021-2025E CAGR 21% 2025E-2029E CAGR 19%

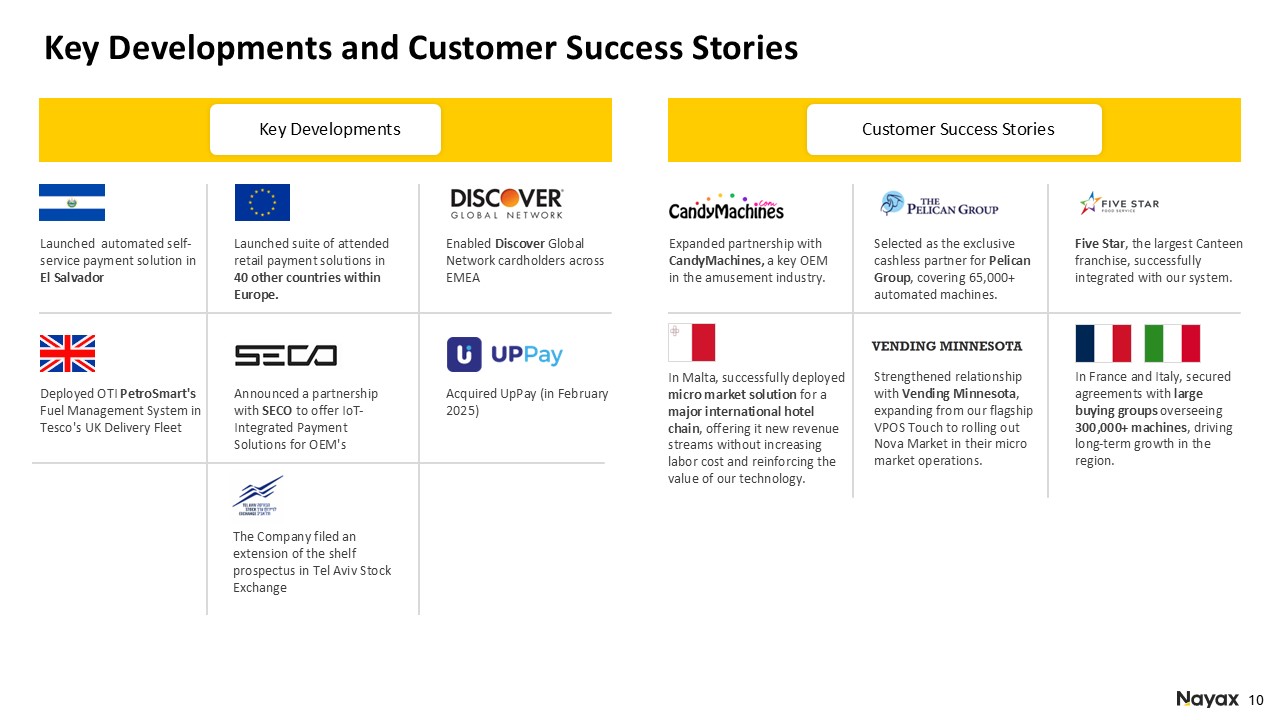

Key Developments and Customer Success Stories Key Developments Launched

automated self-service payment solution in El Salvador Launched suite of attended retail payment solutions in 40 other countries within Europe. Enabled Discover Global Network cardholders across EMEA Deployed OTI PetroSmart's Fuel Management

System in Tesco's UK Delivery Fleet Announced a partnership with SECO to offer IoT-Integrated Payment Solutions for OEM's Acquired UpPay (in February 2025) Customer Success Stories Expanded partnership with CandyMachines, a key OEM in the

amusement industry. Selected as the exclusive cashless partner for Pelican Group, covering 65,000+ automated machines. Five Star, the largest Canteen franchise, successfully integrated with our system. Strengthened relationship with Vending

Minnesota, expanding from our flagship VPOS Touch to rolling out Nova Market in their micro market operations. In France and Italy, secured agreements with large buying groups overseeing 300,000+ machines, driving long-term growth in the

region. In Malta, successfully deployed micro market solution for a major international hotel chain, offering it new revenue streams without increasing labor cost and reinforcing the value of our technology. The Company filed an extension of

the shelf prospectus in Tel Aviv Stock Exchange

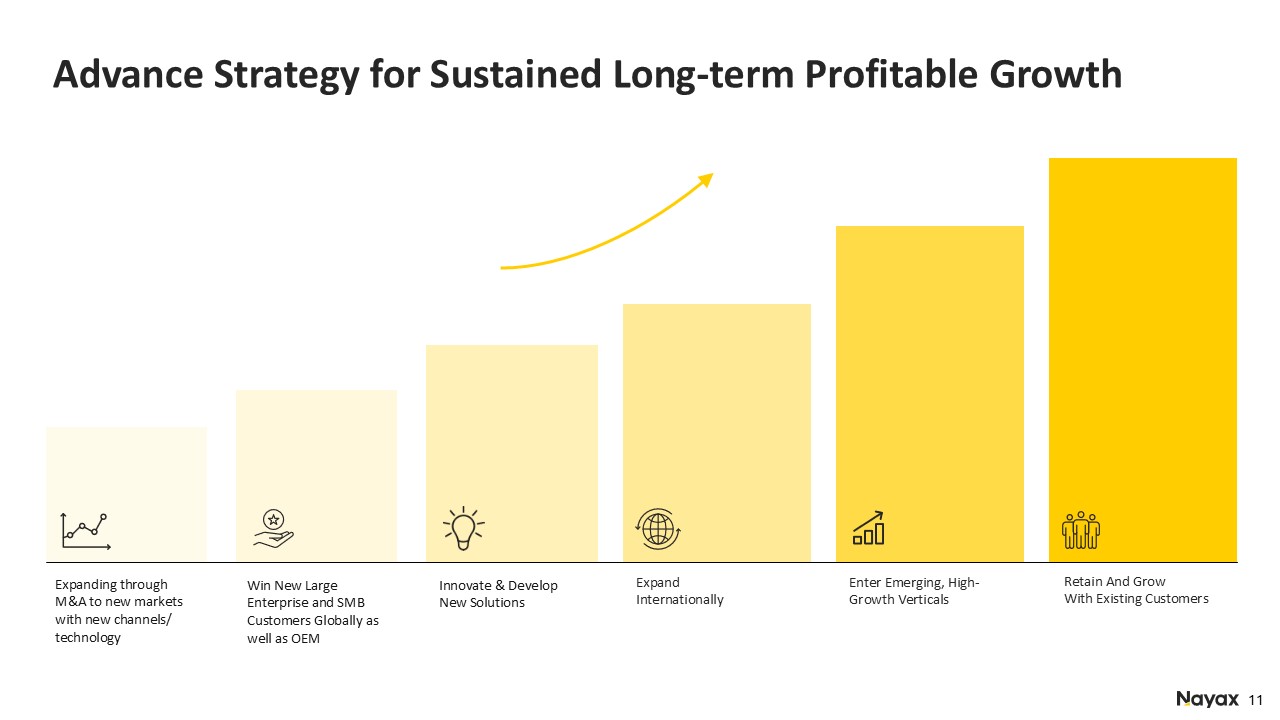

Advance Strategy for Sustained Long-term Profitable

Growth Expand Internationally Enter Emerging, High-Growth Verticals Retain And Grow With Existing Customers Innovate & Develop New Solutions Win New Large Enterprise and SMB Customers Globally as well as OEM Expanding through

M&A to new markets with new channels/ technology

Driving Growth with One Complete Solution for all Retailers Global Cashless

Payments Acceptance Multiple Integrated POS VPOS Touch Nova Market Management Platform Loyalty & Marketing Solutions Financing & Banking Multiple unattended retail verticals Automated Self Service Hospitality &

Retail Robust solution for numerous retail verticals Complete electric vehicle charging & payment solutions Energy & Mobility

Our Differentiated Go-To-Market

Strategy Offices 11 *POS Distributers 80+ Global OEM Partners 2,400+ Resellers 892 Online eShops 10 Financial Partners 50 Nano 1-25* SMB 26-3,000* Enterprise > 3k*

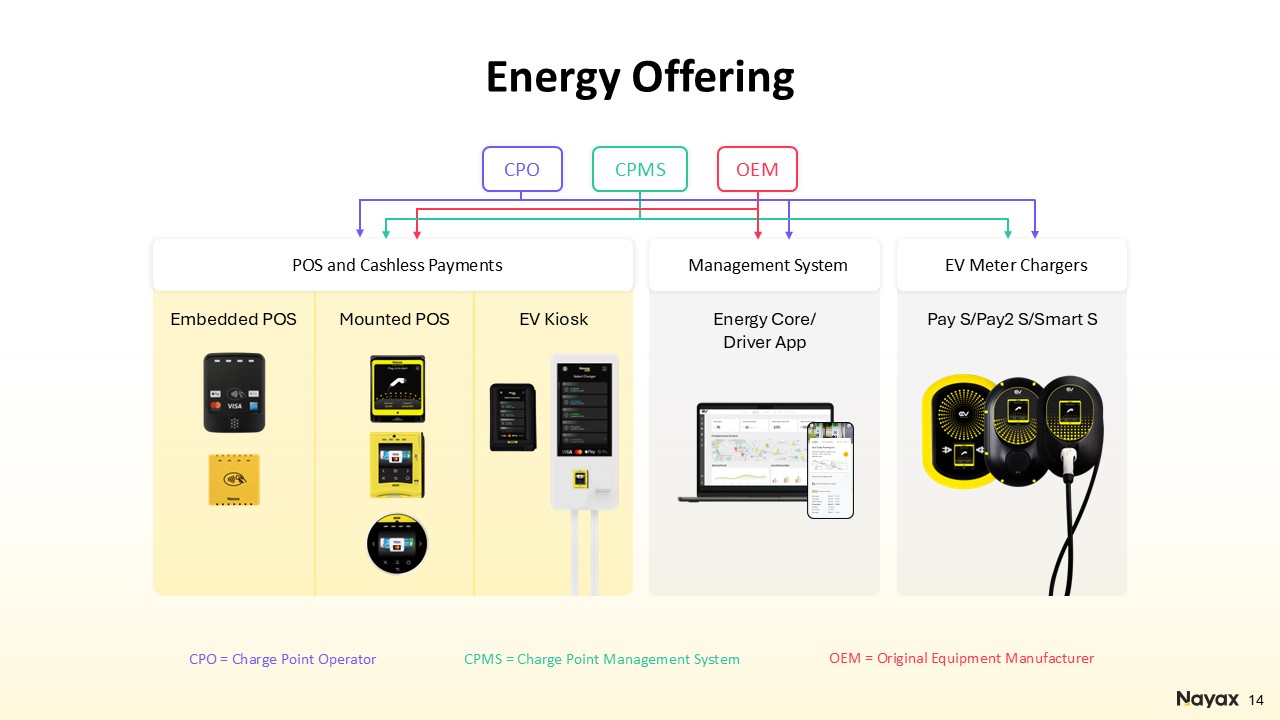

Energy Offering 14 CPO CPMS OEM Energy Core/ Driver App Management

System EV Meter Chargers Pay S/Pay2 S/Smart S Embedded POS EV Kiosk POS and Cashless Payments Mounted POS CPO = Charge Point Operator CPMS = Charge Point Management System OEM = Original Equipment Manufacturer

Partners Retail Your Way Enterprise Global Specialty Retail Self Service

& Ordering SMBs Retail SMB “Simplicity” Offering Payment Processing

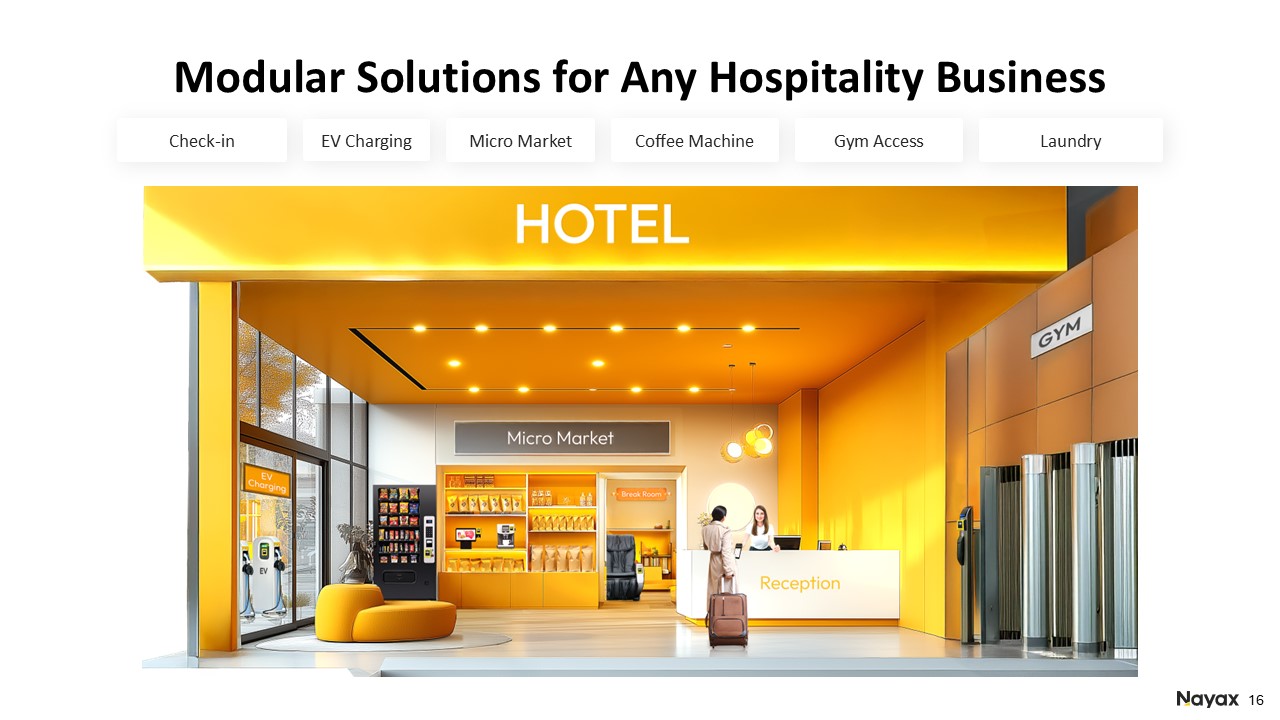

Check-in Micro Market EV Charging Coffee Machine Gym Access Laundry Modular

Solutions for Any Hospitality Business

Financials 17

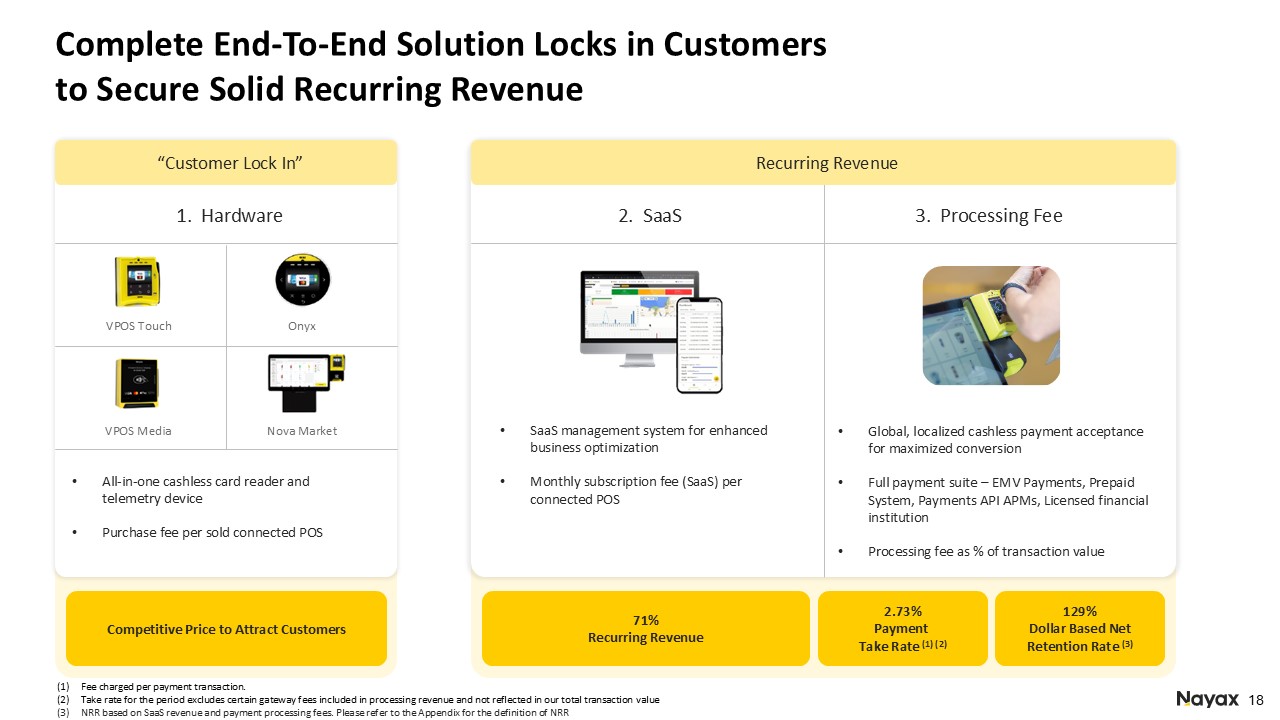

Complete End-To-End Solution Locks in Customers to Secure Solid Recurring

Revenue “Customer Lock In” VPOS Touch All-in-one cashless card reader and telemetry device Purchase fee per sold connected POS Onyx VPOS Media Nova Market Competitive Price to Attract Customers 1. Hardware 2. SaaS 3. Processing

Fee 71% Recurring Revenue 2.73% Payment Take Rate (1) (2) 129% Dollar Based Net Retention Rate (3) SaaS management system for enhanced business optimization Monthly subscription fee (SaaS) per connected POS Global, localized

cashless payment acceptance for maximized conversion Full payment suite – EMV Payments, Prepaid System, Payments API APMs, Licensed financial institution Processing fee as % of transaction value Fee charged per payment transaction. Take

rate for the period excludes certain gateway fees included in processing revenue and not reflected in our total transaction value NRR based on SaaS revenue and payment processing fees. Please refer to the Appendix for the definition of

NRR Recurring Revenue

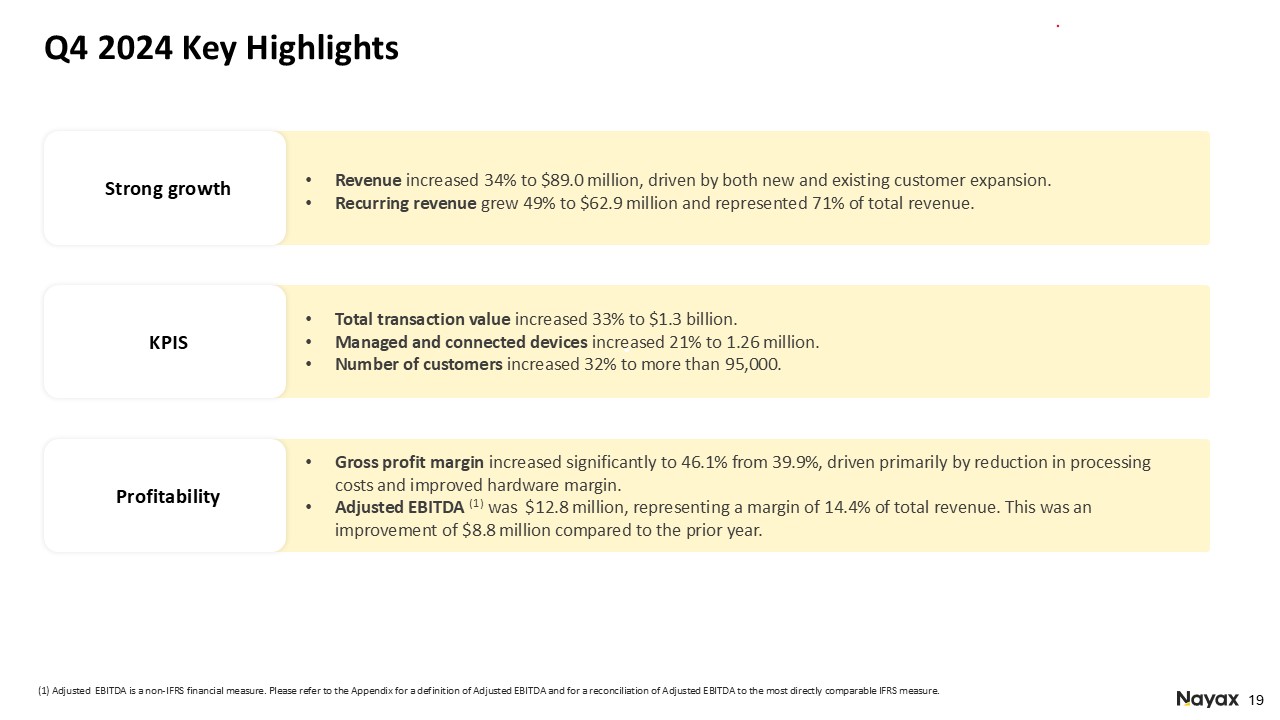

Strong growth Q4 2024 Key Highlights Revenue increased 34% to $89.0 million,

driven by both new and existing customer expansion. Recurring revenue grew 49% to $62.9 million and represented 71% of total revenue. Total transaction value increased 33% to $1.3 billion. Managed and connected devices increased 21% to 1.26

million. Number of customers increased 32% to more than 95,000. KPIS Profitability Gross profit margin increased significantly to 46.1% from 39.9%, driven primarily by reduction in processing costs and improved hardware margin. Adjusted

EBITDA (1) was $12.8 million, representing a margin of 14.4% of total revenue. This was an improvement of $8.8 million compared to the prior year. (1) Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a

definition of Adjusted EBITDA and for a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure.

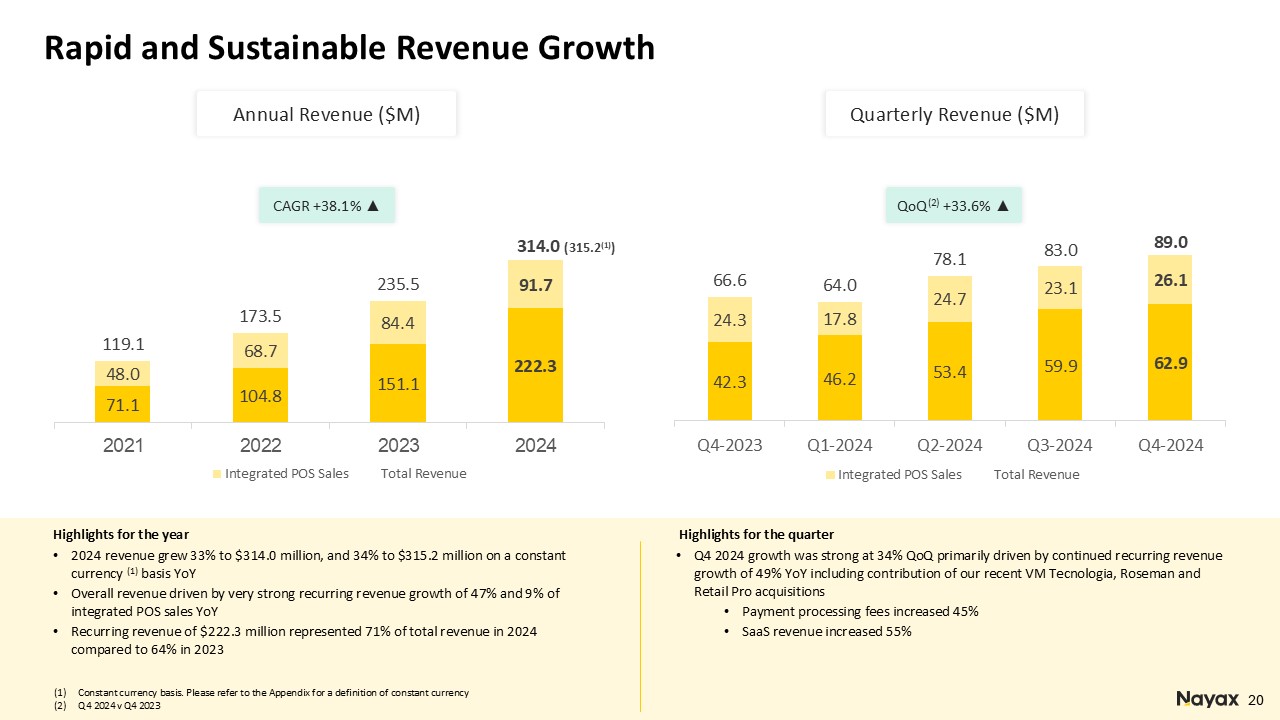

Rapid and Sustainable Revenue Growth Highlights for the year 2024 revenue grew

33% to $314.0 million, and 34% to $315.2 million on a constant currency (1) basis YoY Overall revenue driven by very strong recurring revenue growth of 47% and 9% of integrated POS sales YoY Recurring revenue of $222.3 million represented 71%

of total revenue in 2024 compared to 64% in 2023 Constant currency basis. Please refer to the Appendix for a definition of constant currency Q4 2024 v Q4 2023 CAGR +38.1% ▲ 20 Annual Revenue ($M) Quarterly Revenue ($M) QoQ(2) +33.6% ▲

Highlights for the quarter Q4 2024 growth was strong at 34% QoQ primarily driven by continued recurring revenue growth of 49% YoY including contribution of our recent VM Tecnologia, Roseman and Retail Pro acquisitions Payment processing fees

increased 45% SaaS revenue increased 55%

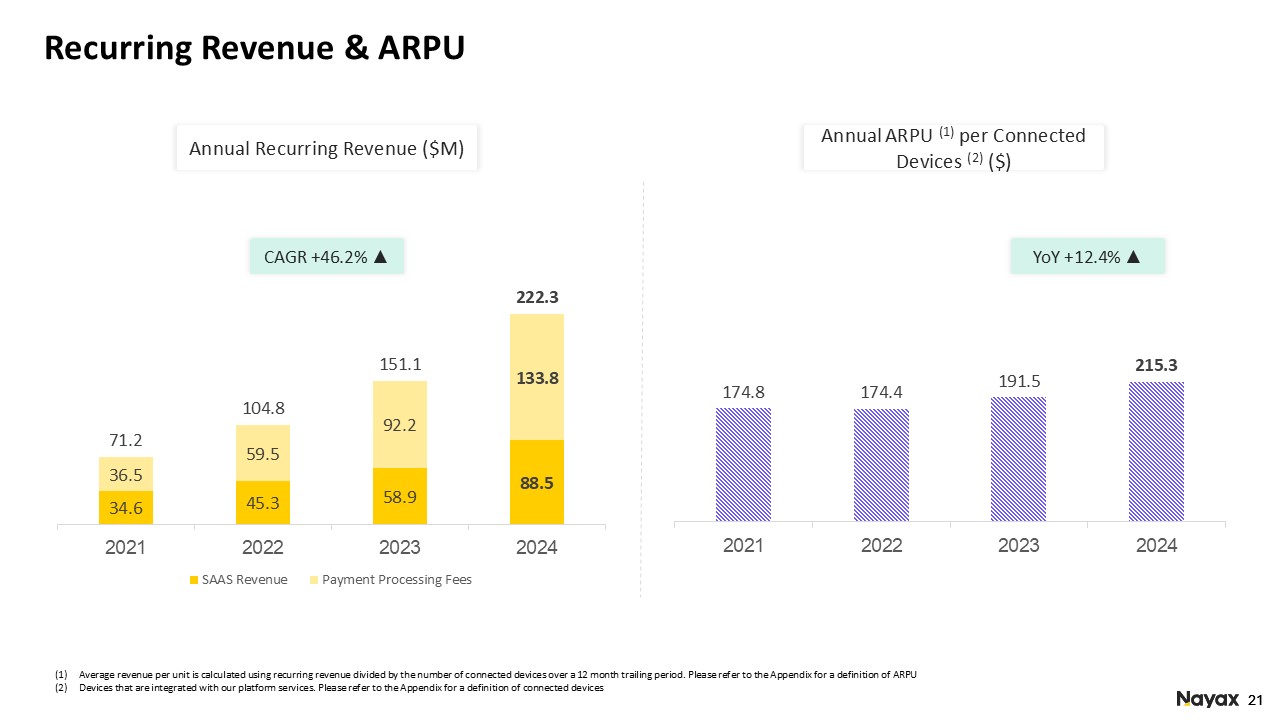

Recurring Revenue & ARPU Average revenue per unit is calculated using

recurring revenue divided by the number of connected devices over a 12 month trailing period. Please refer to the Appendix for a definition of ARPU Devices that are integrated with our platform services. Please refer to the Appendix for a

definition of connected devices CAGR +46.2% ▲ 21 Annual Recurring Revenue ($M) Annual ARPU (1) per Connected Devices (2) ($) YoY +12.4% ▲

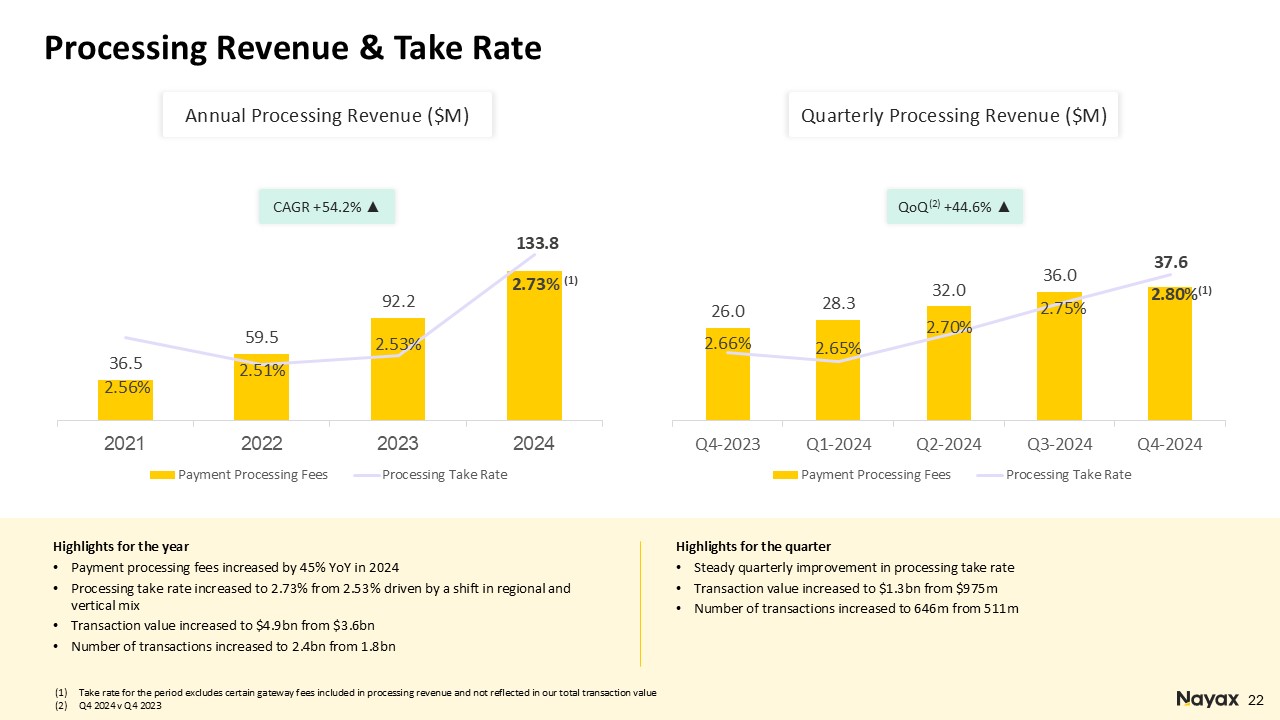

Processing Revenue & Take Rate CAGR +54.2% ▲ 22 Annual Processing Revenue

($M) Quarterly Processing Revenue ($M) QoQ(2) +44.6% ▲ Take rate for the period excludes certain gateway fees included in processing revenue and not reflected in our total transaction value Q4 2024 v Q4 2023 Highlights for the

year Payment processing fees increased by 45% YoY in 2024 Processing take rate increased to 2.73% from 2.53% driven by a shift in regional and vertical mix Transaction value increased to $4.9bn from $3.6bn Number of transactions increased

to 2.4bn from 1.8bn Highlights for the quarter Steady quarterly improvement in processing take rate Transaction value increased to $1.3bn from $975m Number of transactions increased to 646m from 511m

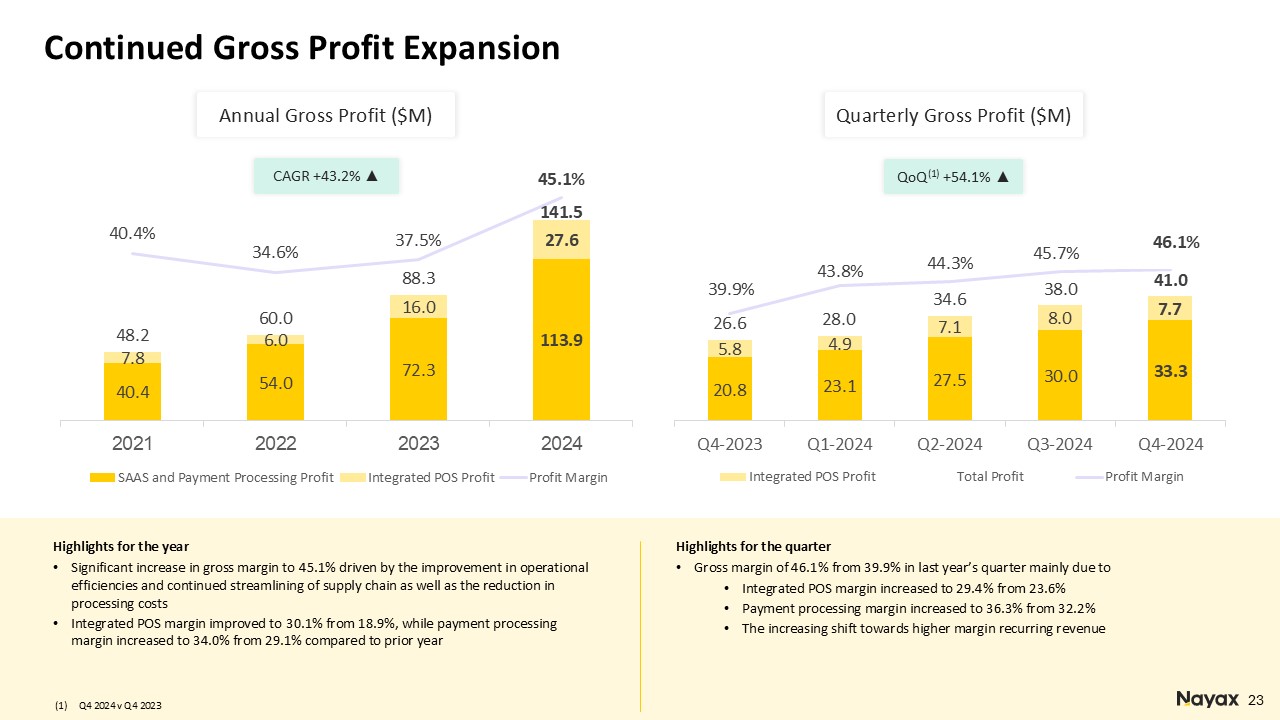

Continued Gross Profit Expansion CAGR +43.2% ▲ 23 Annual Gross Profit

($M) Quarterly Gross Profit ($M) QoQ(1) +54.1% ▲ Q4 2024 v Q4 2023 Highlights for the year Significant increase in gross margin to 45.1% driven by the improvement in operational efficiencies and continued streamlining of supply chain as

well as the reduction in processing costs Integrated POS margin improved to 30.1% from 18.9%, while payment processing margin increased to 34.0% from 29.1% compared to prior year Highlights for the quarter Gross margin of 46.1% from 39.9%

in last year’s quarter mainly due to Integrated POS margin increased to 29.4% from 23.6% Payment processing margin increased to 36.3% from 32.2% The increasing shift towards higher margin recurring revenue

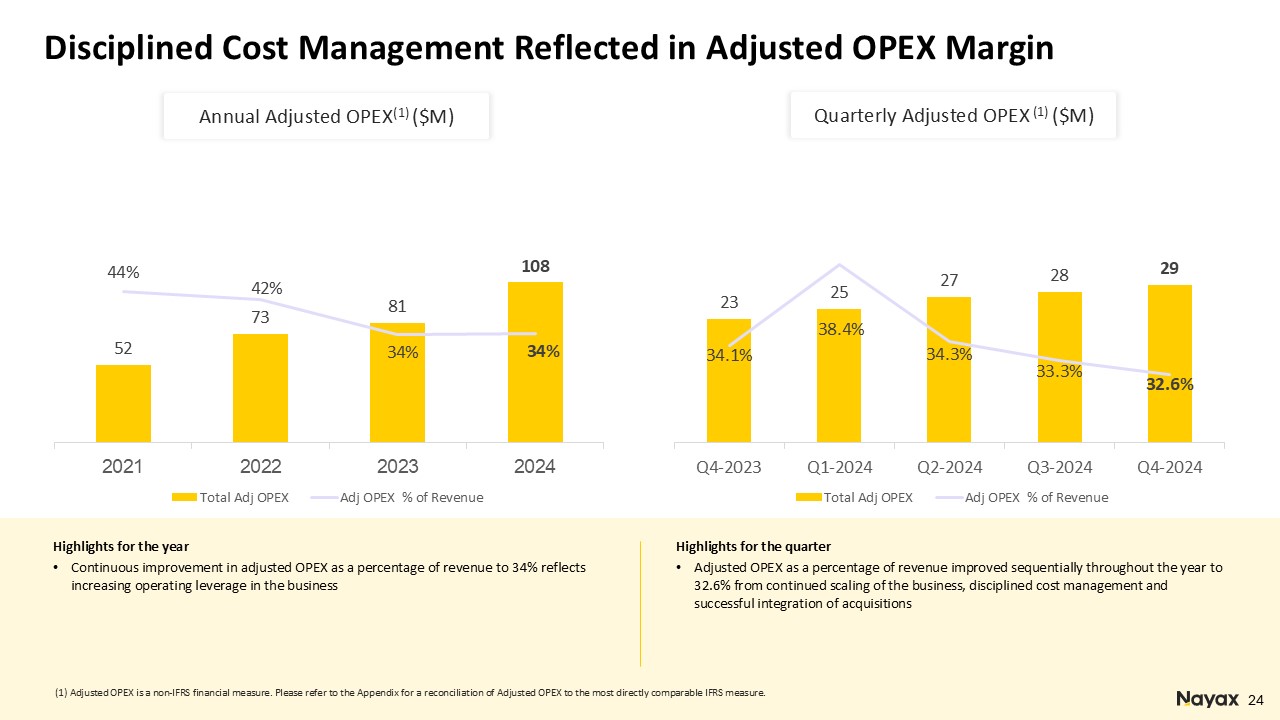

Disciplined Cost Management Reflected in Adjusted OPEX Margin 24 Annual Adjusted

OPEX(1) ($M) Quarterly Adjusted OPEX (1) ($M) Highlights for the year Continuous improvement in adjusted OPEX as a percentage of revenue to 34% reflects increasing operating leverage in the business Highlights for the quarter Adjusted

OPEX as a percentage of revenue improved sequentially throughout the year to 32.6% from continued scaling of the business, disciplined cost management and successful integration of acquisitions (1) Adjusted OPEX is a non-IFRS financial

measure. Please refer to the Appendix for a reconciliation of Adjusted OPEX to the most directly comparable IFRS measure.

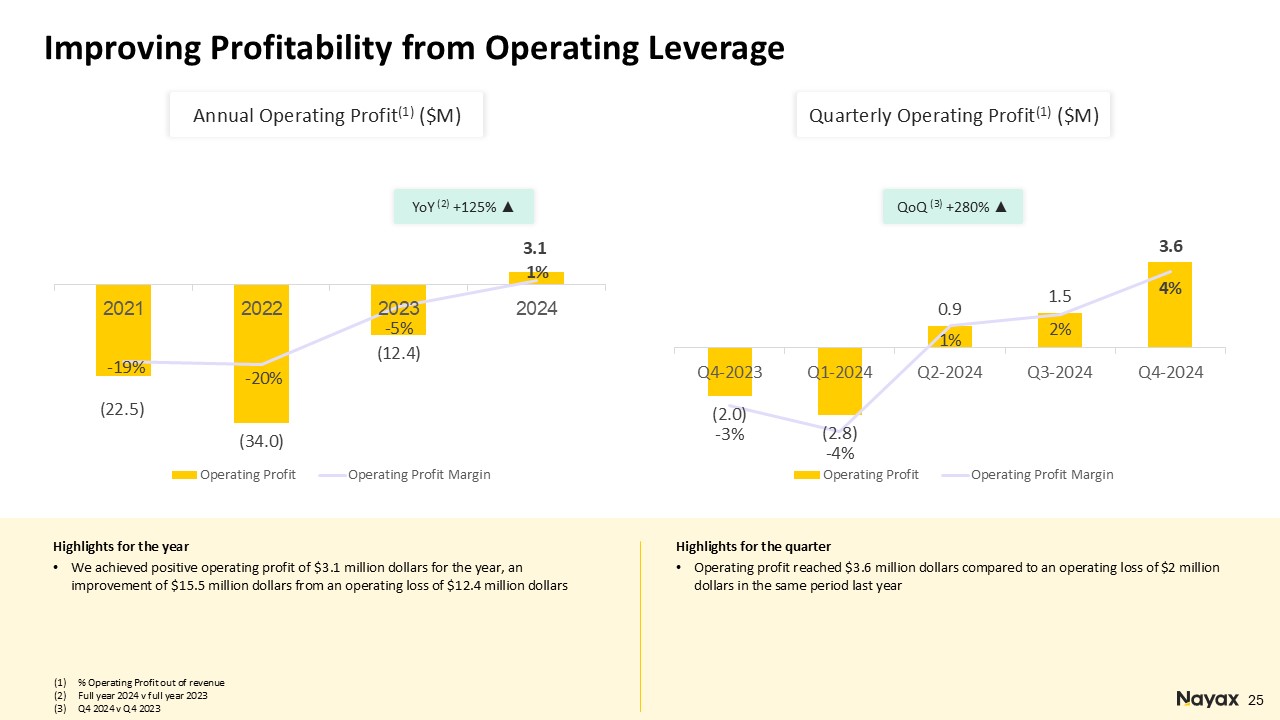

Improving Profitability from Operating Leverage YoY (2) +125% ▲ 25 Annual

Operating Profit(1) ($M) Quarterly Operating Profit(1) ($M) QoQ (3) +280% ▲ % Operating Profit out of revenue Full year 2024 v full year 2023 Q4 2024 v Q4 2023 Highlights for the year We achieved positive operating profit of $3.1 million

dollars for the year, an improvement of $15.5 million dollars from an operating loss of $12.4 million dollars Highlights for the quarter Operating profit reached $3.6 million dollars compared to an operating loss of $2 million dollars in the

same period last year

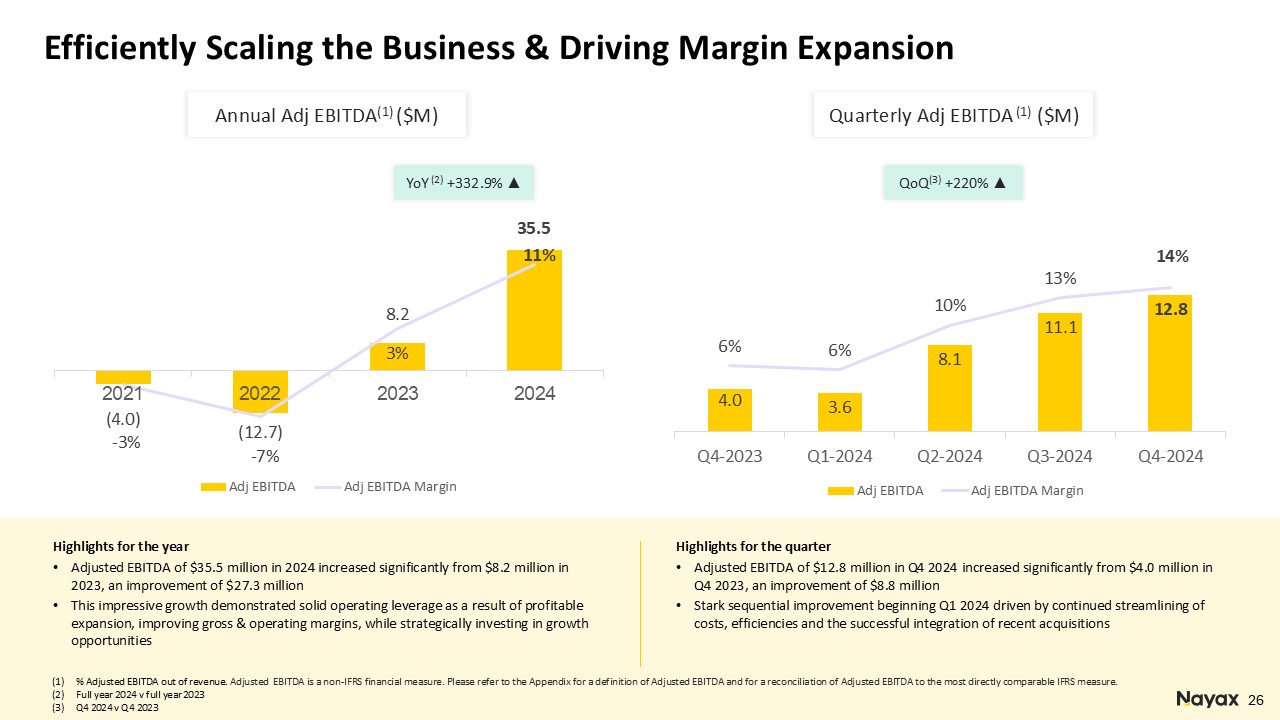

Efficiently Scaling the Business & Driving Margin Expansion YoY (2) +332.9%

▲ 26 Annual Adj EBITDA(1) ($M) Quarterly Adj EBITDA (1) ($M) QoQ(3) +220% ▲ % Adjusted EBITDA out of revenue. Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA and for

a reconciliation of Adjusted EBITDA to the most directly comparable IFRS measure. Full year 2024 v full year 2023 Q4 2024 v Q4 2023 Highlights for the year Adjusted EBITDA of $35.5 million in 2024 increased significantly from $8.2 million

in 2023, an improvement of $27.3 million This impressive growth demonstrated solid operating leverage as a result of profitable expansion, improving gross & operating margins, while strategically investing in growth

opportunities Highlights for the quarter Adjusted EBITDA of $12.8 million in Q4 2024 increased significantly from $4.0 million in Q4 2023, an improvement of $8.8 million Stark sequential improvement beginning Q1 2024 driven by continued

streamlining of costs, efficiencies and the successful integration of recent acquisitions

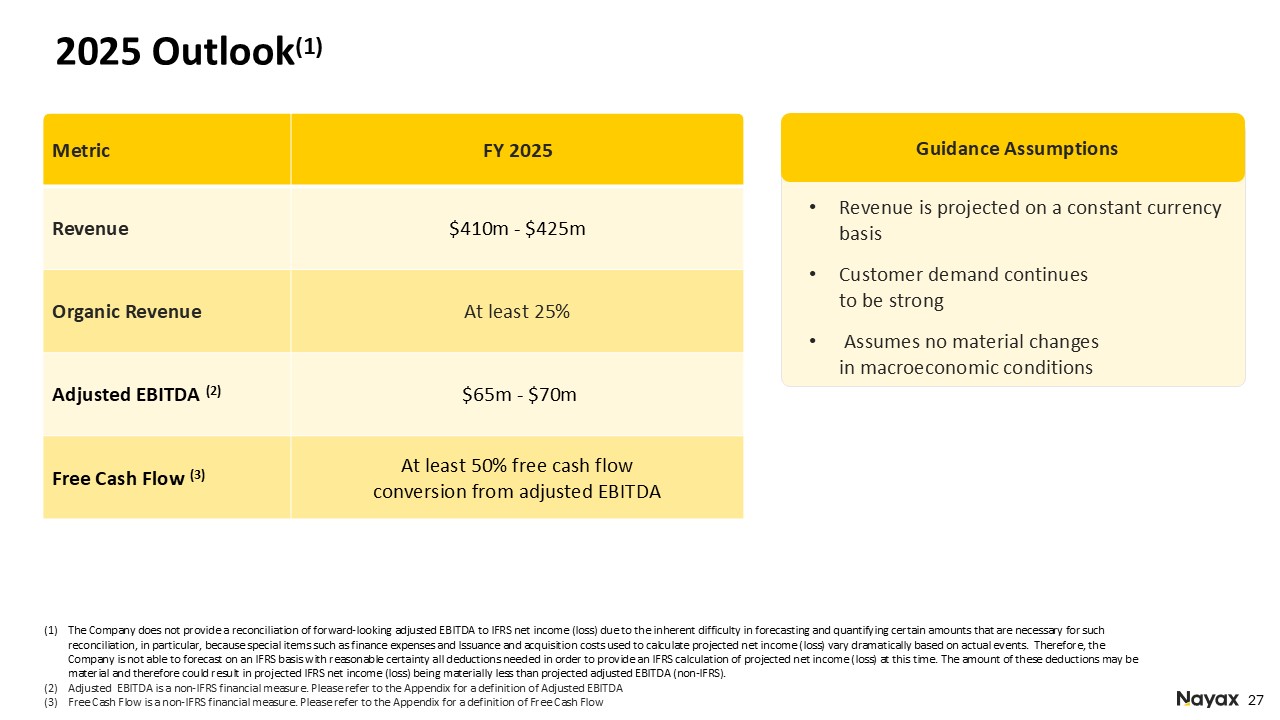

2025 Outlook(1) Guidance Assumptions Revenue is projected on a constant currency

basis Customer demand continues to be strong Assumes no material changes in macroeconomic conditions Metric FY 2025 Revenue $410m - $425m Organic Revenue At least 25% Adjusted EBITDA (2) $65m - $70m Free Cash Flow (3) At least

50% free cash flow conversion from adjusted EBITDA The Company does not provide a reconciliation of forward-looking adjusted EBITDA to IFRS net income (loss) due to the inherent difficulty in forecasting and quantifying certain amounts that

are necessary for such reconciliation, in particular, because special items such as finance expenses and Issuance and acquisition costs used to calculate projected net income (loss) vary dramatically based on actual events. Therefore, the

Company is not able to forecast on an IFRS basis with reasonable certainty all deductions needed in order to provide an IFRS calculation of projected net income (loss) at this time. The amount of these deductions may be material and therefore

could result in projected IFRS net income (loss) being materially less than projected adjusted EBITDA (non-IFRS). Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a definition of Adjusted EBITDA Free Cash

Flow is a non-IFRS financial measure. Please refer to the Appendix for a definition of Free Cash Flow

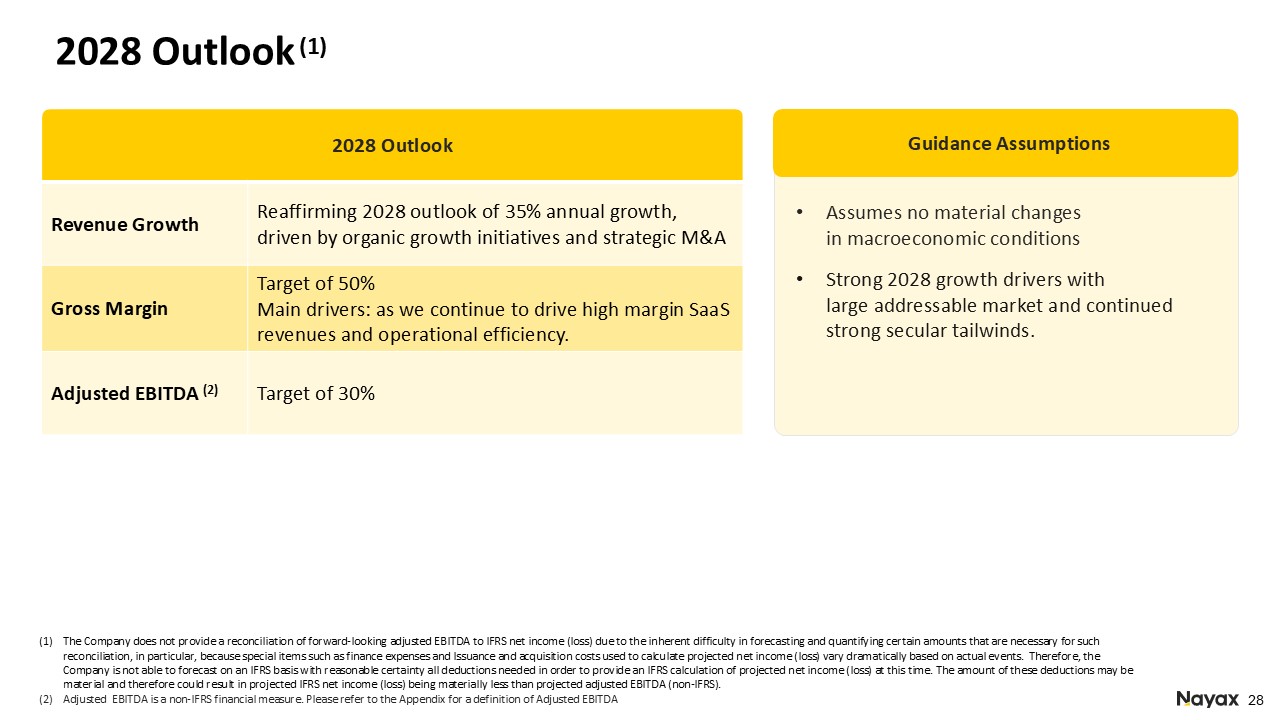

2028 Outlook (1) Assumes no material changes in macroeconomic conditions Strong

2028 growth drivers with large addressable market and continued strong secular tailwinds. The Company does not provide a reconciliation of forward-looking adjusted EBITDA to IFRS net income (loss) due to the inherent difficulty in forecasting

and quantifying certain amounts that are necessary for such reconciliation, in particular, because special items such as finance expenses and Issuance and acquisition costs used to calculate projected net income (loss) vary dramatically based

on actual events. Therefore, the Company is not able to forecast on an IFRS basis with reasonable certainty all deductions needed in order to provide an IFRS calculation of projected net income (loss) at this time. The amount of these

deductions may be material and therefore could result in projected IFRS net income (loss) being materially less than projected adjusted EBITDA (non-IFRS). Adjusted EBITDA is a non-IFRS financial measure. Please refer to the Appendix for a

definition of Adjusted EBITDA 2028 Outlook Revenue Growth Reaffirming 2028 outlook of 35% annual growth, driven by organic growth initiatives and strategic M&A Gross Margin Target of 50%Main drivers: as we continue to drive high margin

SaaS revenues and operational efficiency. Adjusted EBITDA (2) Target of 30% Guidance Assumptions

Appendix 29

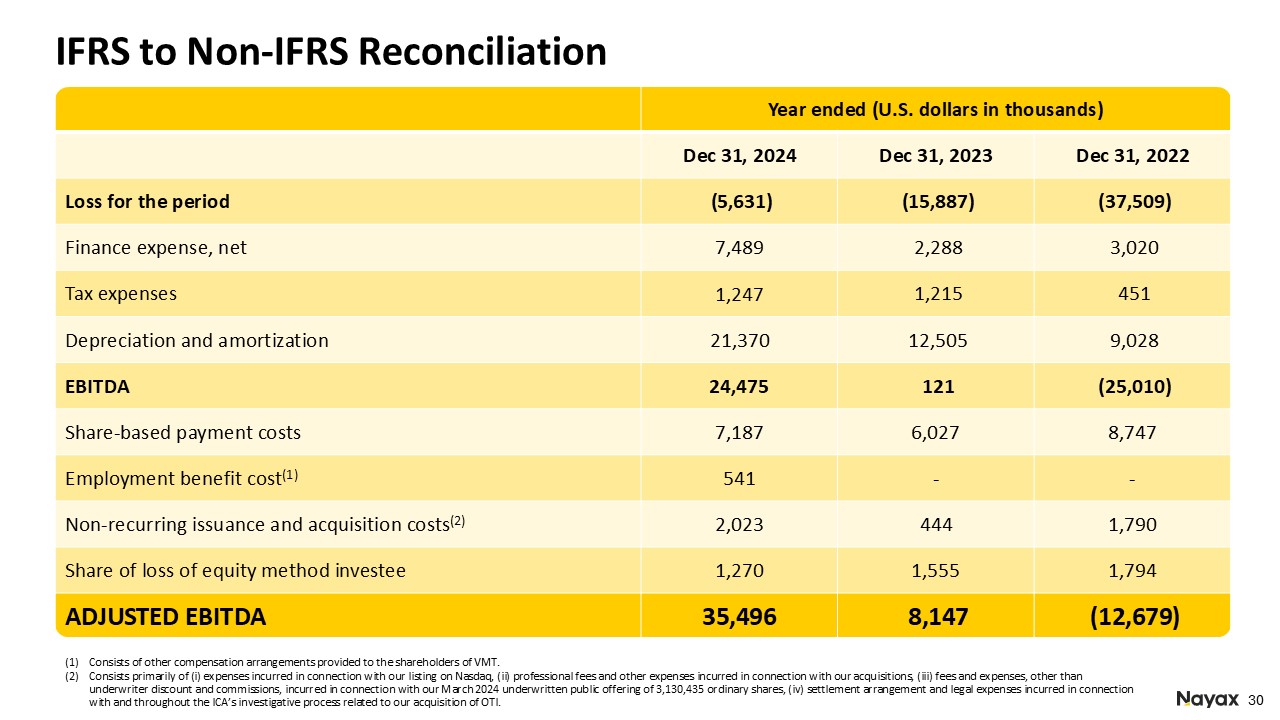

Year ended (U.S. dollars in thousands) Dec 31, 2024 Dec 31, 2023 Dec 31,

2022 Loss for the period (5,631) (15,887) (37,509) Finance expense, net 7,489 2,288 3,020 Tax expenses 1,247 1,215 451 Depreciation and amortization 21,370 12,505 9,028 EBITDA 24,475 121

(25,010) Share-based payment costs 7,187 6,027 8,747 Employment benefit cost(1) 541 - - Non-recurring issuance and acquisition costs(2) 2,023 444 1,790 Share of loss of equity method investee 1,270 1,555 1,794 ADJUSTED

EBITDA 35,496 8,147 (12,679) IFRS to Non-IFRS Reconciliation Consists of other compensation arrangements provided to the shareholders of VMT. Consists primarily of (i) expenses incurred in connection with our listing on Nasdaq, (ii)

professional fees and other expenses incurred in connection with our acquisitions, (iii) fees and expenses, other than underwriter discount and commissions, incurred in connection with our March 2024 underwritten public offering of 3,130,435

ordinary shares, (iv) settlement arrangement and legal expenses incurred in connection with and throughout the ICA’s investigative process related to our acquisition of OTI.

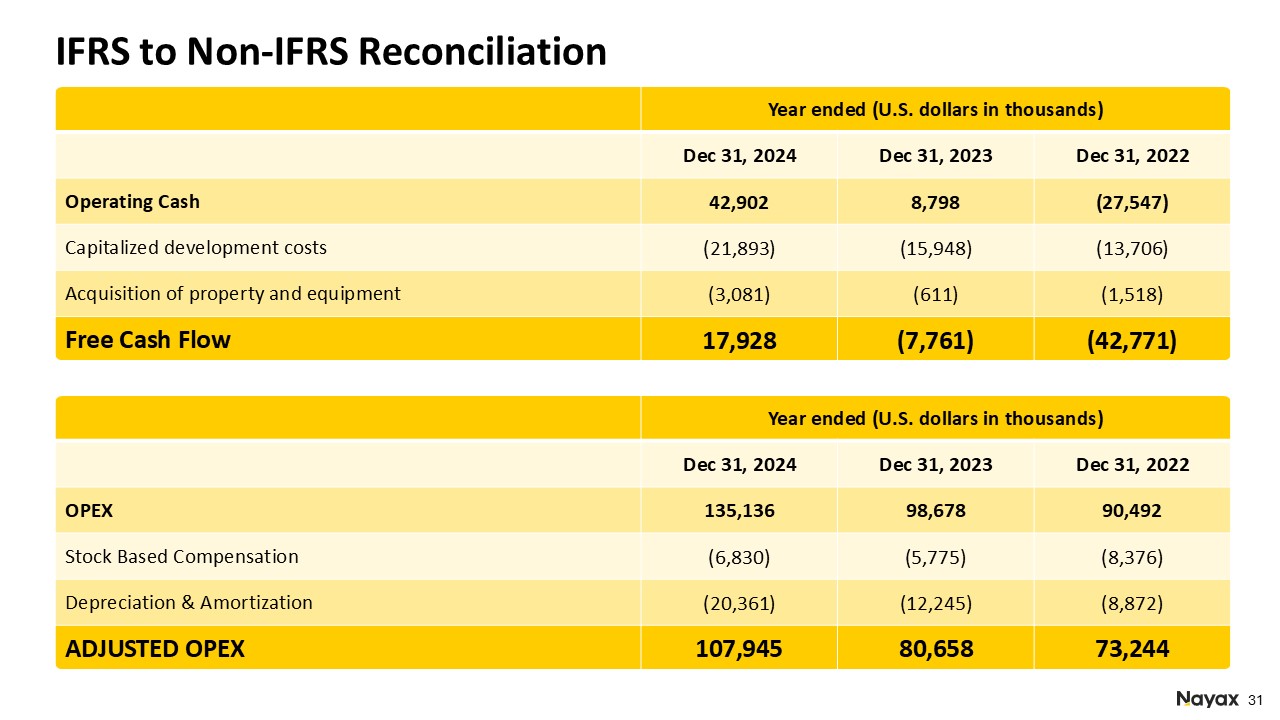

Year ended (U.S. dollars in thousands) Dec 31, 2024 Dec 31, 2023 Dec 31,

2022 Operating Cash 42,902 8,798 (27,547) Capitalized development costs (21,893) (15,948) (13,706) Acquisition of property and equipment (3,081) (611) (1,518) Free Cash Flow 17,928 (7,761) (42,771) IFRS to Non-IFRS

Reconciliation Year ended (U.S. dollars in thousands) Dec 31, 2024 Dec 31, 2023 Dec 31, 2022 OPEX 135,136 98,678 90,492 Stock Based Compensation (6,830) (5,775) (8,376) Depreciation &

Amortization (20,361) (12,245) (8,872) ADJUSTED OPEX 107,945 80,658 73,244

IFRS to Non-IFRS Reconciliation Consists of other compensation arrangements

provided to the shareholders of VMT. Consists primarily of (i) expenses incurred in connection with our listing on Nasdaq, (ii) professional fees and other expenses incurred in connection with our acquisitions, (iii) fees and expenses, other

than underwriter discount and commissions, incurred in connection with our March 2024 underwritten public offering of 3,130,435 ordinary shares, (iv) settlement arrangement and legal expenses incurred in connection with and throughout the ICA’s

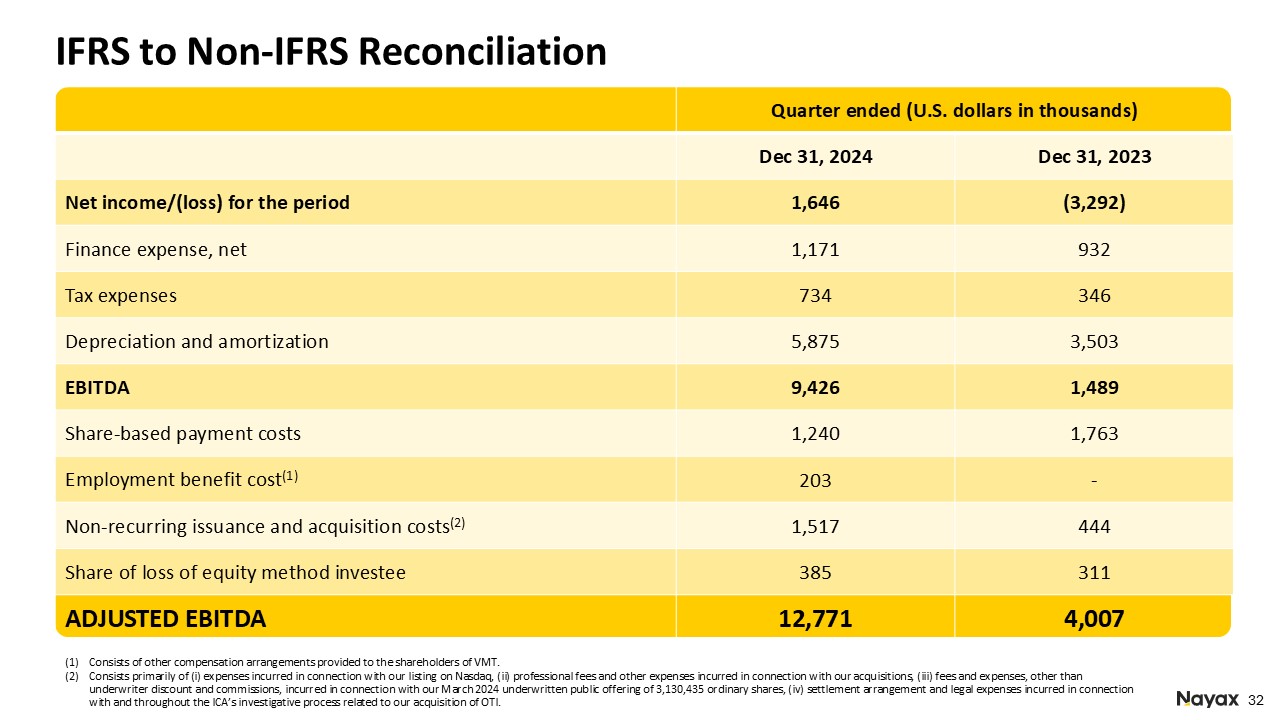

investigative process related to our acquisition of OTI. Quarter ended (U.S. dollars in thousands) Dec 31, 2024 Dec 31, 2023 Net income/(loss) for the period 1,646 (3,292) Finance expense, net 1,171 932 Tax expenses

734 346 Depreciation and amortization 5,875 3,503 EBITDA 9,426 1,489 Share-based payment costs 1,240 1,763 Employment benefit cost(1) 203 - Non-recurring issuance and acquisition costs(2) 1,517 444 Share of loss of equity

method investee 385 311 ADJUSTED EBITDA 12,771 4,007

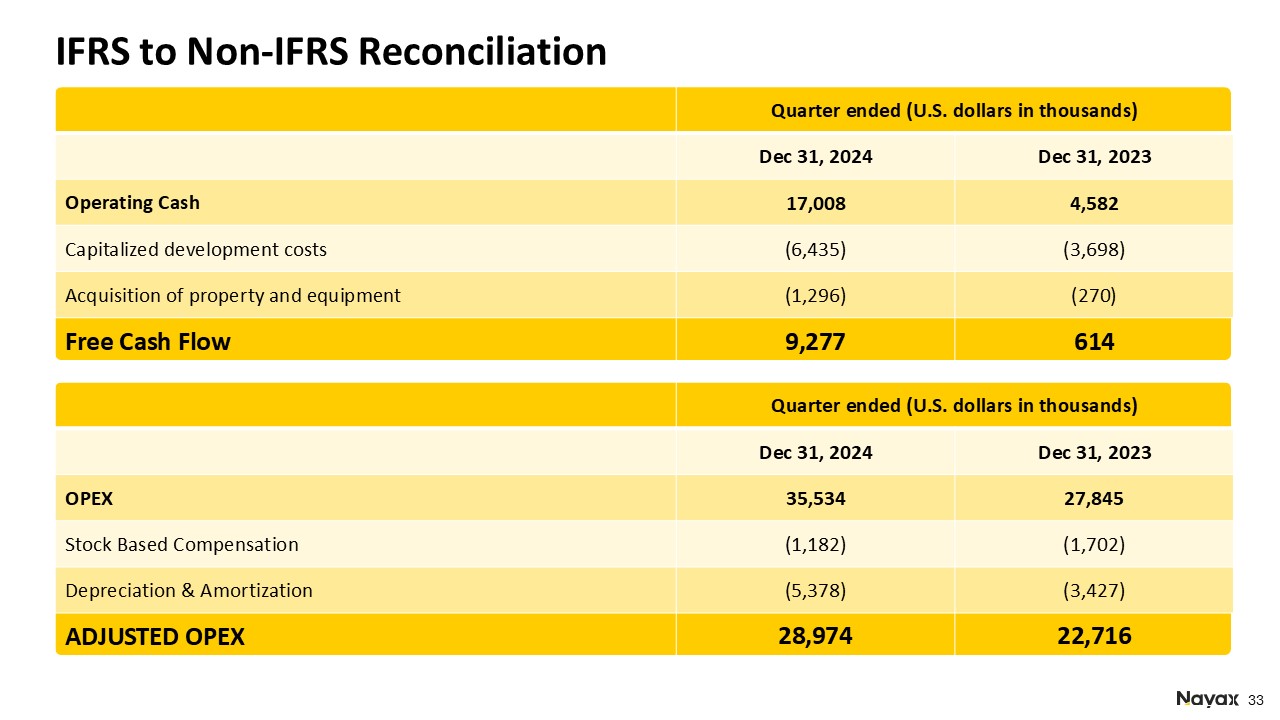

IFRS to Non-IFRS Reconciliation Quarter ended (U.S. dollars in thousands) Dec

31, 2024 Dec 31, 2023 Operating Cash 17,008 4,582 Capitalized development costs (6,435) (3,698) Acquisition of property and equipment (1,296) (270) Free Cash Flow 9,277 614 Quarter ended (U.S. dollars in thousands) Dec 31,

2024 Dec 31, 2023 OPEX 35,534 27,845 Stock Based Compensation (1,182) (1,702) Depreciation & Amortization (5,378) (3,427) ADJUSTED OPEX 28,974 22,716

Key Definitions Measured as a percentage of Recurring Revenue from returning

customers in a given period as compared to the Recurring Revenue from such customers in the prior period, which reflects the increase in revenue and the rate of losses from customer churn. Dollar-based net retention rate Nayax presents

constant currency information to provide a framework for assessing how our underlying businesses performed excluding the effect of foreign currency rate fluctuations. Future expected results for transactions in currencies other than United

States dollars are converted into United States dollars using the exchange rates in effect in the last month of the reporting period. Nayax provides this financial information to aid investors in better understanding our performance. These

constant currency financial measures presented in this release should not be considered as a substitute for, or superior to, the measures of financial performance prepared in accordance with IFRS. Constant Currency Adjusted EBITDA is a

non-IFRS financial measure that we define as profit or loss for the period plus finance expenses, tax expense, depreciation and amortization, share-based compensation costs, non-recurring issuance and acquisition related costs and our share in

losses of associates accounted for by the equity method. Adjusted EBITDA Devices that are integrated with our platform services, either sold or leased by us, enabling seamless connectivity, data exchange, and service management. These devices

operate within our ecosystem, ensuring optimized performance and enhanced user experience. Connected Devices A financial metric that measures the average recurring revenue generated per connected device over a 12 months trailing

period. ARPU Devices that are operated by our customers. Managed & Connected Devices Customers that contributed to Nayax revenue in the last 12 months. End Customers SAAS revenue and payment processing fees. Recurring Revenue The

percentage of revenue lost as a result of customers leaving our platform in the last 12 months. Revenue Churn Revenue generated within a given cohort over the years presented. Each cohort represents customers from whom we received revenue for

the first time, in a given year. Existing Customer Expansion Net cash provided from operating activities minus capitalized development costs and acquisition of property and equipment. Free Cash Flow Third-party devices on which we provide

a software solution, enabling functionality, monitoring, and management without direct ownership or control over the hardware. Managed Devices Total OPEX excluding stock base compensation, depreciation and amortization Adjusted OPEX

Aaron Greenberg Chief Strategy Officer ir@nayax.com IR Contact Thank

You! ir.nayax.com Website