Exhibit 99.3

Fair Market Value Appraisal: Internal Use

Client

Series 526, a series of Masterworks Vault 3, LLC

Intended User

Masterworks Administrative Services, LLC on behalf of the above-named Client.

Intended Use

To determine fair market value as outlined in the Scope of Work.

Effective Date of Valuation

January 28, 2026

Date of Report

February 2, 2026

TABLE OF CONTENTS

| Certification | 2 |

| About Masterworks | 3 |

| Scope of Work | 3 |

| Definition of Value | 4 |

| Method of Research | 4 |

| Method of Examination | 4 |

| Assignment Conditions | 4 |

| Approach to Value | 5 |

| Opinion of Value | 5 |

| Global Art Market Overview | 6 |

| Subject Artwork | 9 |

| Fair Market Value | 9 |

| Artist Background | 10 |

| Valuation Narrative | 10 |

| Comparable Sales | 12 |

| Sources of Data | 13 |

| Masterworks Appraisers’ Qualifications | 13 |

| Statements and Disclosures | 14 |

| Appraisal Terminology and Definitions | 15 |

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 1 |

Certification

I certify that, to the best of my knowledge and belief:

| ● | The statements of fact contained in this Appraisal Report are true and correct. |

| ● | The reported analyses, opinions, and conclusions are limited only by the reported assumptions and limiting conditions, and are my personal, impartial, and unbiased professional analyses, opinions and conclusions. |

| ● | In my role at Masterworks Administrative Services, LLC, I provide on-going valuation and consultation regarding the Masterworks Portfolio; in this context, I frequently perform an initial review of the Artwork prior to its acquisition by Masterworks. |

| ● | I am an employee of Masterworks Administrative Services, LLC, which serves as the administrator to the owner of the Artwork. Masterworks Administrative Services, LLC receives revenue for the administration of the Artwork and, its affiliate, Masterworks Gallery, LLC holds a financial interest in the corporate entity that owns the Artwork. However, I have no direct personal interest or bias with respect to the property that is the subject of this report or to the parties involved with this assignment. |

| ● | My engagement in this assignment was not contingent upon developing or reporting predetermined results. |

| ● | My compensation for completing this assignment is not contingent upon the development or reporting of a predetermined value or direction in value that favors the cause of Masterworks, the amount of the value opinion, the attainment of a stipulated result, or the occurrence of a subsequent event directly related to the intended use of this appraisal. |

| ● | My analyses, opinions, and conclusions were developed, and this report has been prepared, in conformity with the Uniform Standards of Professional Appraisal Practice. |

| ● | The property that is the subject of this report was inspected by a member of the Masterworks’ Acquisitions team and/or Appraisal team; in the event that I did not personally inspect the artwork, I relied on information, including photographs and other documentation, supplied by both the seller and the Masterworks team member who conducted the inspection. |

| ● | I received personal property appraisal assistance from Jessica Maliszewski, Senior Appraiser, who assisted with research and appraisal development. |

| |

| Abigail Athanasopoulos | |

| Director of Appraisals | |

| Masterworks Administrative Services, LLC |

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 2 |

About Masterworks

Masterworks Administrative Services, LLC acts as manager for individual Delaware LLCs that own, through a segregated portfolio of Masterworks Cayman SPC, a single artwork as its sole investment which have been offered and sold as securities pursuant to an exemption from registration under Rule 251(a)(2) of Regulation A under the Securities Act of 1933. For the purposes of this Appraisal Report only, and unless otherwise indicated in a specific instance, this organizational structure shall be referred to as “Masterworks.”

Scope of Work

The following appraisal report (“Appraisal Report”) was prepared to conclude the Fair Market Value of the subject artwork (the “Artwork”) prior to acquisition. This Appraisal Report is not valid for any other purpose. Values stated may not reflect additional expenses which might be incurred should the Artwork be sold such as advertising costs, or shipping. For the avoidance of doubt, this Appraisal Report shall not be construed as providing investment advice or be relied upon by those making investment decisions. Given the volume of transactions, internally compiled intelligence and qualified personnel, among other items, Masterworks believes it is well-positioned to appraise artworks in the Masterworks Portfolio. This appraisal was prepared in accordance with the most recent publication of the Uniform Standards of Professional Appraisal Practice (“USPAP”; last issued in 2024) developed by the Appraisal Standards Board of the Appraisal Foundation, by a USPAP-compliant appraiser from the Masterworks Appraiser(s). It is noted that there are potential conflicts of interest given that all Masterworks Appraiser(s) are employees of Masterworks, and Masterworks retains an ownership and other pecuniary interests in the Artwork. This valuation is valid as of the Effective Date, and does not take into account any sales of comparable works or market movement that occur after the Effective Date.

The Artwork is owned by Series 526, a series of Masterworks Vault 3, and this Appraisal Report is intended for use by Series 526, a series of Masterworks Vault 3, and its subsidiaries (collectively referred to as “Series 526”). The Appraisal Report has been prepared by the Masterworks Appraiser(s) on behalf of Masterworks Administrative Services, LLC in its capacity as administrator to Series 526, a series of Masterworks Vault 3.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 3 |

Definition of Value

The definition of fair market value is set forth in IRS Section 1.170 and 20.2031-1 which states that: “The Fair Market Value is the price at which the property would change hands between a willing buyer and a willing seller, neither being under any compulsion to buy or to sell and both having reasonable knowledge of relevant facts.” (According to Technical Advisory Memorandum [TAM] 9235005 [May 27, 1992], fair market value should include the buyer’s premium) 20.2031 (b) continues “the fair market value of an item of property includible in the decedent’s gross estate is not to be determined by a forced sale price. Nor is the fair market value of an item of property to be determined by the sale price of that item in a market other than that in which such item is commonly sold to the public, taking into account the location of the item wherever appropriate.”

Method of Research

In preparing this Appraisal Report, research was conducted in the Masterworks offices. The offices are equipped with an extensive library relevant to the artworks held in the Masterworks’ collection. Research involved but was not limited to: i) detailed research of comparable transactions occurring at public auction via third-party, on-line artwork-focused databases including artprice and artnet; ii) review of an internal database of similar works and works by the same artists that have been previously offered to Masterworks for purchase; iii) review of historical market trends within the specific artist market, the market for similar (or comparable) artwork based on internally-compiled market indices, and the broader art market; iv) review of past condition reports, photos, previous appraisals, sales transactions, auction catalogues and other documentation related to the Artwork; iv) review of general art market intelligence and observations acquired by Masterworks through the attendance of auction previews, art fairs exhibiting comparable works, gallery and museum exhibitions and v) art historical research pertaining to the artist and the subject artwork using Masterworks’ Reference Library and resources available at the New York Public Library, the Metropolitan Museum of Art’s Watson Library and the Frick’s Art Reference Library among others. Sources for art market data include third-party online transaction databases, physical auction catalogues, sales (or offers) made to Masterworks by dealers and other general market observations and intelligence.

Method of Examination

The Artwork was last physically inspected by third-party conservator Hamish Dewar for Masterworks on January 28, 2026, with the most recent condition report issued on January 28, 2026; it is assumed that the artwork has sustained no visible apparent change in its condition since that time.

Assignment Conditions

During the development of this Appraisal and preparation of this Appraisal Report, the Masterworks Appraiser(s) relied on photographs and descriptions of the Artwork retained in Masterworks’ collection files to confirm the work’s physical characteristics. Relevant information regarding comparable sales is included in this report or, in the case of confidential private sale data, maintained in the Masterworks Appraiser(s)’work file at the offices of Masterworks. The Masterworks Appraiser(s) may not have personally examined the comparable works referenced in the Appraisal Report, and thus relied on the information available through online databases, auction catalogues, private dealers and/or galleries. Not all comparables have current condition reports for review.

| ● | Extraordinary Assumptions: An extraordinary assumption is defined by USPAP as “an assumption, directly related to a specific assignment, as of the effective date of the assignment results, which, if found to be false, could alter the appraiser’s opinions or conclusions.” The appraised value assumes the clear title, good condition, and authenticity. While members of Masterworks may have viewed the work prior to acquisition by Masterworks, the Masterworks Appraiser(s) did not inspect the property in person during the preparation of this report, and thus relied solely on images and descriptions retained in Masterworks’ files and assumed this information to be accurate. The Masterworks Appraiser(s) may not have been able to examine the comparable works used for this assignment and thus relied on information available through online databases, auction catalogues, private dealers and or galleries. When no condition report was available for comparable works, the object is assumed to be in good condition. |

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 4 |

| ● | Hypothetical Conditions: A hypothetical condition is defined by USPAP as “a condition, directly related to a specific assignment, which is contrary to what is known by the appraiser to exist on the effective date of the assignment results but is used for the purpose of analysis.” No hypothetical conditions have been applied to this Appraisal Report. |

| ● | Limiting Conditions: The following Limiting Conditions exist in this assignment. Such conditions may limit the appraisers’ expertise in specific areas as well as the perceived responsibilities of the assignment. Some are also considered to be Extraordinary Assumptions and were taken by the appraiser as facts. If these Limitations and Extraordinary Assumptions are found to be untrue, the appraiser’s opinions, including the opinions of value may be affected. |

| ○ | The Appraisal Report is limited in that the appraiser is not an authenticator. This is also considered an Extraordinary Assumption as they assume the work is authentic. |

| ○ | This Appraisal Report is limited in that the appraiser is not a conservator. As such, they did not prepare a professional condition report for the subject work. This is also considered an Extraordinary Assumption as they assume the work is in good condition. |

Approach to Value

The Artwork was evaluated based on the “Sales Comparison Approach.” This method of valuation involves analysis of recent sales involving similar objects, also referred to as comparable sales, which have sold within the market that is most common for each object. In the context of the Artwork, comparable sales generally include sales of other artwork (or the Artwork itself) created by the same artist, with similar dimensions, creation period range and subject matter as the Artwork. Comparable sales may have taken place at public auction or in private sales, if such private sales information is verifiable. The Appraisers may adjust the valuation of the Artwork, otherwise derived from past comparable sales, based on a historical price appreciation benchmark for similar works by the artist or the artist’s market overall.

The “Income Approach” and the “Cost Approach” were also considered for this appraisal. While the subject work is an income producing asset, such income is not part of the scope of the assignment and thus the “Income Approach” was not applied. The “Cost Approach” was also considered and since its application was not relevant to the assignment’s scope of work, it was not applied.

Opinion of Value

The value expressed herein is based on the Masterworks Appraiser(s)’ best judgment and opinion. This value is not a representation or warranty that the item will realize this value if offered for sale in an appropriate market. The value expressed is based on current information on the date the Appraisal Report was made. No opinion is expressed as to any past value, nor, unless otherwise expressly stated, as to any future value.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 5 |

Global Art Market Overview

The most recent major shift in the art market occurred in 2020, which proved to be a truly unprecedented year across sectors, when the COVID-19 health crisis began in the first quarter, prompting global shutdowns and social distancing efforts. According to the 2021 Art Basel and UBS annual report, global art sales only reached $50.1 billion in 2020, a 22% decrease from 2019, but still above the 2009 recession low.1 2021 saw the continuation of the pandemic-related challenges, yet according to Dr. McAndrew’s 2022 Art Basel and UBS annual report, the global art market recovered strongly, with total turnover (including both auction and private market sales) reaching an estimated $65.1 billion, up 29% from 2020, with values surpassing pre-pandemic levels in 2019.2 Dr. McAndrew’s 2023 Art Basel and UBS annual report indicates that the Global Art Market continued to strengthen in 2022, up 3% from the previous year to an estimated $67.8 billion (the second highest year on record following closely behind 2014’s $68.2 billion).3 In 2023, the Global Art Market softened, falling 4% from 2022 to an estimated $65 billion, primarily the result of fewer sales at the top end of the market; however, while the dollar amount decreased, the number of transactions increased by 4% (primarily in the lower price levels). 2024 marked the second year of an ongoing softening in the Global Art Market, experienced in both the public and private sectors, with a further aggregate decline of 12% year-on-year to an estimated total of $57.5 billion globally (a level that has not been seen since pre-pandemic in 2016).4

While 2025 figures for global art sales have not yet been released, total auction sales (at the “big three” - Christie’s, Sotheby’s and Phillips) were up from the previous year (for the first time since 2022) across the Old Masters, Impressionist, Modern, Post-War and Contemporary art sectors, reaching $4.56 billion (an 11% increase from 2024, though still 42% below the 2022 peak), with Impressionist art seeing the highest year-to-year increase of 80.4%.5 This upward trending followed a somewhat lackluster H1 2025, during which auction sales were 6.2% lower year-on-year (only reaching $3.9 billion compared to $4.2 billion in the same period of 2024) - although this period also saw the second highest volume of lots sold since 2016, demonstrating increased activity and broader participation within the middle and lower tiers.6 Key drivers of the “turn around” observed in H2 2025 include increased buyer confidence (as well as higher quality consignments), the return of prominent single-owner collections (which accounted for 32.9% of auction sales during the second half of the year), and marked growth within the $10 million and above “trophy” market (up 19.4% year-to-year), particularly within the Impressionist and Modern sectors.7 Christie’s and Sotheby’s reported sell-through rates (overall) of 88% and 87% (respectively).8 Additionally, the total of the top ten auction sales (of individual lots) reached $757m - which included the record sale of Klimt’s “Bildnis Elisabeth Lederer (Portrait of Elisabeth Lederer)” (1914/16) at $236m - surpassing both 2024 and 2023 totals ($512.6m and $660m, respectively).9

Post-War & Contemporary Art Auction Market

PWC, together with the Modern art sectors, continues to constitute the largest portion of the global auction market, a claim firmly held since 2011. During 2023, the PWC sector alone accounted for 53% of total global art sales by value, a 1% decrease from 2022, and 55% by volume, down by 3% year-on-year. Total sales for the sector reached $6.5 billion in 2023, representing a fall of 16% from 2022, with the total number of lots also decreasing by 3% year-on-year.10

1 Dr. Clare McAndrew, The Art Market 2021, Art Basel and UBS, pp. 30-31

2 Dr. Clare McAndrew, The Art Market 2022, Art Basel and UBS, p. 14

3 Dr. Clare McAndrew, The Art Market 2023, Art Basel and UBS, p. 17

4 Dr. Clare McAndrew, The Art Market 2024, Art Basel and UBS, p. 17

5 ArtTactic, The Art Market 2025: A Year in Review, p.3

6 Artnews, “Global Auction Sales Fell 6 Percent for First Half of 2025 According to ArtTactic Report,” July 16, 2025 (online).

7 ArtTactic, The Art Market 2025: A Year in Review, p. 4

8 Marion Mankeker, Puck: Wallpower, “Art’s $14B Goldilocks Year,” December 20, 2025, pp. 8-9

9 Artlyst, The Top Ten Most Expensive Artworks Sold at Auction In 2025, December 17, 2025

10 Dr. Clare McAndrew, The Art Market 2024, Art Basel and UBS, pp. 174-182.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 6 |

In the first half of 2024, the PWC market continued to soften, down 25.2% from the previous year totaling just $1.43 billion (in the top three auction houses: Christie’s, Sotheby’s and Phillips).11 The top end of the market in particular became more selective, with lots selling over $10 million decreasing by 30% from the same period in 2023 (in the overall market), and no sales in the over $50 million bracket, presumably due to the reluctance of collectors to sell high-end works in a softening market.12 Sales at the top three houses hit its lowest level since 2020 totaling $937.3 million against a pre-sale low estimate of $934.2 million (22.2% down year-on-year). At the top end, in the above $10 million segment, 24 lots sold in the first half of 2024 compared to 29 lots in 2023 (and to the 46 lots sold in the same period at 2022 when the market was at its most recent peak); on aggregate this segment totaled $466.9 million in 2024, down by 24.8% or $620.8 million in 2023.13

Although there were signs of stability, the fall marquee sales that closed-out 2024 saw continued contraction, with total evening sales (across sectors) reaching $906 million, which marked a 42% decline compared to November 2023 (though only 3% decline from May 2024).14 However, 35% of lots exceeded their mid-estimates, which was up from 33% in November 2023.15 While there was growth in the under $1,000,000 sector, the market for artworks above $1mm declined from 199 lots in November 2023 to 146 lots, and only 18 lots (compared to 41 lots in November 2023 and 24 in May 2024) sold for over $10mm. Total revenue from lots selling for over $10mm was down year-to-year by 57%.16

While there was some expansion in the global art market over the past year, 2025 saw a decline of 14.4% (down to $1.12 billion from 2024’s $1.31 billion) in the Contemporary sector (including Young Contemporary) and a decline of 17.7% (down to $733.6 million) in the Post-War sector (due in large part to significant contractions in both the Warhol and Kusama markets of 41.7% and 72.9% respectively). The Young Contemporary segment saw a 39.1% year-on-year decline (to $62.5 million), though the total number of young artists appearing at auction (861) remained above the 10 year average (of 656). This segment also saw a marked decrease in auction guarantee levels, which were 34.3% lower than in 2024, as well as a continued low appetite in the secondary market for these works (as evidenced by the -16.2% average CAGR for resold works within this sector).17 Though still a major revenue-generator accounting for 23.2% of total fine art sales in 2025 (second only to Modern art at 30.3%), the Contemporary art market declined for the fourth consecutive year in both the number of total lots sold (falling 12%) and total auction sales (falling 12.3% to $1.06 billion); however, though average resale CAGR declined from 5.1% in 2024 to 2.3% in 2025, auction guarantee levels were up 8.9%,18 which may suggest increased confidence in this sector. Interestingly enough, the Post-War sector saw an increase in both auction guarantee levels (up 3.8% from 2024) as well as the average resale CAGR, which was up from 2024’s 4.9% to 5.1%.19

Despite an overall sentiment of market uncertainty (and a year-to-year decrease in this sector), some notable results were still achieved in the PWC market. During the Spring season, at Sotheby’s New York Marquee sale, two 24 x 24 inch Andy Warhol paintings from the artist’s renowned Flowers series sold well-over their rather conservative pre-sale estimates (of $1m to $1.5m) to realize $3.8 and $4 million (becoming the second and third highest records for this series format). Also at Sotheby’s, Jean-Michel Basquiat achieved his second highest record for a work on paper with the sale of “Untitled” (1981) realizing $16.365 million (and following the new record for a work on paper at Christie’s in the fall of 2024 for $22.9m). Finally, at Christie’s New York Marquee sale, Marlene Dumas achieved a new high record sale when the monumental “Miss January” (1997) sold for $13.365 million (falling just short of the record for a living female artist set by a 2018 sale of a Jenny Saville work for $12.4 million, which is nearly $15.8 million if adjusted for inflation).

11 ArtTactic, RawFacts, Auction Review, 1st Half 2024, ArtTactic Limited, p. 4.

12 Artnet, The Intelligence Report: Mid-Year Review 2024, Artnet News, p. 5.

13 ArtTactic, Impressionist, Modern, Post-War & Contemporary Art, New York - May 2024, ArtTactic Limited, p. 3.

14 ArtTactic, Auction Analysis: Impressionist, Modern, Post-War & Contemporary Art, New York, November 2024, p. 1

15 ArtTactic, Auction Analysis: Impressionist, Modern, Post-War & Contemporary Art, New York, November 2024, p. 1

16 ArtTactic, Auction Analysis: Impressionist, Modern, Post-War & Contemporary Art, New York, November 2024, p. 3

17 ArtTactic, The Art Market 2025: A Year in Review, pp. 5 & 9

18 ArtTactic, The Art Market 2025: A Year in Review, p. 12

19 ArtTactic, The Art Market 2025: A Year in Review, p. 15

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 7 |

The Fall auction season saw notably strong sales within the PWC market by Matthew Wong, Jean-Michel Basquiat, David Hockney, Christopher Wool, Peter Doig and Agnes Martin. In the Young Contemporary sector, at Sotheby’s (The Now & Contemporary Evening Auction), in New York, Matthew Wong’s “The Gentle Sea” (2017), 40 x 30 inches, sold above estimate ($1.2m-$1.8m) to realize $2,368,000. Among Contemporary artists, Basquiat continued to have a strong year with the Sotheby’s sale of “Crowns (Peso Neto)” (1981), 76.25 x 94.25 inches, for $48,335,000 - the highest auction record for a work from this year and the eighth highest auction record for this artist overall. Hockney achieved his third highest auction record with the Christie’s sale of “Christopher Isherwood and Don Bachardy” (1968), 83.5 x 119.5 inches, in New York, the first of the artist’s acclaimed double portraits, for $44,335,000. This Fall also saw the return of one of Christopher Wool’s iconic, large-scale word paintings, with Christie’s sale of “Untitled (Riot)” (1990), 108 x 72 inches, for $19,840,000 (the fourth highest record for Wool and the highest price achieved for a painting by this artist since 2015). In London, Christie’s sold a large-scale ski painting by Peter Doig, “Ski Jacket” (1994), 71.875 x 83.875, for the GBP equivalent of $19,100,010, which was nearly 2x the high pre-sale estimate of $10,707,784. A work by Agnes Martin achieved one of the highest prices this year within the Post War sector with the sale of a rare (and large-scale) 1960’s painting, “The Garden” (1964), 72 x 72 inches, from the Leonard A. Lauder sale at Sotheby’s for $17,630,000 (also above estimate).

While the market in 2025 for “trophy” lots saw some expansion, this sector continued to experience some challenges within the PWC market as such highly anticipated artworks as Andy Warhol’s “Big Electric Chair” (which was anticipated to sell for $30 million) was withdrawn from Christie’s just prior to the sale, and Alberto Giacometti’s bronze bust “Grande tête mince” was bought-in at Sotheby’s when it failed to meet its reserve of $70m.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 8 |

Subject Artwork

|

|

Banksy (British, b. 1974)

xHxaxpxpxyx xCxhxoxpxpxexrx, 2002

Acrylic and spray paint on modified oil

19.1 x 23.2 x 1.8 in. (48.5 x 58.9 x 5.08 cm)

Signed on the reverse

Accompanied by a registration card issued by the artist’s studio.

Fair Market Value

$1,650,000

Location

Cadogan Tate London

Condition

Excellent

Provenance

Private Collection, gifted by the Artist

Acquired from the above by Masterworks

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 9 |

Artist Background

The famously anonymous street artist Banksy (b. 1974, Bristol, United Kingdom) has become a household name in contemporary art, rising to international fame for his subversive approach to social commentary and persisting air of mystery. Although Banksy’s concealed identity leaves much of his biography open to conjecture, over the years he has shed light on relevant aspects of his adolescence. The artist recalls being expelled from school and briefly going to prison for “petty crime” as a teen. Graffiti became his outlet for self-expression when he joined the Bristol-based graffiti group DryBreadZ crew, tagging his pseudonym “Banksy” all around the city. In the late 1980s, he developed his signature stencil style inspired by the use of stencil in revolutionary propaganda throughout history and the practical time-saving nature of the technique. By the early 1990s, he had become a fixture of the British street art scene. During this decade, he met the photographer Steve Lazarides, who became Banksy’s documentarian and later, his agent. Banksy’s artistic practice expanded to include painting, sculpture, and film, and he held his first solo exhibition of acrylic on canvas works in an apartment in Easton, Bristol, in 1998. He moved to London around the turn of the century and retreated further into anonymity, showing his eyes on a recording for the final time in 2003. In July of that same year, his exhibition held in a former warehouse, “Turf War,” startled London’s art world with its flagrant and dark political humor. As his anarchical reputation in the art world grew, so did the boldness of his artistic interventions. Between 2003 and 2005, he successfully installed “re-mixed” replicas of Old Master oil paintings in prestigious museums, including Tate in London, the Louvre in Paris, and the Metropolitan Museum of Art in New York, among many others. In 2010, he directed a documentary about graffiti artists titled “Exit Through the Gift Shop,” which received an Academy Award nomination. Banksy’s achieved mainstream success allowed him to pursue larger conceptual installation works like his apocalyptic amusement park installation “Dismaland” (2015) in Weston-super-Mare, England. In line with his egalitarian ethos, all of “Dismaland’s” building materials were recycled into shelters for homeless migrants after the show’s closure. Given the artist’s anonymity, little is known about his current whereabouts; however, Banksy remains active as an international graffiti artist and art world disruptor. His most recent intervention, a stencil of a gorilla releasing animals, appeared on the gates of the London Zoo on August 13, 2024, after nearly a week of stenciling animals around the city.

Banksy does not have any gallery representation; he is supported only by his discreet and appropriately ironic office Pest Control, which authenticates his works. Despite the artist’s refusal to cooperate with the institutional art world, his widespread popularity has also led him to be the subject of numerous blockbuster traveling exhibitions, including “Banksy: Genius or Vandal?,” and “Banksy in New York.” Rather than ostracize him, Banksy’s unique and subversive position in the art world has made him especially desirable in the commercial market.

Valuation Narrative

“xHxaxpxpxyx xCxhxoxpxpxexrx” (2002), 19.1 x 23.2 x 1.8 inches, is a characteristic example of Banksy’s “modified” or “vandalized” oil paintings, which insert contemporary, often political, iconography or commentary onto Old Master style paintings. For this series, the artist paints over “ready-made” paintings (typically sourced from local flea markets around London) and then frames them with ornate gilded frames made by his studio to highlight the classic academic style of the series. Banksy’s “modified” or “vandalized” oil paintings were first exhibited in an empty store front in London at his solo exhibition Crude Oils in 2005, two years before the Artwork’s creation. He spray painted his first “Happy Choppers” on Whitecross Street Market in London in 2002 as an activist response to the use of American and British Apache helicopters in Afghanistan. The Artwork’s composition appears to reference the scene of flying Apache helicopters in the epic 1979 film Apocalypse Now. The Artwork is a small, reclaimed oil painting on canvas of a forested stream with a spray-painted helicopter at the center of the composition. The artist has framed the canvas in a traditional gilded frame.

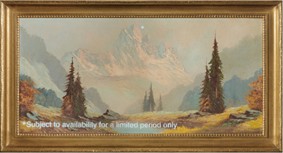

Vandalized oil paintings by Banksy are offered only sporadically through auction and offerings of examples from this series that, like the subject work, feature the highly sought-after chopper image are few and far between. Most recently, on February 8, 2025, “Subject To Availability” (2011), 19.63 x 35.88 inches, sold at Sotheby’s Saudi Arabia for $1,200,000.20 Although larger than the subject work and with a more expansive (Bierstadt-inspired) landscape, this painting has a somewhat diminished line of spray-painted text across the lower left edge of the composition (indicated with an asterisk) that demonstrates both a weaker visual impact as well as a less extensive intervention by the artist.

The next most recent sale of a related painting from this series occurred on June 29, 2023, when another larger example, “Congestion Charge” (2004), 26.94 x 31 inches, sold (within estimate) at Bonhams London for the GBP equivalent of $2,121,000; though also lacking the chopper motif, this painting has an image-based intervention of a stenciled sign advertising “Congestion charging” that is cleverly and discordantly juxtaposed against a bright and colorful bucolic landscape.

20 Acquired by Masterworks 471, LLC

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 10 |

Prior to this, on May 19, 2022, “This Is Not A Photo Opportunity” (2007), 24.12 x 28.12 inches, which is only slightly larger than the subject work and features three lines of text (a transcription of the title) as opposed to a boldly stenciled image, sold at Sotheby’s New York for $2,690,000. This painting was subsequently (and much more recently) purchased by Masterworks in a private transaction for $2,050,000.21 The disparity between the 2022 auction sale price and the more recent private sale (which occurred in January 2025) is supportive of the substantial softening of the market during this period.

Finally, the most recent public auction sale of a painting featuring Banksy’s chopper stencil (presumably the exact same stencil used in the subject work but in reverse) was on March 2, 2022, when a larger painting with a clearer and brighter composition as well as a second (significantly smaller) helicopter on the horizon, “Vandalised Oil (Choppers)” (2006), 24 x 37 inches, sold well-above its pre-sale estimate (of the GBP equivalent of $3,338,562-$4,673,987) at Sotheby’s London to realize $5,855,705. Although this painting sold in a much stronger market for the artist, the strength of this sale is indicative of the desirability of the chopper motif among Banksy collectors.

The Fair Market Value of the Painting was determined in relation to the aforementioned paintings, with differences in subject, scale, execution, composition and date of sale taken into consideration. Based on this information, it is the opinion of the appraisers that the Fair Market Value of the subject work is above the recent sale of “Subject To Availability” (2011) and below both the recent private sale of “This Is Not A Photo Opportunity” (2007) and the 2023 auction sale of “Congestion Charge” (2004).

21 Acquired by Masterworks 464, LLC

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 11 |

Comparable Sales

|

Title: Subject To Availability Year Made: 2011 Medium: Oil, spray paint on canvas Dimensions: 19.63 x 35.88 inches Date of Sale: February 8, 2025 Sale Name: Origins Sale Location: Sotheby’s Saudi Arabia Lot: 27 Estimate: $800,000-$1,200,000 Realized Price: $1,200,000 | |

|

|

Title: Congestion Charge Year Made: 2004 Medium: Oil on canvas Dimensions: 26.94 x 31 inches Date of Sale: June 29, 2023 Sale Name: Post-War & Contemporary Art Sale Location: Bonhams London Lot: 108 Estimate: $1,517,494-$2,276,244 Realized Price: $2,121,000

| |

|

Title: This Is Not A Photo Opportunity Year Made: 2007 Medium: Spray paint on found oil painting in artist’s frame Dimensions: 24.12 x 28.12 inches Date of Sale: May 19, 2022 Sale Name: The Now Evening Auction Sale Location: Sotheby’s New York Lot: 21 Estimate: $2,000,000-$3,000,000 Realized Price: $2,690,000 | |

|

Title: Vandalised Oil (Choppers) Year Made: 2006 Medium: Oil and spray paint on canvas Dimensions: 24 x 37 inches Date of Sale: March 2, 2022 Sale Name: The Now Evening Auction Sale Location: Sotheby’s London Lot: 7 Estimate: $3,338,562-$4,673,987 Realized Price: $5,855,705

|

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 12 |

Sources of Data

Auction Houses: Christie’s, Sotheby’s, Phillips, Bonhams, Artcurial, SBI Art Auction, Mainichi Auction, Mallet Japan, China Guardian, Ketterer Kunst, Seoul Auction, iART Co.

Online Databases: Artprice, Artnet, AskArt, Mutual Art and the Baer Faxt Auction Database

Masterworks Appraisers’ Qualifications

Abigail Athanasopoulos, Director of Appraisals, is an Accredited Senior Appraiser with the American Society of Appraisers (ASA) with over nineteen (19) years of experience appraising fine art. Prior to her position with Masterworks, she was the Founder & Principal of Spectrum Appraisals, LLC, a comprehensive art appraisal and advisory firm providing a range of services, including fair market value and replacement value appraisals for a wide variety of intended uses. She previously worked as a senior appraiser and project manager for Appraisal Resource Associates, Inc., and a gallery associate at D. Wigmore Fine Art, New York; she has also recently served on ASA’s executive committee and is a former member of ArtTable (a professional organization dedicated to advancing the leadership of women in the visual arts). Ms. Athanasopoulos holds a B.A. in Art History from Wellesley College and has completed extensive coursework in appraisal studies through New York University’s Appraisal Studies Program, Pratt Institute (in association with the American Society of Appraisers), from which she obtained a Certificate in Fine & Decorative Arts Appraisal Studies, and the American Society of Appraisers. She is “qualified” per IRS guidelines and is compliant with the Uniform Standards of Professional Appraisal Practice (USPAP).

Jessica Maliszewski, Senior Appraiser, is an Accredited Member of the Appraisers Association of America (AAA) specializing in Post-War, Contemporary and Emerging Art. A member of the AAA for eight (8) years, Ms. Maliszewski is Uniform Standards of Professional Appraisal Practice (USPAP) compliant and presently serves on AAA’s Membership Committee. As a Fine Art Appraiser, she has completed appraisals for clients nationally and internationally for purposes of insurance, tax and estate planning, charitable donations, and equitable distribution. Though predominantly working in Post-War, Contemporary and Emerging Art since 2008, Ms. Maliszewski has further experience in valuing and cataloguing a wide variety of fine and decorative objects. In addition to her appraisal work, Ms. Maliszewski has twenty (20) years of experience in New York and London, working in collections management and research, and working for art consultancies, art fairs, museums, galleries, and artist studios. Ms. Maliszewski holds a B.A. with a concentration in Art History from Northeastern University, an M. Litt in the History of Art and Connoisseurship in Fine and Decorative Arts from Christie’s Education in London, and completed extensive coursework in appraisal studies through New York University’s Appraisal Studies Program and the Appraisers Association of America.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 13 |

Statements and Disclosures

This Appraisal Report consists of pages and must be presented in its entirety to be valid. This document is prepared solely for internal corporate and accounting purposes as described in the Scope of Work using the Sales Comparison approach to arrive at the Fair Market Value as of the stated effective valuation date. It is to be used solely by the intended users listed in this Appraisal Report for that purpose and can be relied upon by the intended user as described in the Scope of Work.

Unless otherwise stated herein, this Appraisal Report is based only on the readily apparent identity of the item appraised, and no further opinions or guarantee of authenticity, genuineness, attribution, or authorship is made. However, in appraising the subject property, the Masterworks Appraiser(s) found no reason to question the authenticity of the article, except as noted. To the knowledge of the Masterworks Appraiser(s), no laboratory testing has been performed on the subject property.

Unless otherwise stated herein, the appraised value is based on whole ownership and possessory interest undiminished by any liens, fractional interests or any other form of encumbrance or alienation.

This Appraisal Report is made at the request of the parties named for their use. The Appraisal Report is not an indication or certificate of title ownership. The identification of the interest of the requesting parties is simply represented to the Masterworks Appraiser(s) by such parties and no inquiry or investigation has been made nor is any opinion given as to the truth of such representation.

The value expressed herein reflects the professional judgment and opinion of the Masterworks Appraiser(s) and is not a representation or warranty that the item will realize that value if offered for sale at an auction or otherwise. The value expressed is based on current information on the assigned effective valuation date stated on the cover page of this report. No opinion is hereby expressed as to any future value, nor unless otherwise stated, as to any past value.

Masterworks is active in bidding in the auction market. If there is a sale of a work that Masterworks has purchased at public auction that qualifies as comparable to the Artwork, the comparable sale may be included in the comparable data set at the discretion of the Masterworks Appraiser(s), provided that the related party nature of the comparable sale will be noted in the appraisal.

The market level selected for this assignment is based on the subject property’s current use and alternative uses as relevant to the type and definition of value and the intended use of the Appraisal Report. As such, the Masterworks Appraiser(s) considered the most common marketplace(s) given the purpose of this appraisal assignment.

The Masterworks Appraiser(s) are not required to give testimony, be present in any court of law, or appear before any commission or board by reason of this Appraisal Report without reasonable prior notice. Should this report be challenged in any way, not limited to litigation, it is understood that the Masterworks Appraiser(s) are prepared to defend this Appraisal Report, if required. Appearance and testimony at deposition, trial, or alternative dispute resolution proceedings and the necessary preparations thereof are considered to be new and separate assignments.

Possession of this Appraisal Report, or a copy thereof, does not include the right of publication without the written consent of Masterworks. This Appraisal Report, or any part thereof, including the identity of the Masterworks Appraiser(s), shall not be made public through advertising, public relations, news releases, sales, or other distributive or information media without the written consent of Masterworks.

Copies of this Appraisal Report and written and electronic notes pertaining to the appraisal assignment will be kept in the offices of Masterworks for a minimal period of five (5) years after the date of issue or two (2) years after final disposition of any judicial proceedings involving the Masterworks Appraiser(s), whichever period expires last. Masterworks makes every effort to store records pertaining to the Appraisal in a safe and secure environment. However, Masterworks is not responsible for acts of nature, war, terrorism, or other unexpected catastrophes which may affect the safekeeping of this Appraisal Report.

All matters regarding the duties, responsibilities, and liabilities of the Masterworks Appraiser(s) are in accord with the Valuation Standards and Professional Practices as outlined by the Appraisal Foundation in the most recent publication of the Uniform Standards of Professional Appraisal Practice (last issued in 2024) and the Principles of Practice and the Code of Ethics of the Appraisers Association of America.

Submission of this Appraisal Report concludes this appraisal assignment.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 14 |

Appraisal Terminology and Definitions

Appraisal: As defined in the Uniform Standards of Professional Appraisal Practice (USPAP), “the act or process of developing an opinion of value; an opinion of value.” According to the USPAP, value can “be numerically expressed as a specific amount, as a range of numbers, or as a relationship (e.g., not more than, not less than) to a previous value opinion or numerical benchmark (e.g., assessed value, collateral value).” It should be noted that the USPAP states that using any other term for an appraisal does not remove the work from being in compliance with USPAP; it is an appraisal if an opinion of value is given.

Buyer’s Premium: The percentage of the bid or “hammer” price paid by the buyer to the auction house when purchasing an item. The fee usually ranges between 5% and 25% of the hammer price.

Bought In (BI): Occurs at auction when an object does not meet its reserve price and fails to sell.

Catalogue Raisonné: A scholarly catalogue that should include all the known works of an artist or all of his or her known works in a specific medium at the time of the catalogue’s compilation. Essential information identifying the works is included, making the catalogue a definitive reference book.

Certificate of Authentication/Authenticity: An official document that certifies that the piece in question is correct, of the period, and by the artist designated. Some states (including New York) require specific information be included on a certificate of authentication.

Clear Title: Refers to ownership of property that is free from encumbrance, obstruction, burden or limitation.

Comparables: Those objects selected by the appraiser as being similar to one being appraised. An examination and analysis of sales figures for similar works or comparable objects allows the appraiser to arrive at an appraised value for the object under consideration.

Condition: Term referring to the physical state of a property and must be noted in an appraisal document.

Conservation: The treatment and preventive care of an object so that its condition does not deteriorate and will remain stable; the preservation of a work of art involving careful maintenance and protection of an object, using materials and procedures that will have no adverse effect on it.

Cost Approach: A valuation approach used to determine the value of an object based upon the cost of re-creating the identical piece. This approach may be applied to the decorative arts when the methods of construction or materials used are replicable.

Hammer Price: The actual (final) bid price at auction; it does not include the buyer’s premium.

Hypothetical Conditions: According to USPAP, those conditions that are contrary to the conditions that actually exist, but are supposed for the purpose of reasonable analysis. Hypothetical conditions assume conditions contrary to known facts about physical, legal or economic characteristics of a subject property or about conditions external to the property, such as the market conditions or trends, or about the integrity of data used in an analysis. Appraisals of damaged or destroyed objects employ hypothetical conditions. A hypothetical condition may be used in an assignment only if 1) the use of the hypothetical condition is clearly required for legal purposes, for purposes of reasonable analysis or for purposes of comparison; 2) the use of the hypothetical condition results in a credible analysis; and 3) the appraiser complies with the disclosure requirements set forth in USPAP for hypothetical conditions.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 15 |

Income Approach: A valuation approach used to determine the value of a work of art or object that will be used to generate future income. This is most often done through leasing, rental or the creation of reproductions but not through a one-time only sale with transfer of title and/or copyright.

Market Analysis: The study of market conditions for a specific type of personal property; sometimes both the retail and wholesale markets must be examined and analyzed.

Medium: 1.) The material from which an object or artwork is made or on which it is produced; it may include paper, canvas, board, cel (acetate), bronze; 2.) The specific tool and material used by an artist; e.g., brush and oil paint, chisel and stone; 3.) The mode of expression used by an artist; e.g., painting, sculpture, graphic arts, etc.; 4.) A liquid that may be added to a paint to increase its manipulability without decreasing its adhesive, binding or film forming properties.

Most Appropriate Market or Marketplace: The venue in which an appraiser determines that an object can be sold most easily and at the highest price. In the case of personal property, when comparables are scarce, it frequently references the most appropriate market, which can be a combination of auction and private gallery sales.

No Commercial Value (NCV): A term that usually refers to an object or a group of objects, usually in estate situations, for which it is not reasonable to assign a monetary value; for example, a mattress and a box spring.

Offering Amount: For Masterworks’ purposes, the aggregate total value of all Class A shares in a given Artwork as reflected in the final offering circular filed with the SEC.

Original Cost: Also known as the historical cost or the cost of acquiring an item of personal property.

Offering Date: For Masterworks’ purposes, the date at which the final offering circular is filed with the SEC.

Personal Property: Defined by USPAP as “identifiable, tangible objects that are considered by the general public as being “personal”; for example, furnishings, artwork, antiques, gems and jewelry, collectibles, machinery and equipment.”

Primary Market: A market created either by the maker or the maker’s agent when an object is sold for the first time, usually in galleries or stores. The secondary market is the venue for the sale of an object between a seller and a buyer when neither of them have participated in the creation or initial sale of the object. In the instance of multiples, a valid secondary market cannot exist while the maker or his agent retains a supply of the original offering.

Primary Source: Material, used in research and data comparisons, that is gathered from first-hand witnesses and includes auctions attended, galleries, art fairs and stores visited as well as actual comparables witnessed by the appraiser.

Provenance: The history of an object that may include its past ownership as well as its exhibition and catalogue history.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 16 |

Qualified Appraisal: An appraisal will be treated as a qualified appraisal within the meaning of IRS Code §170 (f)(11)(E) if the appraisal complies with all the requirements of §1.170A-13(c) of the existing regulations (except for the extent the regulations are inconsistent with § 170 (f)(11)), and is conducted by a qualified appraiser in accordance with generally accepted appraisal standards. See sections 3.02(2) and 3.03 of Notice 2006-96. An appraisal will be treated as having been conducted in accordance with generally accepted appraisal standards within the meaning of §170 (f)(11)(E)(i)(II) if, for example, the appraisal is consistent with the substance and principles of the Uniform Standards of Professional Appraisal Practice (“USPAP”).

Qualified Appraiser: (1) Appraisal designation. An appraiser will be treated as having earned an appraisal designation from a recognized professional appraiser organization within the meaning of §170 (f)(11)(E)(ii)(I) if the appraisal designation is awarded on the basis of demonstrated competency in valuing the type of property for which the appraisal is performed. (2) Education and experience in valuing the type of property. An appraiser will be treated as having demonstrated verifiable education and experience in valuing the type of property subject to the appraisal within the meaning of §170 (f)(11)(E)(iii)(1) if the appraiser makes a declaration in the appraisal that, because of the appraiser’s background, experience, education and membership in professional associations, the appraiser is qualified to make appraisals of the type of property being valued. (3) Minimum education and experience. An appraiser will be treated as having met minimum education and experience requirements within the meaning of §170 (f)(11)(E)(iii)(1) if the appraiser has successfully completed college or professional level coursework that is relevant to the property being valued, has obtained at least two years of experience in the trade or business of buying, selling, or valuing the type of property being valued, and has fully described in the appraisal the appraiser’s education and experience that qualify the appraiser to value the type of property being valued.

Recto: The front side of a painting.

Sales Comparison Approach: the most commonly applied valuation approach when appraising personal property, in which appraised value is based on achieved prices for similar works by the same artist or artisan of equal standing and related reputation (alternatively called Comparative Market Data Approach, Market Data Approach or Comparable Market Data Approach.)

Secondary Market: Refers to the marketplace in which a used object is bought and sold. Once an item is no longer available from the original source, it is considered a secondary market item. The term usually refers to the auction market and is in no way associated with the value or the condition of the object. The secondary market is the venue for the sale of an object, through an auction or a gallery, between a seller and a buyer, neither of whom has participated in the creation or initial sale of the object. In the instance of multiples, a valid secondary market cannot exist while the maker or his agent retains a supply of the original offering.

Secondary Source: an article or book that discusses information that was first presented somewhere else. Examples of secondary sources utilizing exact primary sources in research and data comparison are Artnet, ArtFact, P4a, Gordonsart, Art-Sales-Index, newel.com and other internet research tools.

Seller’s Premium or Seller’s Commission: The percentage of the bid or “hammer” price paid by a seller to an auction house when selling an item. The fee ranges from nothing to 35 percent and may be more negotiable than the buyer’s premium.

Statement of Assumptions & Limiting Conditions: Terms or concepts generally linked together in most appraisals. An assumption is that which is taken to be true. An extraordinary assumption is an assumption, directly related to a specific assignment, that, if found to be false, could alter the appraiser’s opinions or conclusions. A limiting condition refers to the conditions that limit the appraiser’s examination or research of the appraised items and the appraisal assignment. Hypothetical conditions are those that are contrary to what exists, but are supposed for the purpose of analysis.

Uniform Standards of Professional Appraisal Practice (USPAP): The appraisal standards covering the development and communication of appraisers’ opinions and conclusions published by the Appraisal Standards Board of The Appraisal Foundation. First published in 1987, these standards apply to all disciplines of appraising.

Verso: The backside of a painting.

Work Size: The dimensions of works on panel or board. When the word “sight” is used in conjunction with worksize, it refers to the dimensions of the visible image of the work.

| Fair Market Value Appraisal for Use by Masterworks Administrative Services, LLC Effective Date of Valuation: January 28, 2026 | Page 17 |